MNI US Macro Weekly: Soft Labor Surprises Precede Payrolls

Feb-06 21:19By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- January’s Employment Report may have been pushed back to Feb 10 due to the brief federal government shutdown, but in the meantime there was plenty of labor market data to chew on this week.

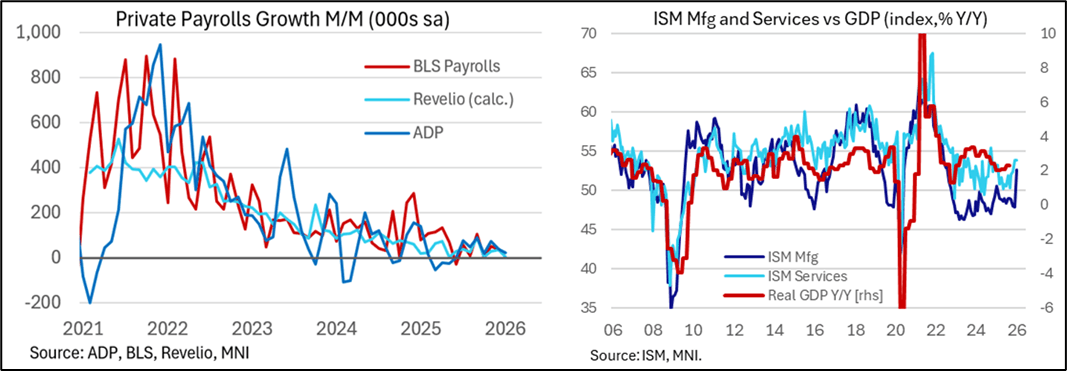

- Most of it was weaker than expected, including ADP payrolls and Revelio Labs payrolls, Challenger job cuts and hiring announcements, JOLTS job openings, and the latest weekly initial jobless claims.

- There are mitigating explanations (JOLTS doesn’t line up with private sector estimates so may bounce in January; jobless claims look impacted by severe weather), but overall theme of a lower hiring and lower firing (with the exception of the Challenger data) labor market easily remains intact.

- That remains in divergence with the continued solidity in the latest activity data, with ISM Manufacturing soaring (highest since Aug 2022) and Services putting in another solid print (joint-15 month high).

- The flawed UMichigan survey suggested that consumer sentiment has bottomed, while the latest credit indicators appeared to show slight acceleration. Latest retail sales metrics are solid if somewhat mixed.

- Rate markets largely tracked the bifurcation in data. Strong ISMs saw Fed easing potential fade early in the week, but there was a reversal in a more dovish direction by week-end alongside the soft labor data and tech-led equity weakness exacerbating negative risk sentiment.

- Fed Funds futures at one point implied 63bp of cuts to end-2026. That has since pulled back closer to 55bp with some stabilization in risk assets and a subsequent boost from U.Mich consumer sentiment firming.

- FOMC speakers were mostly patient on the next move, including increasingly cautious-sounding Board members Cook and Jefferson, with non-voter Daly one of the few flying the dovish flag.

- In general there’s a sense that the economy is resilient with downside labor market risks in relative check, with more evidence required that inflation is converging to 2% before declaring victory on inflation.

- We’ll all be watching the two major releases next week with January reports for nonfarm payrolls (Wed) and CPI (Fri), with Retail Sales on Tuesday also bearing watching (but it’s only for December).

- Monthly payrolls growth is currently expected at 70k in January for a slight acceleration from the 50k in December. The market likely currently views that to be on the high side considering a swathe of soft labor indicators this past week. The unemployment rate will again be a key component in shaping reaction to the report, with consensus currently looking for 4.4% after the 4.38% in December.

- As for CPI inflation, January is always an important month as it begins to capture start-of-year price resets - historically about 20% net price increases for the year come in January and another 20% in February. Consensus currently stands at 0.3% M/M for both headline and core CPI in the early days for the Bloomberg survey.