POWER: GERMAN POWER FOR AUG. 22 SETTLES AT EU 63.04 /MWH: EPEX AUCTION"-bbg

Aug-21 10:50

- The German day-ahead spot settled at €63.04/MWh from €52.62/MWh on the previous day.

FRENCH POWER FOR AUG. 22 SETTLES AT EU 36.70 /MWH: EPEX AUCTION

- The French day-ahead spot cleared at €36.70/MWh from €39.29/MWh on the previous day.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

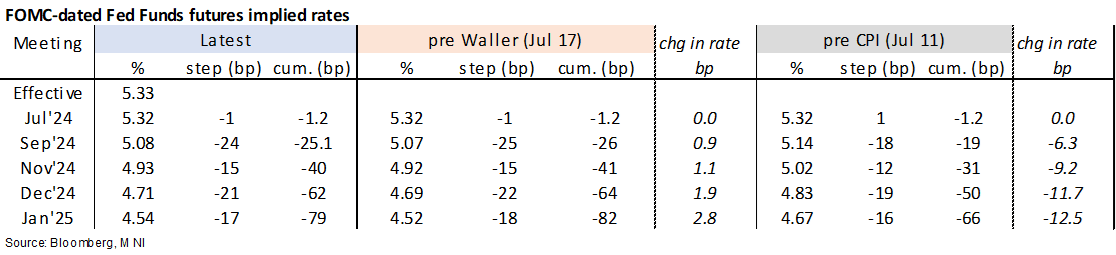

STIR: Marginal Increase In Fed Rates After Biden Withdrawal and PBOC Rate Cut

Jul-22 10:33

- Fed Funds implied rates are unchanged for July and September meetings and beyond that just 0.5bp higher in an extension of Friday’s increase.

- The PBOC surprisingly cutting its seven-day reverse repo rate is one factor at play whilst investors continue to grapple with implications from Biden ending his re-election campaign.

- Cumulative cuts from 5.33% effective: 1bp Jul, 25bp Sep, 40bp Nov, 62bp Dec and 79bp Jan.

- It follows last week’s almost clean sweep of stronger than expected data but one that was overshadowed by the prior week’s CPI/PPI plus Powell’s comments on greater dual mandate progress.

- Ahead of today’s particularly light docket with the FOMC in media blackout, see the latest macro recap here.

EQUITIES: Tech Bounce Aids Recovery Off Last Week's Lows

Jul-22 10:31

- The e-mini S&P inches to a new daily high as markets continue to reverse the Friday leg lower, but the index will need a further 30 points to challenge the Friday high. A close higher today would snap the losing streak posted off the Tuesday cycle high at 5721.25 - intraday levels of note include 5631.62.

- It's unlikely Biden's withdrawal from the race has triggered the recovery off lows for equities this week - betting markets have shifted slightly to acknowledge Harris' nomination and likely candidacy, but Trump's comfortable lead remains - and news of Biden's stepping down across the tail-end of last week did little to prop up headline indices.

- Outperformance in tech names (the laggards and drivers of the sell-off last week) are bouncing well: the NASDAQ-100 mini is higher by 0.8%, while Europe's tech sector in the Stoxx600 leads, higher by 1.3% at pixel time.

- Earnings season continues apace this week, with Tuesday particularly busy - highlights include:

Monday - Verizon

Tuesday - General Motors, Lockheed Martin, Coca-Cola, General Electric, Visa, Alphabet, Tesla

Wednesday - AT&T, IBM, Ford

Thursday - AbbVie, American Airlines, Baker Hughes

LOOK AHEAD: Monday-Tuesday Data Calendar: Regional Fed Data, Existing Home Sales

Jul-22 10:19

- US Data/Speaker Calendar (prior, estimate)

- Jul-22 0830 Chicago Fed Nat Activity Index (0.18, -0.09)

- Jul-22 1130 US Tsy $76B 13W, $70B 26W Bill auctions

- --

- Jul-23 0830 Philly Fed Non-Mfg Activity (2.9, --)

- Jul-23 1000 Richmond Fed Mfg Index (-10, -7)

- Jul-23 1000 Richmond Fed Business Conditions (-11, --)

- Jul-23 1000 Existing Home Sales (4.11M, 3.99M)

- Jul-23 1000 Existing Home Sales MoM (-0.7%, -3.0%)

- Jul-23 1130 US Tsy $70B 42D CMB Auction

- Jul-23 1300 US Tsy $69B 2Y Note auction (91282CLB5)