FRANCE DATA: Q3 GDP Confirms Flash At 0.5% Q/Q, Domestic Demand Softer

Nov-28 09:36

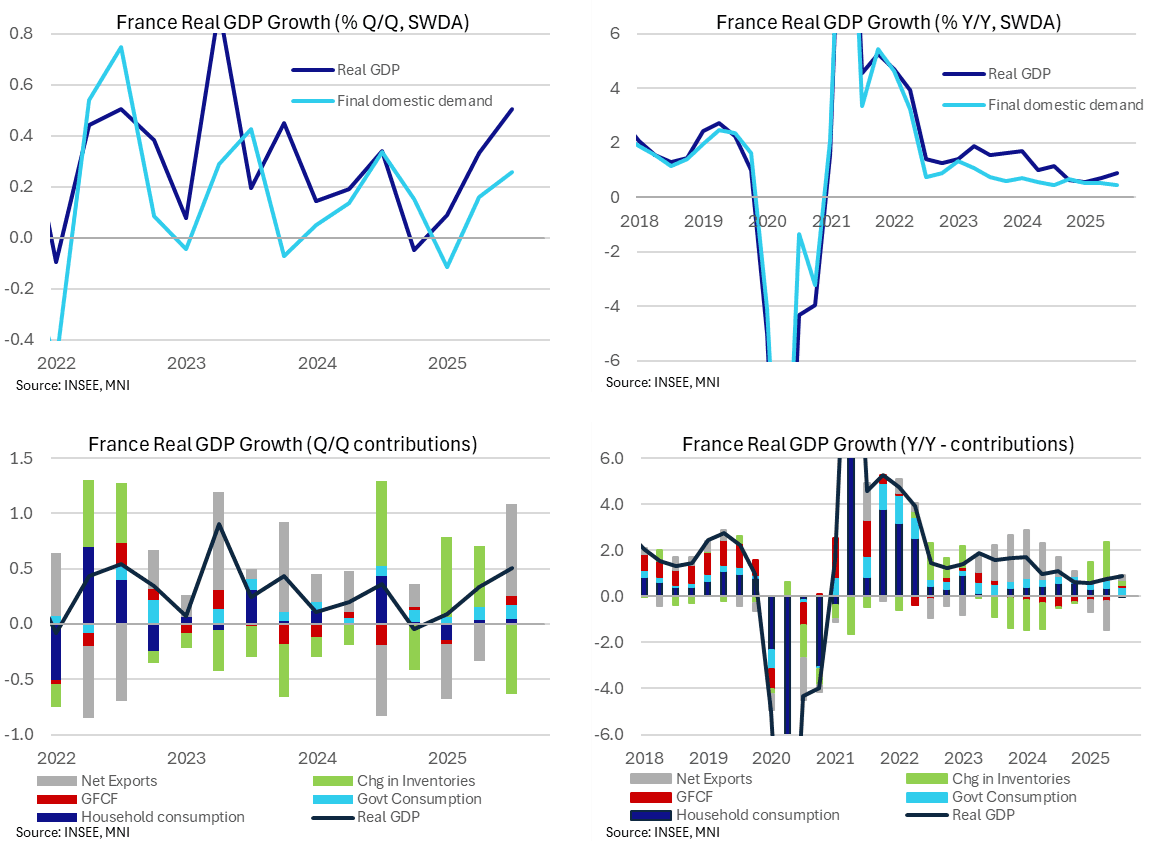

France Q3 final GDP confirmed flash estimates at 0.5% Q/Q for an acceleration from 0.3% in Q2, along with 0.9% Y/Y after a downward revised 0.7% (-0.1pp) in Q2. GDP growth has been picking up pace throughout 2025 after US-driven trade disruption in Q1, with this quarterly rate being the highest since Q2 2023. Final domestic demand continued to lag, however.

- Gross fixed capital formation grew 0.5% in Q3, after a flat print in Q2, "driven by the acceleration of GFCF in information and communications".

- Household consumption saw another slight increase of 0.1% (vs 0.1% Q2). "The decline in spending on food products (-1.0% vs 1.5% Q2) is more than offset by the rebound in spending on energy (1.3% vs -2.3% Q2) and by the increase in spending on services (0.1% vs 0.5% Q2)", notes INSEE.

- Inventories switched to a sizeable drag in Q3 of -0.35pps after tariff front-running saw a strong build worth an average 0.6pps through 1H25.

- For a better sense of underlying activity, final domestic demand increased 0.3% Q/Q in Q3 after 0.2% in Q2 and -0.1% in Q1, for its fastest pace since 3Q24. Final domestic demand held steady at 0.5% Y/Y meanwhile, where it's been for five of the past six quarters.

- Looking more broadly, comparing Q/Q growth rates, 2025 is broadly in line with last year, averaging 0.3% so far this year vs 0.2% 2024. The same comparison for Y/Y rates shows 2025 slightly weaker (averaging 0.8% vs 1.1% 2024), however a weak print in Q4 last year could point to a higher Y/Y rate in the next reading.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Supply Underpinning Yields; 10-year Gilt/Bund Close To YTD Low

Oct-29 09:34

- Impending sovereign supply is likely underpinning UK and German yields this morning, keeping the 10-year Gilt/Bund spread close to the 2025 low of ~177.5bps.

- The DMO will sell GBP3.75bln of the new 4.125% Mar-33 Gilt at 1000GMT. Meanwhile, Germany will sell E4.5bln of the 10-year 2.60% Aug-35 Bund at 1030GMT.

- The April low continues to contain downside in 10-year Gilts, which are currently little changed at 4.40%.

- Spanish Q3 flash GDP confirmed expectations at 0.6% Q/Q (vs 0.8% prior), but domestic demand signals were solid. UK September consumer credit was in line with expectations.

- The EFSF has sent an RFP for an upcoming transaction, which will likely be held early next week.

- In the Eurozone, focus remains on the ECB decision (Thurs), Eurozone Q3 flash GDP (Thurs) and October flash inflation (Fri). In the UK, spillover from US Treasuries amid today’s FOMC decision will be eyed alongside ongoing budget headline flow.

MNI: UK BOE SEP MORTGAGE APPROVALS 65,944

Oct-29 09:30

- MNI: UK BOE SEP MORTGAGE APPROVALS 65,944

- UK BOE SEP SECURED LENDING GBP5.49 BLN

- UK BOE SEP CONSUMER CREDIT GBP1.49 BLN

MNI: UK SEP M4 MONEY SUPPLY +0.6% M/M, +3.6% Y/Y

Oct-29 09:30

- MNI: UK SEP M4 MONEY SUPPLY +0.6% M/M, +3.6% Y/Y