EUROPEAN INFLATION: MNI Projects 2.3-2.4% Y/Y German National CPI, Core 2.8%

From state-level data that equates to 89.1% weighting of the national November flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.3-2.4% Y/Y (2.3% prior) and fell around 0.2-0.3% M/M. See the tables below for full calculations.

- Analyst consensus stands at 2.4% Y/Y and -0.2% M/M, risks to consensus therefore appear to be skewed slightly to the downside.

- Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies around 2.8% Y/Y (2.8% prior). Analysts have expected core to be roughly unchanged to slightly higher this time.

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is generally the same.

| Y/Y | November (Reported) | October (Reported) | Difference |

| North Rhine Westphalia | 2.3 | 2.3 | 0.0 |

| Hesse | 2.5 | 2.4 | 0.1 |

| Bavaria | 2.2 | 2.2 | 0.0 |

| Brandenburg | 2.6 | 2.6 | 0.0 |

| Baden Wuert. | 2.3 | 2.3 | 0.0 |

| Berlin | 2.5 | 2.3 | 0.2 |

| Saxony | 2.2 | 2.1 | 0.1 |

| Rhineland-Palatinate | 2.0 | 1.9 | 0.1 |

| Lower Saxony | 2.2 | 2.2 | 0.0 |

| Saarland | 2.2 | 2.2 | 0.0 |

| Saxony-Anhalt | 2.6 | 2.7 | -0.1 |

| Weighted average: | 2.33% | for | 89.1% |

| M/M | November (Reported) | October (Reported) | Difference |

| North Rhine Westphalia | -0.3 | 0.4 | -0.7 |

| Hesse | -0.2 | 0.3 | -0.5 |

| Bavaria | -0.2 | 0.3 | -0.5 |

| Brandenburg | -0.2 | 0.4 | -0.6 |

| Baden Wuert. | -0.3 | 0.3 | -0.6 |

| Berlin | -0.2 | 0.2 | -0.4 |

| Saxony | -0.2 | 0.3 | -0.5 |

| Rhineland-Palatinate | -0.1 | 0.2 | -0.3 |

| Lower Saxony | -0.2 | 0.2 | -0.4 |

| Saarland | -0.2 | 0.2 | -0.4 |

| Saxony-Anhalt | -0.2 | 0.2 | -0.4 |

| Weighted average: | -0.24% | for | 89.1% |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

TARIFFS: US Lowering Auto Tariffs On South Korea

"US AUTO TARIFFS WILL BE LOWERED TO 15%: SOUTH KOREA" Bloomberg

"*US WILL CONTINUE 15% OF ACROSS THE BOARD TARIFFS: S.KOREA" Bloomberg

GREECE T-BILL AUCTION RESULTS: 13-Week GTB

| Type | 13-week GTB |

| Maturity | Jan 30, 2026 |

| Amount | E500mln |

| Target | E500mln |

| Previous | E500mln |

| Avg yield | 1.72% |

| Previous | 1.78% |

| Bid-to-cover | 2.36x |

| Previous | 1.99x |

| Previous date | Oct 01, 2025 |

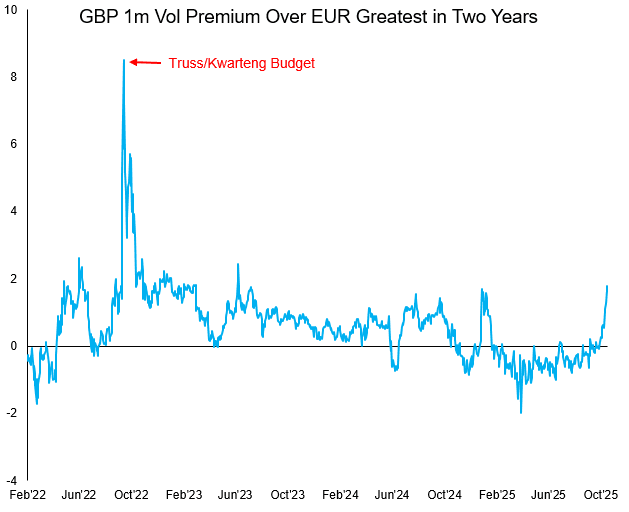

GBP: Vol Markets Signalling Significant GBP Vol Premium Into Budget

The pick-up in spot volatility this week has helped support implied at the margins, with the 1m contract (capturing the UK Autumn Budget on November 26th) rising back above 7 points to provide a decent premium over shorter-dated contracts that expire before the Budget.

While vols above 7 points look unimpressive in isolation, relative to EURUSD the move is extreme. The GBP 1m vol premium over EUR is now near 2 points and the widest since 2023 - signalling markets assigning a greater risk premium to GBP despite the background low vol regime.

We write on the latest expectations for the UK Budget in the Gilt Week Ahead here: https://media.marketnews.com/Gilt_Week_Ahead20251027_14ac41803e.pdf

And summarise the key drivers of GBP spot weakness here:

- Speculation that Reeves will break a manifesto pledge and raise income tax has been bolstered by the FT's reporting on a sizeable productivity estimate cut triggering a broader financing need.

- Higher income taxes would contain consumption, helping smooth the path for faster BoE rate cuts across 2026 (and potentially by the end of 2025).

- Food inflation remains a key driver of inflation expectations (e.g. Just this week: The Times: '‘Shrinkflation’ of supermarket staples rife on British high streets', BBC: 'Businesses face 'rising costs and staffing pressures''), however Tuesday's BRC-NIQ shop price data suggests we have passed the peak in food price gains.

- Food price inflation is particularly important given how well supported it has been this year via both higher employer's NIC contributions as well as incoming packaging taxes, but today's numbers endorse the step lower in ONS food inflation and may suggest inflation expectations will follow.