MNI ECB Preview: Euro Intrigue Fades But Not Entirely

Feb-03 17:42By: Chris Harrison and 1 more...

BundsGermanyEUR/USD

Hidden PDF

Executive Summary

- The ECB is again fully expected to leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff.

- There have been both slightly dovish and slightly hawkish developments in January, which should guard against President Lagarde sending too strong a signal in either direction at the press conference. Expect renewed uncertainty to feature.

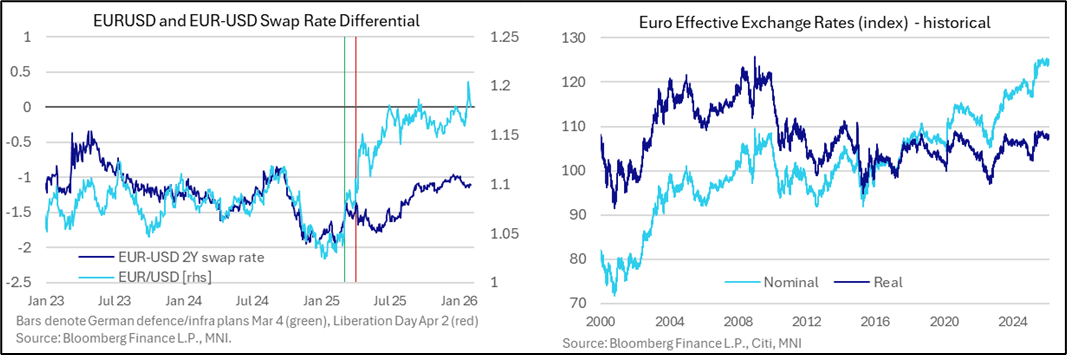

- Q&A focus will no doubt be on recent euro appreciation, even if it looks softer in trade-weighted terms and has given back some of its recent increases.

- We estimate that the disinflationary impulse from recent currency moves are offset by commodity price increases when projecting on from the December projections.

- That said, with those projections already seeing a modest core inflation undershoot in 2027, expect sensitivity to any further downward pressure.

- We’re still to receive the flash January HICP report tomorrow (Wednesday) on day one of the two-day ECB meeting, an important report in that it captures some start-of-year price resets. Country-level data imply differing degrees of disinflation.

- Only 2 of 27 analysts expect rate cuts this year, neither of which look for a cut with this meeting. A clear majority look for rates on hold through 2026 although 2 also look for an end-2026 25bp hike.

- We approach this meeting with a mild easing bias again (4bp through Sept) after a brief hiking bias in Dec.

A short-lived surge higher in EURUSD drew a reaction from various GC members:

Trending Top

Jun-26 16:22