SWITZERLAND DATA: Q3 GDP Unrevised, Net Exports Drag Heavily

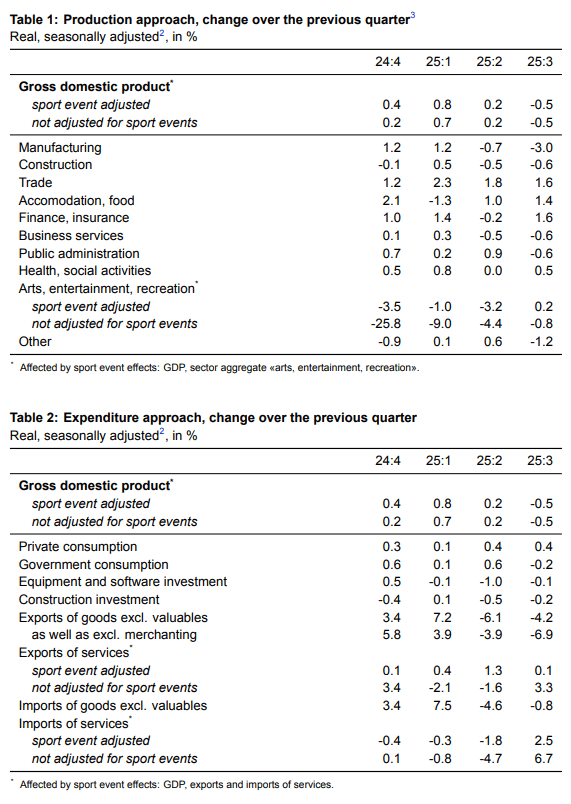

Swiss GDP growth was unrevised in the final Q3 release at a very weak -0.5% Q/Q on a sports-event and seasonally-adjusted basis, following Q2's 0.2% (upwardly revised by 0.1pp). "The negative result is largely down to the chemical and pharmaceutical industry, where strong exports gave way to a compensatory decline. Below-average growth in the services sector failed to offset the downturn in the industrial sector.", SECO comments.

- While undoubtedly weak, we do not see how the (singular) print should move the needle for the SNB, which views its monetary policy already as "accommodative". This applies especially as a key obstacle in Q3, the 39% tariffs on exports to the US, have now been mitigated for the most part. Downside pressure on inflation for continued headline CPI readings below 0% would likely be needed to put an SNB cut below 0% firmly on the table again.

- Across an expenditure split, goods exports stand out negatively, seeing the second consecutive negative quarter at -4.2% Q/Q (excl. valuables) after US tariff front-running supported here in H1. Elsewhere, government consumption as well as investment contracted marginally in Q3, while private consumption expanded by 0.4% sequentially. See tables below for details.

Separately, the Swiss KOF index slightly outperformed expectations in November at 101.5 (101.0 consensus) to hold steady after 101.5 in October (initially 101.3). "The positive developments are particularly reflected by the demand side indicators included in the KOF Economic Barometer. Both the indicator bundles for foreign demand as well as for private consumption show a favourable outlook. Among the production side indicator bundles, the indicators for financial and insurance services and for construction are under pressure.", KOF comments on drivers.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: SPAIN Q3 FLASH GDP +0.6% Q/Q, +2.8% Y/Y (VS +0.8% Q/Q, +3.0% Y/Y Q2)

- MNI: SPAIN Q3 FLASH GDP +0.6% Q/Q, +2.8% Y/Y (VS +0.8% Q/Q, +3.0% Y/Y Q2)

GILTS: Opening Calls

- Gilt Calls, a tight 93.73/93.74.

Although be aware of the downside continuation in the Pound, potential upside risk?

EQUITIES: EU Cash Opening Calls - some focus on Banks

Some potential focus on the Banks, Santander (most weighted on the SX7E), Deutsche and UBS all beat expectations earlier.

- Calls: Estox 50: +0.03%, Dax: -0.11%, CAC: -0.13%, FTSE +0.39%, SMI +0.02%.