MNI US OPEN - Prices Missing on CME Data Outage

EXECUTIVE SUMMARY

- CME FUTURES OUTAGE DISRUPTS TRADING ACROSS MAJOR GLOBAL MARKETS

- STARMER FACES LABOUR REVOLT OVER ‘DAY ONE’ WORKERS’ RIGHTS REFORMS

- TAKAICHI OBTAINS MAJORITY IN LOWER HOUSE AHEAD OF BUDGET VOTES

- MNI PROJECTS GERMAN NATIONAL CPI AT 2.3-2.4% Y/Y, CORE AT 2.8%

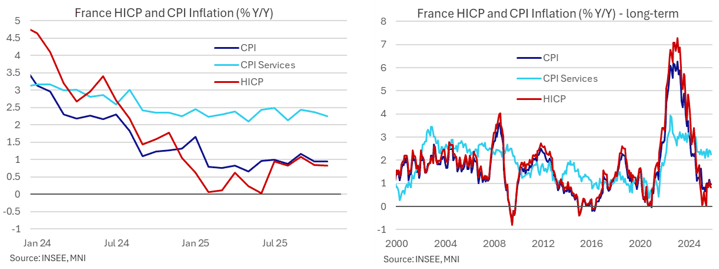

Figure 1: France HICP softer than expected in November flash

NEWS

GLOBAL (BBG): CME Futures Outage Disrupts Trading Across Major Global Markets

Trading of futures and options on the Chicago Mercantile Exchange stopped for several hours due to a data center fault, disrupting markets across equities, foreign exchange, bonds and commodities. The malfunction is already longer than a similar, hours-long outage due to a technical error back in 2019 and underscores the reach of CME Group and its Globex electronic trading platform. It has also triggered widespread frustration, as market participants contemplated the prospect of a lost trading session.

US/INDIA (MNI): US-India Trade Deal Expected By Year End - Indian Trade Secretary

Reuters reports Indian Trade Secretary Piyush Goyal stating, "India expects to have a deal with the US before year-end as most issues already resolved." Goyal adds negotiators are holding "virtual talks", noting remaining issues could be addressed at the political level. Commerce Secretary Rajesh Agrawal said Monday negotiators are close to finalising a package covering US market access to India, and reducing 25% reciprocal/25% additional oil tariffs, per the Times of India.

CANADA (BBG): Carney Loses Quebec Minister Guilbeault After Energy Deal

Prime Minister Mark Carney lost a cabinet minister over his oil pipeline agreement with Alberta, marking the first major fracture in his Liberal Party caucus over the government’s energy policies. Steven Guilbeault, a former environmental activist with Greenpeace, resigned his position as culture minister but will remain in Parliament.

UK (The Times): Starmer Faces Labour Revolt Over ‘Day One’ Workers’ Rights Reforms

Sir Keir Starmer is facing a revolt from Labour MPs after abandoning a manifesto pledge to give workers the right to claim unfair dismissal from “day one”, a policy championed by Angela Rayner. Ministers axed the move to change the “qualifying period” for unfair dismissal from 24 months to day one in an attempt to get the government’s controversial workers’ rights legislation through the House of Lords. Workers will now have to have been in their job for at least six months to qualify. The announcement triggered a backlash from left-wing Labour MPs and the union Unite, which accused Starmer of gutting Labour’s Employment Rights Bill.

GERMANY (BBG): Germany Set to Approve €2.9 Billion in Arms in Defense Surge

German lawmakers are set to approve spending €2.9 billion ($3.4 billion) on 11 military procurement contracts, including for drones, rifles and missiles, in deals that will go largely to domestic manufacturers. The defense ministry asked parliament to give the green light for the orders, including the purchase of as many as 250,000 G95 assault rifles from Heckler & Koch for €765 million, according to procurement documents seen by Bloomberg News. Lawmakers are expected to approve the purchases at a closed-door meeting next week.

GERMANY (MNI): Pensions Package Freezes Current Payments Through 2031

The German coalition has agreed on passing a pension package freezing the current level of payments through 2031 according to matching local media reports, according to Handelsblatt. The pension reform has been on the edge of failing internally in CDU as backbench support for the bill faded. The approval should stabilize the coalition for now after labour minister Bas (SPD) indirectly warned against a breakup of the coalition should CDU not manage to keep mentioned subgroups voting in favour, letting the reform fail.

JAPAN (BBG): Takaichi Obtains Majority in Lower House Ahead of Budget Votes

Japanese Prime Minister Sanae Takaichi’s ruling coalition added three independent lawmakers, securing a majority in the powerful lower house of parliament ahead of two key budget votes. Her Liberal Democratic Party welcomed the three lawmakers belonging to the “Reform Association” parliamentary group to its ruling coalition with the Japan Innovation Party, known as Ishin, LDP Secretary-General Shunichi Suzuki told reporters Friday.

JAPAN (BBG): Japan to Issue More Short-Term Debt to Fund Takaichi’s Stimulus

Japan plans to increase its issuance of short-term debt to help finance Prime Minister Sanae Takaichi’s economic package, a move that comes as markets grow uneasy about fiscal discipline and upward pressure on super-long yields. The cabinet approved Friday a ¥18.3 trillion ($117 billion) extra budget to fund the largest round of fresh spending in a stimulus package since the scaling back of pandemic restrictions. Of that total, ¥11.7 trillion will be covered by fresh debt, according to the Finance Ministry.

JAPAN (BBG): Japan to Spend $2 Billion on AI, Semiconductors in Extra Budget

Japan is set to spend roughly ¥252.5 billion ($1.6 billion) in an extra budget to further support developments of artificial intelligence and semiconductors. The sum is much smaller than the about ¥1.5 trillion allocation in last year’s supplementary budget, as the government is expected to start securing most of the additional funding for those sectors in regular budgets going forward, according to a ruling party lawmaker and the Ministry of Economy, Trade and Industry. That’s expected to provide more stable funding to the sectors.

RUSSIA/HUNGARY (BBG): Orban to Meet Putin as He Eyes Sanctioned Russian Refineries

Hungarian Prime Minister Viktor Orban will meet President Vladimir Putin as Russia weighs the sale of sanctioned refineries that have triggered concerns about fuel shortages across eastern Europe. Orban said he is traveling to Moscow on Friday to discuss crude oil and natural gas supplies after recently securing, via President Donald Trump, an exemption from US sanctions on Russian oil. He said Russia’s war on Ukraine would also be discussed.

DATA

EUROZONE DATA (MNI): Consumer Inflation Outlook Little Changed - ECB

- ECB OCT CONSUMER 1-YR INFLATION EXPECTATION 2.8%

- ECB OCT CONSUMER 3-YR INFLATION EXPECTATION 2.5%

Eurozone consumer inflation expectations for the year ahead picked up in October, though the longer-term outlook was unchanged, an ECB survey published Friday showed. Median expectations for inflation over the next 12 months increased to 2.8%, from 2.7% in September. Expectations for inflation three years ahead were unchanged at 2.5%, as were inflation expectations for five years ahead, at 2.2%.

GERMANY DATA (MNI): MNI Projects 2.3-2.4% Y/Y German National CPI, Core 2.8%

From state-level data that equates to 89.1% weighting of the national November flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.3-2.4% Y/Y (2.3% prior) and fell around 0.2-0.3% M/M. See the tables below for full calculations. Analyst consensus stands at 2.4% Y/Y and -0.2% M/M, risks to consensus therefore appear to be skewed slightly to the downside. Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies around 2.8% Y/Y (2.8% prior). Analysts have expected core to be roughly unchanged to slightly higher this time.

GERMANY DATA (MNI): Retail Sales Start Q4 on a Sour Note After Q3 Consumption Weakness

- GERMANY OCT RETAIL SALES -0.3% M/M, +0.9% Y/Y (VS +0.3% M/M, +0.8% Y/Y SEP)

German October retail sales were weaker than expected, even after considering a decent upward revision to the August data. It sees a weak start to Q4 consumption after what was a very weak -0.3% Q/Q for private consumption in final GDP data released earlier this week. Retail sales volumes fell -0.3% M/M (cons 0.2) in October on a seasonally and calendar adjusted basis after an upward revised 0.3% (initial 0.2) in September

FRANCE DATA (MNI): France HICP Softer Than Expected in Nov Flash

- FRANCE NOV FLASH HICP -0.2% M/M, +0.8% Y/Y

- FRANCE NOV FLASH CPI -0.1% M/M, +0.9% Y/Y

- FRANCE NOV FLASH SERVICES CPI +2.2% Y/Y

French inflation was softer than expected in flash November data, more notably so for the HICP metric. Within CPI, services and manufactured products both moderated further in Y/Y terms. France HICP inflation was surprisingly soft in the preliminary November release, holding at 0.83% Y/Y after 0.84% in October. Bloomberg consensus had looked for 1.0% whilst the MNI median had looked for 0.9% - still, it's notable that only 2 of 22 analysts in the Bloomberg survey had looked for a 0.8 print.

FRANCE DATA (MNI): Consumer Spending Rises Again But Tepid Trend Remains

- FRANCE OCT CONSUMER SPEND +0.4% M/M, +0.4% Y/Y (VS +0.3% M/M, -0.2% Y/Y SEP)

France consumer spending was a little stronger than expected in October for a third consecutive increase, with a boost from energy consumption during a colder October. The Y/Y tilted back into positive territory for the first time since June but it's only at 0.4% and longer-term trends remain tepid at best. Consumer spending increased 0.4% M/M in real terms in October, slightly beating consensus of 0.3% and up from 0.3% prior. This was the third consecutive positive reading.

FRANCE DATA (MNI): Q3 GDP Confirms Flash at 0.5% Q/Q, Domestic Demand Softer

- FRANCE Q3 FINAL GDP +0.9% Y/Y (VS +0.7% Q2)

- FRANCE Q3 FINAL GDP +0.5% Q/Q (VS +0.3% Q2)

France Q3 final GDP confirmed flash estimates at 0.5% Q/Q for an acceleration from 0.3% in Q2, along with 0.9% Y/Y after a downward revised 0.7% (-0.1pp) in Q2. GDP growth has been picking up pace throughout 2025 after US-driven trade disruption in Q1, with this quarterly rate being the highest since Q2 2023. Final domestic demand continued to lag, however.

FRANCE OCT PPI +0.0% M/M, -0.8% Y/Y (VS -0.1% M/M, +0.1% Y/Y SEP) (MNI)

SPAIN DATA (MNI): Flash Nov Core HICP Looks In Line With Expectations

- SPAIN NOV FLASH HICP +0.0% M/M, +3.1% Y/Y

- SPAIN NOV FLASH CPI +0.2% M/M, +3.0% Y/Y

- SPAIN NOV FLASH CORE CPI +2.6% Y/Y

Spanish headline inflation was a touch higher than expected in November. However, core metrics look to have printed in line with consensus. Headline HICP inflation rose 3.1% Y/Y, down from 3.2% prior but above the 3.0% consensus. Core HICP (excluding energy and unprocessed foods) was steady at 2.6% Y/Y. Headline CPI was 3.0% Y/Y as expected, down from 3.1% in October. The sequential increase of 0.2% M/M was slightly above the 0.1% consensus, suggesting only rounding kept Y/Y headline CPI in line. Core CPI ticked up to 2.6% Y/Y (vs 2.5% prior) as expected.

ITALY DATA (MNI): Services Drives Lower-Than-Expected Italian Flash HICP

- ITALY NOV FLASH HICP 1.1% Y/Y (1.3% FCST, 1.3% OCT)

- ITALY NOV FLASH HICP -0.2% M/M (-0.1% FCST, -0.2% OCT)

Italian flash November HICP inflation was lower than expected at 1.1% Y/Y (vs 1.3% cons 1.3% prior). Core inflation looks to have driven the surprise, with HICP excluding energy, food, alcohol and tobacco at 1.7% Y/Y (vs 1.9% prior). Most estimates we had seen looked for a steady core HICP reading. Services inflation pulled back notably to 2.5% Y/Y (vs 2.9% prior). A large pullback in restaurants and hotels looks to be a driver here (3.3% Y/Y vs 3.9% prior), with transport (0.0% vs 0.2% prior) and miscellaneous goods and services (3.2% Y/Y vs 3.3% prior) potentially also contributing to the downside.

ITALY DATA (MNI): Tepid Consumption Trends Take Shine Off Upwardly Revised Q3 GDP

Italian Q3 GDP was revised up a tenth to 0.1% Q/Q (vs -0.1% prior), and is now back in line with the original consensus for the flash release. Details suggest inventories were a large drag in Q3, but weak household consumption trends remain a concern. We continue to think that the biggest risk to continued Italian fiscal consolidation (and by extension BTP/Bund spread tightening) is the growth outlook. While a cyclical recovery is expected over the coming years, fading EU RRP disbursements and a weak potential growth picture remain medium-term fragilities.

SWITZERLAND DATA (MNI): Q3 GDP Unrevised, Net Exports Drag Heavily

- SWISS Q3 GDP -0.5% Q/Q, +0.5% Y/Y (VS +0.2% Q/Q, +1.3% Y/Y Q2)

Swiss GDP growth was unrevised in the final Q3 release at a very weak -0.5% Q/Q on a sports-event and seasonally-adjusted basis, following Q2's 0.2% (upwardly revised by 0.1pp). "The negative result is largely down to the chemical and pharmaceutical industry, where strong exports gave way to a compensatory decline. Below-average growth in the services sector failed to offset the downturn in the industrial sector.", SECO comments.

SWISS NOV KOF ECONOMIC BAROMETER 101.7 (VS 101.5 OCT) (MNI)

SWEDEN DATA (MNI): Q3 GDP "Surprisingly" Meets Flash Estimates

- SWEDEN FINAL Q3 GDP +2.6% Y/Y

Swedish Q3 GDP confirmed flash estimates - somewhat of an impressive feat given the volatile and revision prone nature of the flash. Consensus had a large negative skew, with estimates ranging from 0.6-1.1%. This leaves GDP well above the Riksbank's 0.5% September MPR forecast. Note that Q2 was also revised up to 0.8% Q/Q. No meaningful Riksbank policy changes expected in the near-term, with the policy rate likely to be at 1.75% for "some time to come". However, recent positive activity signals suggest the risks of a hike back to 2.00% are greater than the risk of another cut over the next 6-12 months.

SWEDEN OCT RETAIL SALES +3.4% Y/Y (MNI)

JAPAN DATA (MNI): Japan Nov Tokyo Core CPI Rises 2.8% vs. Oct 2.8%

- JAPAN NOV TOKYO CORE CPI +2.8% Y/Y; OCT +2.8%

- JAPAN NOV TOKYO CORE-CORE CPI +2.8% Y/Y; OCT +2.8%

- JAPAN NOV SERVICES PRICES +1.5% Y/Y; OCT +1.6%

The year-on-year rise in Tokyo core inflation in November was unchanged from October at 2.8% and remained above 2% for the 13th consecutive month, data from Japan’s Ministry of Internal Affairs and Communications showed on Friday. The November index was lifted by higher energy prices, which rose 2.6% y/y from 2.2% in October, but was partly offset by a slowdown in prices of foods excluding perishables to 6.5% from 6.7%.

JAPAN DATA (MNI): Japan Oct Factory Output Posts 2nd Straight Rise

- JAPAN OCT FACTORY OUTPUT +1.4% M/M; SEPT +2.6%

Japan’s industrial output rose 1.4% m/m in October for a second straight increase, following a 2.6% rise in September, driven by higher production of automobiles, electrical machinery, and information and communication electronics equipment, data from the Ministry of Economy, Trade and Industry showed on Friday. Automobile production climbed 6.6% m/m in October for a third consecutive increase after a 1.0% gain in September, while production of electrical machinery and information and communication electronics equipment rose 4.2% for a second straight rise following a 4.9% increase.

JAPAN DATA (MNI): Job-to-Applicant Ratio Downtrend Continues, Risking Higher U/E Rates

- JAPAN OCT JOBLESS RATE UNCHANGED FROM SEPT AT 2.6%

Japan Oct jobless rate and job to applicant ratio figures were weaker than expected. The unemployment rate held steady at 2.6%, against a market forecast of 2.5%. The job to applicant ratio ticked down further to 1.18, versus 1.20 forecast (which was also the Sep outcome),The chart below plots this ratio, which is the white line on the chart (also inverted) against the unemployment rate. The continued trend decline in the job-to-applicant ratio points to further upside in the unemployment rate, all else equal.

JAPAN OCT RETAIL SALES +1.7% Y/Y; SEPT +0.2% (MNI)

JAPAN OCT RETAIL SALES +1.6% M/M; SEPT +0.0% (MNI)

RATINGS: S&P to Update on France After the Close

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Moody’s on Hungary (current rating: Baa2; Outlook Negative)

- S&P on France (current rating: A+; Outlook Stable), Latvia (current rating: A; Outlook Stable) & Lithuania (current rating: A; Outlook Stable)

- Morningstar DBRS on Germany (current rating: AAA, Stable Trend) & Spain (current rating: A (high), Stable Trend)

FOREX: Greenback Tilts Higher Friday, GBPUSD Edges Back Towards 1.3200

- Despite remaining below the 100.00 mark, the USD index has been drifting higher on Friday morning, paring a portion of this week’s downswing. This has helped the likes of EUR and GBP to underperform across G10, while NZD trims its impressive post-RBNZ advance. The moderate greenback optimism has also prompted a punchy turnaround for gold, falling from overnight highs of $4,193 to session lows of $4,155 around 8am London.

- For NZDUSD, the pair kicked on through its 20-day EMA resistance this week, but importantly has found solid supply at the next touted resistance zone around 0.5725/30, which represents both the 50-day and prior trendline support turned resistance.

- It is worth flagging that yesterday’s EURUSD candle pattern is a doji - a potential reversal signal, and highlighting that this week’s recovery appears corrective – for now. Short-term technical parameters appear well defined; key short-term resistance to monitor at 1.1656, the Nov 13 high and key support at 1.1469, the Nov 5 low.

- Concerns surrounding the degree of fiscal tightening that will ultimately be deployed and likely BOE easing in December remain headwinds for the pound. GBPUSD highs of 1.3269 Thursday closely coincided with a test of 50-day EMA resistance, and today’s move back towards 1.3200 keeps the dominant downtrend in place for now.

- The highlight on the Economic calendar is Canada GDP, while volumes may remain on the low side owing to the US Thanksgiving holiday.

EGBS: Little Impact in Bunds From Soft Country-level Inflation Readings

Modest downside inflation risks stemming from this morning’s country-level flash readings have not provided much impulse to Bund futures, which are -15 ticks at 128.91. Gains in Bund futures since November 20 appear corrective, though the contract has traded through the 50-day EMA and is holding on to the bulk of its latest gains for now. Initial resistance is the November 26 high at 129.21.

- Note that market activity may be limited by the ongoing issues on the CME, with UST and S&P500 futures (amongst others) currently halted.

- Roll activity is now being seen in Eurex futures, with the Bund calendar spread active overnight and this morning.

- German yields are up to 1bp higher. The 5s30s curve is at 103bps, off Monday’s 106.7bp multi-week high.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels, with spread ranges narrow since Wednesday. Downside in the BTP/Bund and OAT/Bund spreads continue to be contained by the 70bp figure for now.

- This morning, French and Italian flash HICP printed below consensus, while there are slight downside risks to the German national print at 1300GMT.

- Today’s heavy data calendar has also seen final Q3 GDP readings from France (flash confirmed at 0.5%) and Italy (revised up a tenth to 0.1%), alongside the ECB’s consumer expectations survey (long-term inflation expectations steady).

GILTS: Curves Stabilise After Notable Flattening, Budget Remains Under Scrutiny

Gilt futures hold within yesterday’s range, with spill over from European national level CPI data limited as the market continues to assess the fallout stemming from the Budget.

- Contract last +6 at 91.56 vs. highs of 91.72.

- Initial support and resistance located at 90.53 at 91.93, bulls remain in technical control at this stage.

- Yields little changed vs. yesterday’s close.

- Curves stabilise around round numbers after Wednesday’s post-Budget flattening, 2s10s ~70bp, 5s30s ~130bp, following failure to break above 80bp and 145bp in recent weeks.

- Late on Thursday S&P warned that UK public finances remain constrained despite the measures outlined in the Budget, deeming the UK’s fiscal position to be “vulnerable” and a key constraint on the UK’s credit rating. The rating agency also highlighted risks to the fiscal consolidation plan, particularly towards the end of the forecast horizon.

- This mirrors ideas that we have outlined in our own work, with questions surrounding the likelihood of backloaded fiscal tightening being implemented trimming the post-Budget rally in gilts on Thursday.

- BoE-dated OIS little changed, pricing 22bp of easing for next month. SONIA futures flat to +2.0, implied terminal rate steady at ~3.35%.

- We still expect the BoE to cut rates next month and have outlined the feedthrough of the Budget into monetary policy in recent bullets.

- External cues are limited by the technical issues on the CME, which has halted Tsy futures trade for the best part of 8 hours.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.746 | -22.3 |

Feb-26 | 3.681 | -28.8 |

Mar-26 | 3.595 | -37.4 |

Apr-26 | 3.495 | -47.4 |

Jun-26 | 3.447 | -52.2 |

Jul-26 | 3.386 | -58.3 |

Sep-26 | 3.368 | -60.1 |

EQUITIES: E-Mini S&P Back Above 20-, 50-Day EMAs Following This Week's Recovery

The move higher in Eurostoxx 50 futures this week undermines a recent bearish theme and the contract is holding on to its gains. The contract has traded above the 20- and 50-day EMAs, signalling scope for a stronger recovery near-term. A continuation would open 5691.30 and 5742.40, Fibonacci retracement points. For bears, a reversal lower would instead expose the key S/T support and bear trigger at 5475.00, the Nov 21 low. S&P E-Minis are holding on to their latest gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed higher by 86.81 pts or +0.17% at 50253.91 and the TOPIX ended 9.87 pts higher or +0.29% at 3378.44.

- Elsewhere, in China the SHANGHAI closed higher by 13.336 pts or +0.34% at 3888.596 and the HANG SENG ended 87.04 pts lower or -0.34% at 25858.89.

- Across Europe, Germany's DAX trades lower by 11.58 pts or -0.05% at 23756.34, FTSE 100 higher by 16.88 pts or +0.17% at 9710.68, CAC 40 up 3.38 pts or +0.04% at 8102.85 and Euro Stoxx 50 down 2.37 pts or -0.04% at 5650.8.

- Dow Jones mini up 52 pts or +0.11% at 47542, S&P 500 mini up 7 pts or +0.1% at 6835, NASDAQ mini up 45.5 pts or +0.18% at 25347.75.

Time: 10:20 GMT

COMMODITIES: First Short-Term Bull Trigger for Gold at $4245.23

Recent weakness in WTI futures highlights a bearish theme. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. The contract has recovered from its latest low, resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. This allowed a recent overbought condition to unwind. Key support to watch lies at the 50-day EMA, at $3981.6. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude up $0.43 or +0.73% at $59.08

- Natural Gas up $0.09 or +2.02% at $4.65

- Gold spot up $15.39 or +0.37% at $4174.26

- Copper down $1 or -0.19% at $518.4

- Silver up $0.48 or +0.9% at $53.8493

- Platinum up $27.94 or +1.73% at $1642.19

Time: 10:20 GMT

| Date | GMT/Local | Impact | Country | Event |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1330/0830 | *** | GDP - Canadian Economic Accounts | |

| 28/11/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 28/11/2025 | 1330/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 28/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 28/11/2025 | 1600/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/11/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/11/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 01/12/2025 | 2200/0900 | ** | S&P Global Manufacturing PMI (f) |