ITALY DATA: Tepid Consumption Trends Take Shine Off Upwardly Revised Q3 GDP

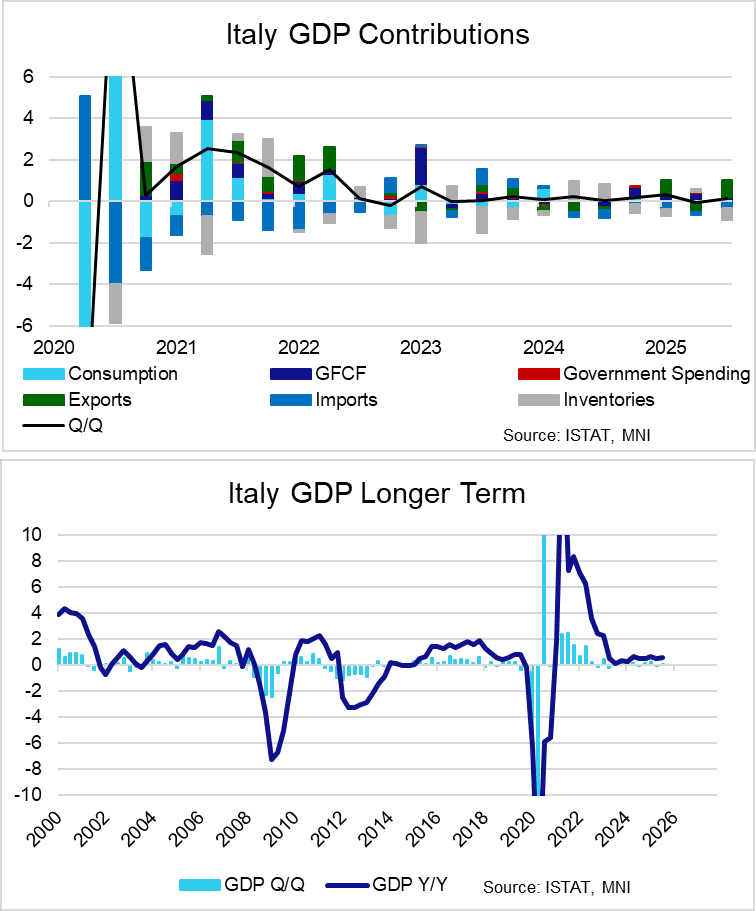

Italian Q3 GDP was revised up a tenth to 0.1% Q/Q (vs -0.1% prior), and is now back in line with the original consensus for the flash release. Details suggest inventories were a large drag in Q3, but weak household consumption trends remain a concern. We continue to think that the biggest risk to continued Italian fiscal consolidation (and by extension BTP/Bund spread tightening) is the growth outlook. While a cyclical recovery is expected over the coming years, fading EU RRP disbursements and a weak potential growth picture remain medium-term fragilities.

- As anticipated from the limited flash release details, net exports made a positive contribution to sequential growth. Exports rose 2.6% Q/Q (vs -1.7% prior), while imports rose 1.2% Q/Q (vs 0.4% prior). The export performance suggests Italian producers have recovered well from the trade-war/tariff induced drag in Q2.

- Household consumption was tepid, rising just 0.1% Q/Q. Despite a low unemployment rate and positive real wage growth, households remain cautious. It is hoped that middle-class tax cuts announced in the 2026 budget will help to stimulate consumption next year.

- Gross fixed capital formation rose 0.6% Q/Q (vs 1.5% prior). A 1.4% pullback in dwelling investment was offset by increases in machinery and equipment (2.5%) and transport (4.5%).

- Government spending made a neutral contribution for the second consecutive quarter, rising 0.2% Q/Q. Italy hopes to continue running primary surpluses in the coming years in order to exit the EU’s excessive deficit procedure and reduce its debt burden

- Inventories pulled down sequential GDP growth by almost 0.6pp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 2.87bn at 1.1600/1.1650.

AUDUSD 1.83bn at 0.6530 (a little far).

EURUSD ~1bn at 1.1650 (thu).

USDCAD 2.42bn at 1.4015/1.4025 (thu).

USDJPY 1.15bn at 152.50 (fri).

EURUSD ~1bn at 1.1640 (tue).

- EURUSD: 1.1600 (637mln), 1.1615 (346mln), 1.1640 (651mln), 1.1650 (1.24bn), 1.1670 (679mln), 1.1675 (282mln).

- USDJPY: 152.50 (299mln).

- USDCAD: 1.3970 (470mln).

- AUDUSD: 0.6530 (1.83bn).

- USDZAR: 17.1500 (210mln).

BONDS: Supply Underpinning Yields; 10-year Gilt/Bund Close To YTD Low

- Impending sovereign supply is likely underpinning UK and German yields this morning, keeping the 10-year Gilt/Bund spread close to the 2025 low of ~177.5bps.

- The DMO will sell GBP3.75bln of the new 4.125% Mar-33 Gilt at 1000GMT. Meanwhile, Germany will sell E4.5bln of the 10-year 2.60% Aug-35 Bund at 1030GMT.

- The April low continues to contain downside in 10-year Gilts, which are currently little changed at 4.40%.

- Spanish Q3 flash GDP confirmed expectations at 0.6% Q/Q (vs 0.8% prior), but domestic demand signals were solid. UK September consumer credit was in line with expectations.

- The EFSF has sent an RFP for an upcoming transaction, which will likely be held early next week.

- In the Eurozone, focus remains on the ECB decision (Thurs), Eurozone Q3 flash GDP (Thurs) and October flash inflation (Fri). In the UK, spillover from US Treasuries amid today’s FOMC decision will be eyed alongside ongoing budget headline flow.

MNI: UK BOE SEP MORTGAGE APPROVALS 65,944

- MNI: UK BOE SEP MORTGAGE APPROVALS 65,944

- UK BOE SEP SECURED LENDING GBP5.49 BLN

- UK BOE SEP CONSUMER CREDIT GBP1.49 BLN