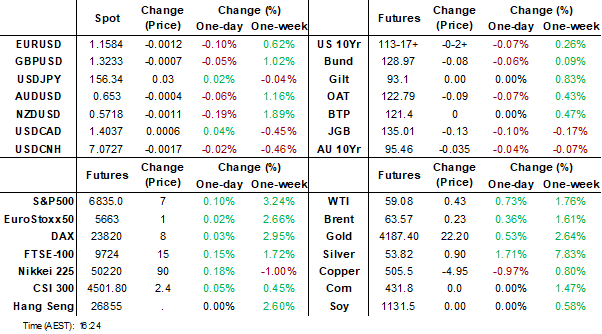

MNI EUROPEAN MARKETS ANALYSIS: Slow Finish to Month End

- Risk appetite remains underpinned by hopes of rate cuts with most major equity bourses finishing with modest gains Friday, whilst capping off a generally weak month. China's stocks have the overhang of a potential further property developer default, news of which have prompted suggestions from local press that further policy support maybe forthcoming.

- With the Thanksgiving holiday in the US truncating trading, bond markets were slow leading into month end and news flow slower. Key data out in Japan was generally positive, as the Japanese market turns its attention to a speech by BOJ Governor Ueda Monday.

- Ahead we have Sweden, Finland, Swiss, France, Czech GDP, Germany Retail Sales and Unemployment and CPI from France and Spain. Whilst the US markets reopen tonight, expectations are for a modest day with no treasury auctions and no tier 1 data releases.

MARKETS

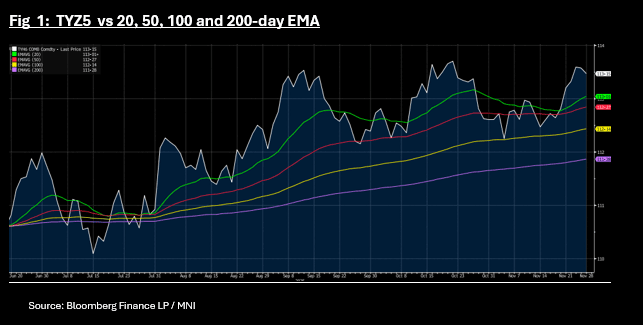

US TSYS: Bond Futures Down; 10-Yr UST Back Above 4%

US bond futures had a low volume day today as expected with the 10-Yr down -03 at 113-15+. TYZ5 maintains its position above all moving averages with the 20-day EMA below at 113-01+ and up for the week by +0-10.

Cash is lower with yields 1-1.5bps higher across the curve. The movement higher in yield takes the 10-Yr back above 4.00%. This is the fourth time over the last two months the 10-Yr has traded below the 4.00% level, but has been unable to maintain it there for very long.

- The US 2-Yr is at 3.495% - +1.6bps

- The US 5-Yr is at 3.579% - +0.9bps

- The US 10-Yr is at 4.013% - +1.7bps

- The US 30-Yr is at 4.658% - +1.5bps

It is widely anticipated that the market will remain quiet overnight with no auctions scheduled until next week, or economic data releases.

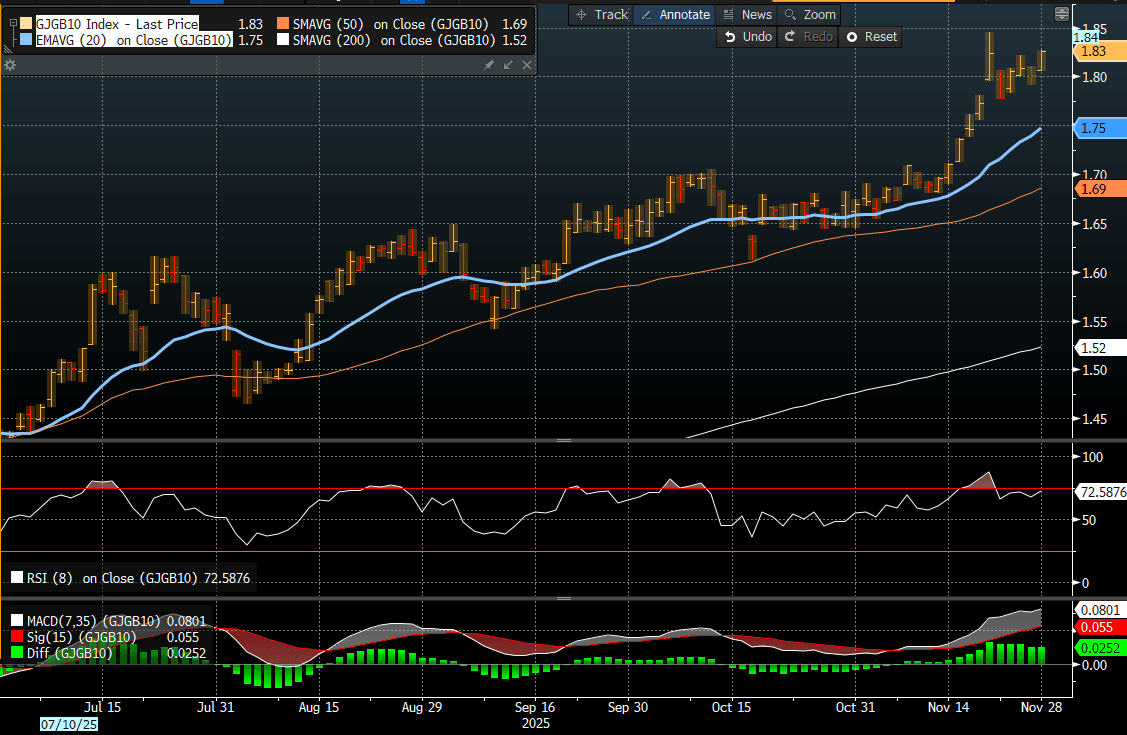

JGBS: Cheaper With 10Y Leading, 10YY Back At Cycle Highs

JGB futures are weaker, -17 compared to settlement levels.

- The 2-year bond auction delivered weak results today. The low price cleared below the Bloomberg-surveyed forecast of 100.05, while the cover ratio dropped to 3.5310x from 4.4665x. The tail also lengthened to 0.012 from 0.002 last month.

- Reuters reported yesterday that the Japanese government will increase issuance of 2-year and 5-year JGBs from January, with around ¥100bn of additional supply in each tenor. There are no changes expected for 10–40-year issuance.

- Japan's Nov Tokyo CPI print was fairly close to market expectations.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session, but volumes have been light given Thursday's Thanksgiving Day Holiday.

- Cash JGBs are flat to 2.5bps across benchmarks, with the 10-year underperforming. The benchmark 10-year yield is 2.5bps higher at 1.826% versus the cycle high of 1.84%. (see chart)

- Swap rates are 1-2bps higher.

- Tomorrow, the local calendar will see Q3 Capital Spending, Q3 Company Sales and S&P Global PMI Mfg alongside a BOJ Governor Ueda Speech in Nagoya.

Source: Bloomberg Finance LP

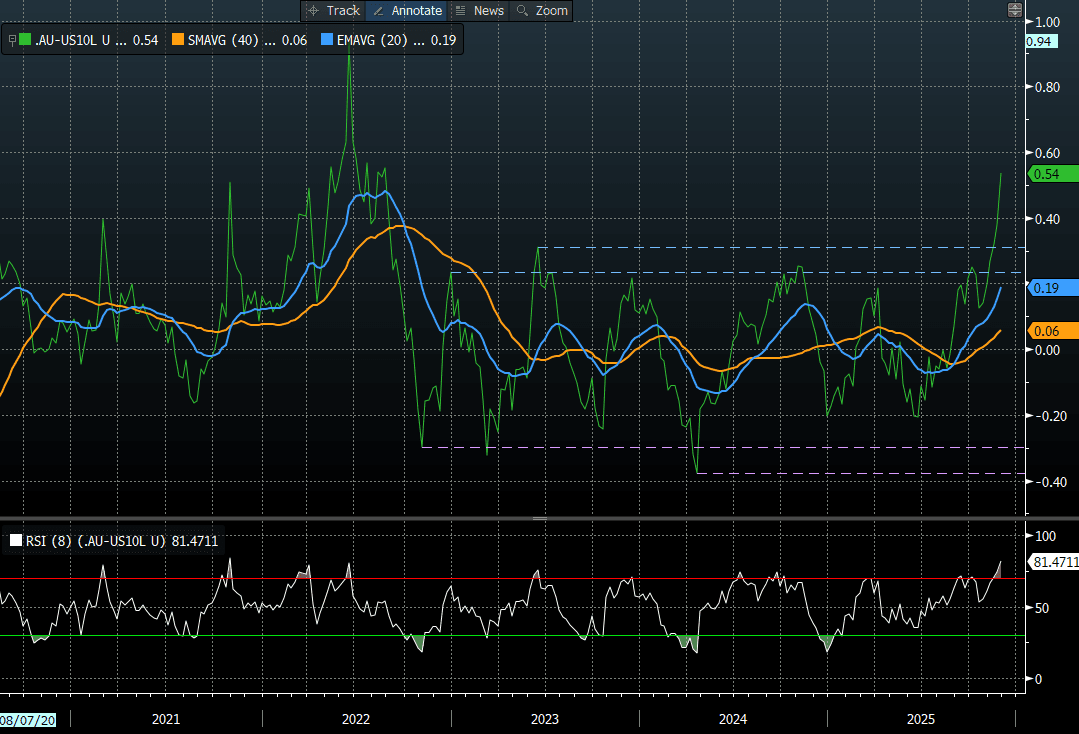

AUSSIE BONDS: Cheaper, AU-US 10Y Diff Keeps Pushing Wider

ACGBs (YM -4.5 & XM -3.0) are cheaper and hovering near session lows.

- Private credit rose 0.7% m/m (estimate +0.6%) in October versus +0.6% in September. Private credit rose 7.3% y/y versus a revised +7.2% in September.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session, but volumes have been light given Thursday's Thanksgiving Day Holiday.

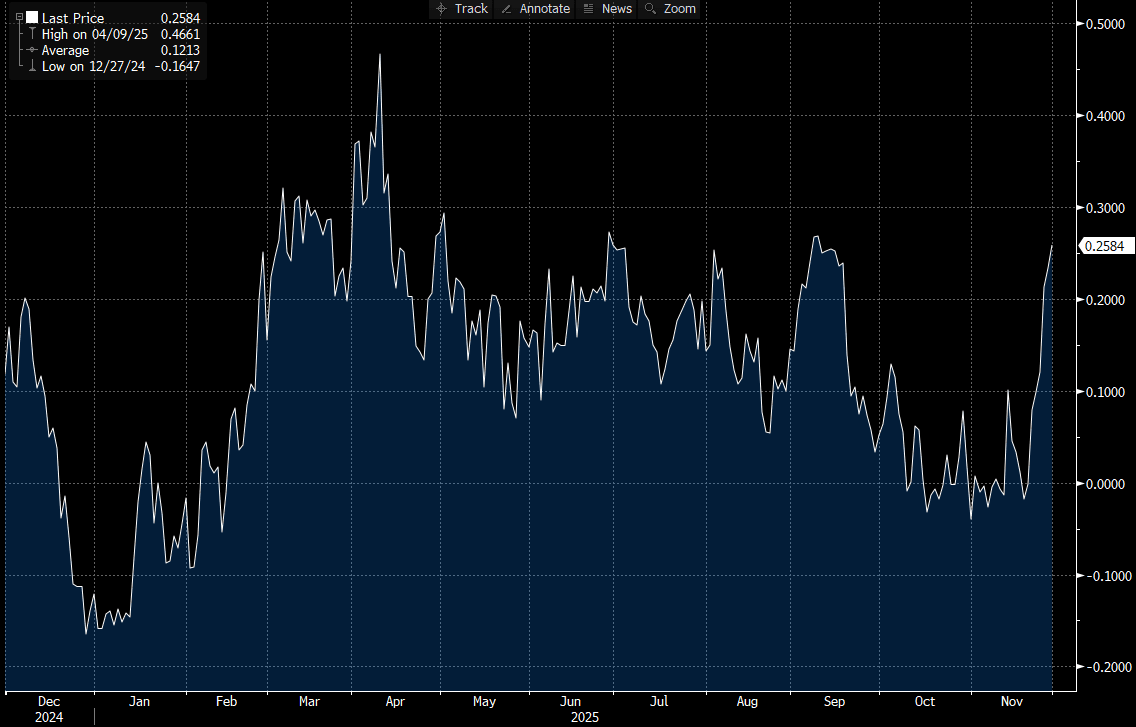

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +52bps. Today’s move has extended the differential’s push above the ±30bps range that had persisted since November 2022 (see chart).

- The bills strip is -2 to -6 across contracts, with a steepening bias.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 0% probability. Notably, the market has shifted to giving a 44% probability to 25bp easing by December 2026.

- On Monday, the local calendar will see Cotality Home Values, S&P Global PMI Mfg, Melbourne Institute Inflation, and ANZ-Indeed Job Advertisements monthly data, and Q3 Company Operating Profit and Inventories.

- Next week, the AOFM plans to sell A$1000mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Sell-Off Extends, NZ-US 10Y Diff 25Bps Wider In 10 Days

NZGBs closed cheaper, with the benchmark yields 2-7bps higher, led by the 5-year. After today’s move, yields are 11-24bps higher than Wednesday’s pre-RBNZ Decision levels.

- Updated projections by the RBNZ showed the OCR at 2.25% in Q1 (with only one meeting in the quarter on 18 February), then 2.20% in Q2 and 2.23% in Q3, implying the RBNZ is effectively on hold if the economy evolves as expected. The profile maintains optionality, and outgoing Governor Hawkesby emphasized that the 2.20% projection reflects an easing bias.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session, but volumes have been light given Thursday’s Thanksgiving Day Holiday.

- The NZ-US 10-year yield differential widened again today, albeit by 1bp, to +25bps. For context, the differential was around flat 10 days ago. (see chart)

- Swap rates closed 6-9bps higher.

- RBNZ-dated OIS pricing closed little changed across meetings. 2bps of easing remains priced for February, while November 2026 has 29bps of tightening priced.

- On Monday, the local calendar will see Building Permits data.

Bloomberg Finance LP

NEW ZEALAND: RBNZ Model Pointing To Positive Q3/Q4 Growth, But Modest Y/Y Pace

The RBNZ nowcaster for Q3 and Q4 GDP has ticked higher this week. For Q3 it sits at 0.79%q/q, which is the highest estimate for the quarter (since the nowcaster started back on Jun 20). The biggest contributor this week has been the retail sales print. Recall that Q2 growth fell by -0.9%. We get the Q3 update on Dec 18. The Q4 estimate rose to 0.47%, from 0.40% the week prior. The biggest contributor to the Q4 rise estimate was this week's survey data (with both the ANZ business and consumer sentiment readings posting solid gains).

- If such outcomes are realized it would push NZD GDP y/y growth to just above 1.2% for both Q3 and Q4 of this year. This would have us back around the pace seen in late 2023/early 2024. The Q2 outcome was -0.6%y/y.

- This is still below longer run averages for y/y growth, which are closer to 2.5-2.6%.

- Our policy team noted yesterday: "Risks to the Reserve Bank of New Zealand’s 2.25% Official Cash Rate remain balanced, with policy likely to stay on hold for the foreseeable future and a hike in the near term highly unlikely, Chief Economist Paul Conway told MNI, emphasising that the RBNZ retains full flexibility to adjust rates in either direction depending on economic developments."

US: CME Trading Impacted By Data Center Issue, Multiple Markets Impacted

Headlines have crossed from both Rrts and BBG that trading has stopped in CME futures, due to a data center glitch. US equity futures were holding a touch higher before trading was halted. (Eminis were up 0.10%, Nasdaq futures +0.18%).

- Via RTRS: "NO TRADES ON S&P 500 FUTURES, NASDAQ 100 FUTURES SINCE 0344 GMT - LSEG DATA" It adds: "Support is working to resolve the issue in the near term and will advise clients of Pre-Open details as soon as they are available," CME said in a statement.

- BBG notes: "Contracts including crude oil and palm oil were affected in Friday morning trading in Asia. Most recent trades for the US West Texas Intermediate oil contract were seen at 10:47 a.m. Singapore time." WTI was at $59.08/bbl then.

- It also quotes traders who stated that FX trades on the EBS platform have been impacted.

- Broader FX trends have been relatively steady in the G10 space, with slightly higher USD index levels. This follows the US overnight session, where markets were out due to Thanksgiving.

FOREX: USD - BBDXY Move Lower Stalls Toward 1218

The BBDXY has had a range today of 1218.76 - 1220.19 in the Asia-Pac session; it is currently trading around 1219, +0.05%. A very subdued Friday Asian session for currencies to end the week. This week the standout has been the huge bounce in global risk together with a repricing of more potential US rate cuts. The USD has played catch up to this but has found some bids initially around the 1218 area overnight stalling the move in a quiet overnight session thanks to the US being off. On the day I suspect a range of 1218-1224 should cover a subdued end of the week as we move back toward the middle or lower end of the 1210-1230 range, first support seen toward 1218 and then the 1208-1214 area.

- EUR/USD - Asian range 1.1582 - 1.1602, Asia is currently trading 1.1590. The pair is consolidating just below 1.1600. On the day I suspect dips could now be supported first up as the market tries to work through the resistance around 1.1600-25, above here and the focus could turn back toward the 1.1700 area.

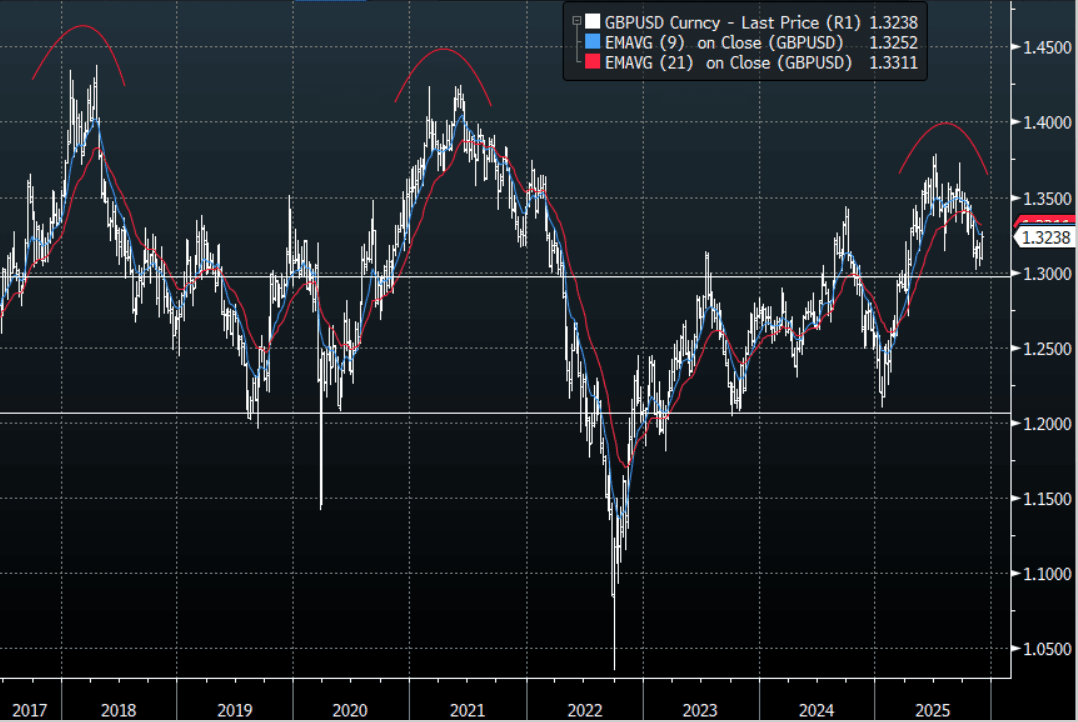

- GBP/USD - Asian range 1.3229 - 1.3245, Asia is currently dealing around 1.3240. The pair is consolidating its recent gains around 1.3250. I remain skewed toward shorts but I feel this move does signal the need to be patient as it could first move a little higher. I will be watching the price action back toward 1.3300-1.3400 for signs of a top should we get back up there.

- Cross asset : SPX +0.40%, Gold $4185, US 10-Year 4.006%, BBDXY 1219, Crude Oil $59.10

- Data/Events : Germany Retail Sales/Unemployment Change/CPI, France CPI/PPI/GDP, Spain CPI/Retail Sales/Current Account Balance, EZ ECB 1&3 Yr CPI Expectations, Italy GDP/CPI

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

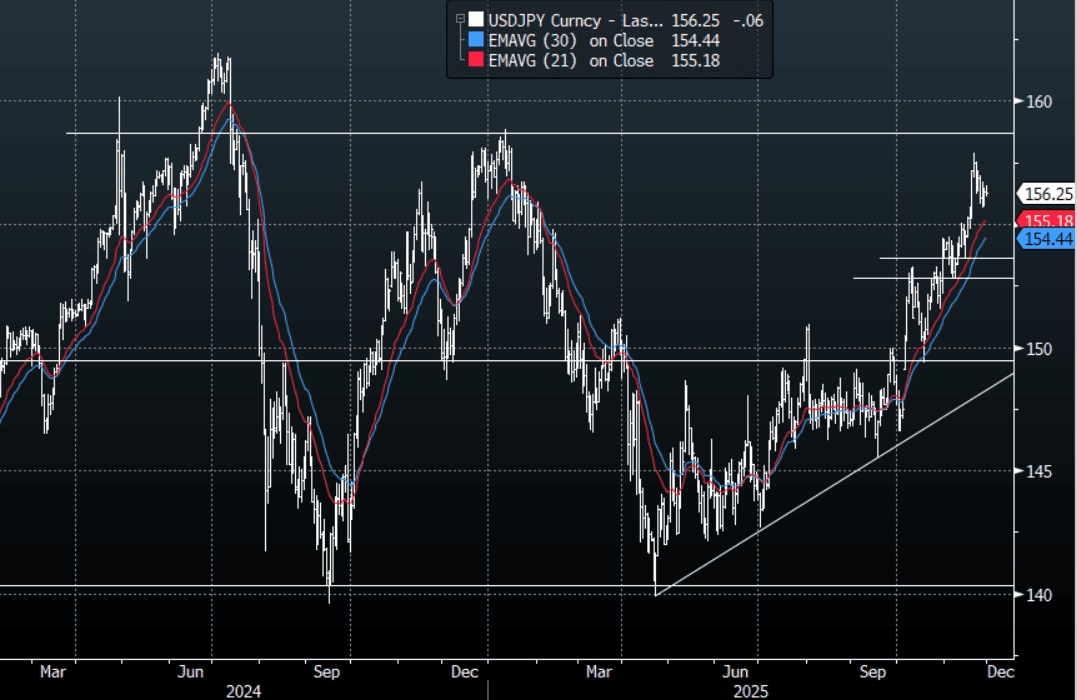

JPY: USD/JPY - Holding Above 156.00, Support Back Towards 154-155

The USD/JPY range today has been 156.10 - 156.58 in the Asia-Pac session, it is currently trading around 156.20, -0.05%. The pair has traded sideways in a very subdued session. The move in the Yen looks like it might force the BOJ into action in December and we now have the market pricing in imminent cuts in the US. This could have an impact or at least slow what looked like a situation that was about to get out hand. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 154-155 area which I suspect would be bought at first. Look for the consolidation to continue as the market contemplates if these moves by central banks are going to be enough to challenge the weakening Yen trajectory.

- MNI AU - Nov Tokyo CPI Close To Forecast, Services Y/Y Steady At 1.56% y/y: Japan's Nov Tokyo CPI print was fairly close to market expectations. Headline rose 2.7%y/y, in line with the consensus (while the Oct outcome was also revised down to this level, from 2.8%). Ex fresh food and energy printed 2.8%y/y (a touch above the 2.7% forecast), while the ex fresh food, energy measure was 2.8%y/y, in line with the prior and consensus forecast for today. We are off earlier 2025 highs, but remain close to 3%.

- MNI AU - Job-To-Applicant Ratio Downtrend Continues, Risking Higher U/E Rates: Japan Oct jobless rate and job to applicant ratio figures were weaker than expected. The unemployment rate held steady at 2.6%, against a market forecast of 2.5%. The job to applicant ratio ticked down further to 1.18, versus 1.20 forecast (which was also the Sep outcome). The continued trend decline in the job-to-applicant ratio points to further upside in the unemployment rate, all else equal. This will be a watch point for the authorities, given on-going focus around positive real wage gains and the importance of this in sustainably reaching the 2% inflation target. It will be hoped the government's stimulus package gives the economy a boost as we progress into 2026.

- Options : Close significant option expiries for NY cut, based on DTCC data: 154.00($665m),156.50($516m). Upcoming Close Strikes : 155.00($2.25b Dec 2) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 95 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

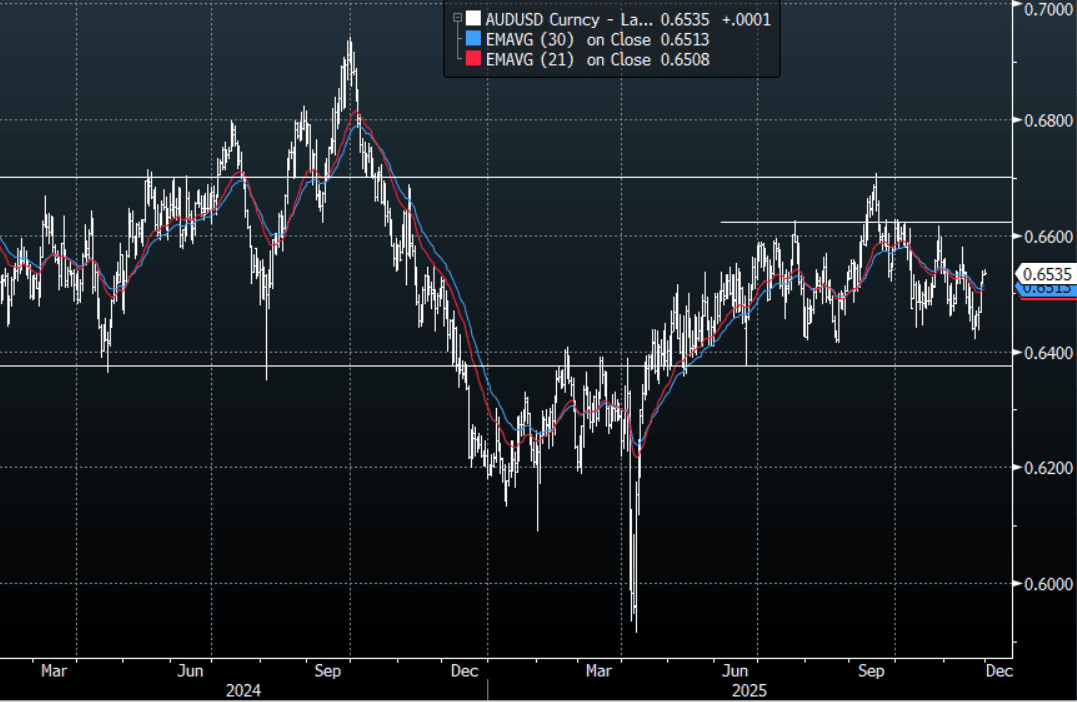

AUD/USD - Consolidates Above 0.6500, Support Likely Toward 0.6490-0.6510

The AUD/USD has had a range today of 0.6530 - 0.6541 in the Asia- Pac session, it is currently trading around 0.6535, +0.05%. The AUD/USD has had a very quiet session albeit with a slight bid undertone. The AUD is consolidating above 0.6500 and is looking to test the pivot toward 0.6550-60 within its wider 0.6350-0.6700 range. On the day, I suspect dips on the day back toward 0.6490-0.6510 continue to remain supported, a sustained break above the 0.6560 area is needed to potentially signal a move toward the top-end of its range. It could be a very quiet Friday unless we get an unforeseen catalyst.

- “Australia Oct. Private Credit Rises 0.7% M/m, Est. +0.6%. Australia's private credit rose more than economists expected in October. Estimates ranged from +0.4% to +0.7%, 13 economists.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD420m), 0.6400(AUD325m). Upcoming Close Strikes : 0.6800(AUD532m Dec 2) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

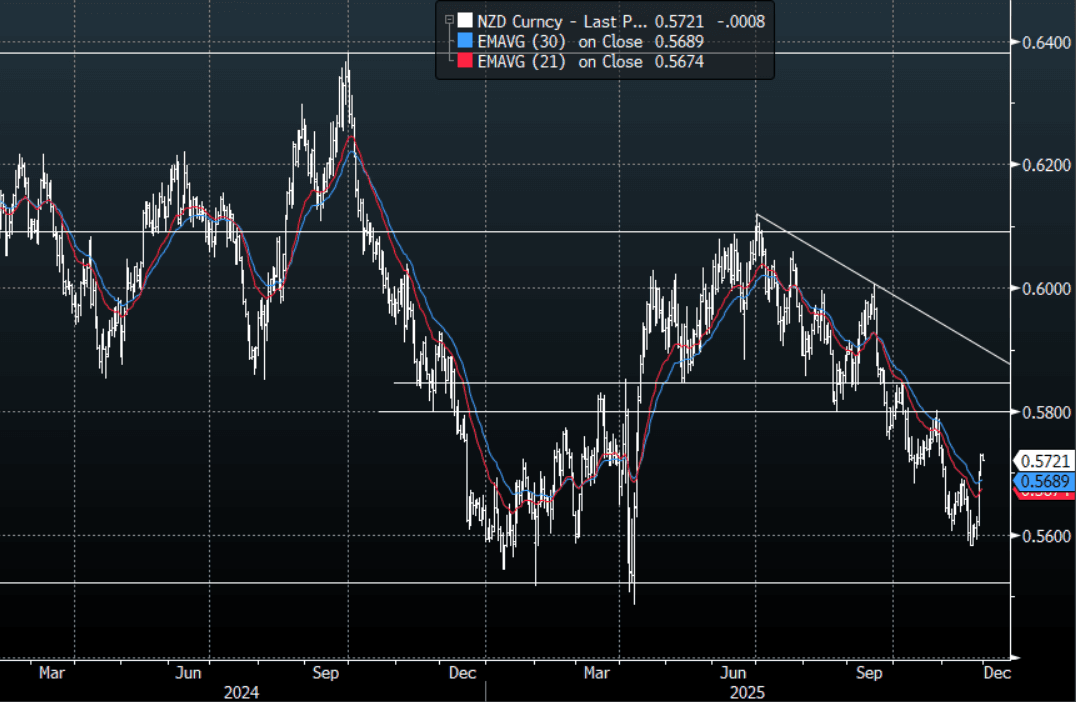

NZD/USD - Drifts Lower, Look For Support Toward 0.5680/0.5700

The NZD/USD had a range today of 0.5719 - 0.5732 in the Asia-Pac session, going into the London open trading around 0.5720, -0.15%. The NZD/USD has drifted a little lower in a very subdued session. Positioning still feels like it could be an issue in the short term. While the risk backdrop remains constructive this should provide further headwinds for the NZD shorts and I suspect we see more of the weaker hands pressured. On the day I suspect dips back toward 0.5680/0.5700 will be supported, as the market turns its focus toward 0.5760 first then the more important 0.6800-50 resistance. I suspect a quiet day all things being equal.

- MNI AU - ANZ Consumer Sentiment Bounces, Capping Off Strong NZ Data Week: The Nov ANZ consumer sentiment index bounced 6.5%m/m, to 98.4. This puts the index just short of 2025 highs, although we aren't above the 100.0 level yet. The sentiment backdrop is suggesting modestly positive growth, although it's likely we need further higher readings to point to accelerating momentum in consumption. It does cap off a solid recent run of NZ data this week, with retail sales volumes up in Q3 and yesterday's ANZ business activity/confidence readings surging to multi year highs.

- "RBNZ updates its Kiwi-GDP nowcast estimate for 3q GDP growth, showing GDP expanding 0.8% q/q. Gauge rises from 0.6% a week earlier, and is highest since began in early June" - via BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5650(NZD300m), 0.5550(NZD300m). Upcoming Close Strikes : 0.5575(NZD547m Dec 3), 0.5940(NZD427m Dec 1) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: US Rate Cut Underpins Sentiment, Mixed End to November

Expectations that the US will cut rates at the December meeting continue to underpin investor sentiment across the region in what was a mostly positive day. News out of Korea gave the KOSDAQ a boost after The Korea Economic Daily reported that the government is seeking to implement tax incentives for KOSDAQ venture funds and exempting pension funds and foreign institutional investors from taxes on stock trading. Tech stocks are still key in investors minds with many key tech names down today, yet overall for the month returns continue to be strong. Despite falls for the HSI, Alibaba's release of smart glasses powered by AI saw its stock jump in Hong Kong. The key themes for Japanese stocks on November 28, 2025, were mixed market performance, persistent inflation figures, a weakening yen, and concerns over the economic impact of rising tensions with China. Chinese stocks continue to have the persistent property market concerns over them, sparked by debt issues at developer China Vanke. Reports in local press suggest that further policy support for the property sector could be expedited given Vanke's woes. This weighed down the mainland and Hong Kong markets, despite some positive long-term economic plans announced by Beijing.

- The NIKKEI finished November with barely a whimper, down just -0.07% to 50,125; and down just -0.18% for the month. The NIKKEI remains over 4% below the October high for the year with signs that investors are rotating out of tech into broader sector allocations.

- China's major bourses were mixed today the the Hang Seng down -0.22%, whilst onshore bourses are all up. Vanke's worries weighed heavy on other property stocks in Hong Kong with China Overseas Land the biggest faller. Shenzhen is up the most with gains of +0.70% today, with Shanghai and CSI 300 up around 0.20%. For the month all major China bourses are lower with losses between 1.80-3.50% as the CSI 300 underperformed its onshore peers in November.

- The KOSPI finished November on the back foot as attention was elsewhere on taxation news. The KOSP is down -1.3% today taking it's November declines to -1.9%. The falls are on the back of over 25% gains in the last two months and likely are as much a reflection of profit taking than anything else.

- SE Asia's bourses were mixed Friday with Malaysia and Jakarta falling whilst the SE Thai delivered gains. The FTSE Malay KLCI opened quite timidly before the selloff picked up steam to be down -0.70% whilst the JCI fell -0.32%. For November the JCI was the star with gains above 5% whilst the FTSE Malay KLCI is down -0.45% and the SE THai over 4%.

- The NIFTY 50 has started Friday off slowly touching a new high of 26,234 on modest gains of 0.05%. Markets continue to wait for news of US trade deal yet are pushing ahead as economic data remains robust. For November, the NIFTY is up over 1% and over 8% for the year.

ASIA STOCKS: Taiwan Leads Inflow Rebound, Tax Headlines Weigh On Kospi Flows

As the Nov trading month comes to an end, we have seen slightly better inflow momentum for tech sensitive plays South Korea and Taiwan. The last 3 trading days for Taiwan has seen almost $1.5bn in net offshore inflows. Still, this has only curbed Nov to date outflows to just over $10.5bn. As we enter into Dec, focus will be on broader equity trends (with the US Fed outlook an important driver), along with AI/chip demand into 2026. Local bellwether TSMC continues to recover from earlier Nov lows but remains off start of the month highs.

- For South Korea, we have seen close to $600mn in net inflows in the past 3 trading days. Interestingly today though is the contrast in Kospi and Kosdaq performance. The Kospi down 1.25%, but the Kosdaq up over 3.2%. This followed earlier reports via the Korea Economic Daily: "South Korea will push for an expansion of income tax deductions for Kosdaq venture funds, which invest a significant portion of their capital in venture cos." Per the NBUY function, offshore investors have sold around -$722mn of Kospi shares today, but added $230mn to the Kosdaq. To the extent this drives Kosdaq versus Kospi outperformance we may see more outflows from the Kospi by offshore investors.

- Indian inflow momentum is back positive for the past 5 days, with chunky inflows on Wednesday. This leaves Nov to date net inflows marginally in positive territory. The Nifty has consolidated its break above 26000 in recent sessions.

- In SEA, Indonesian inflow momentum has been pared slightly into month end. However, we still sit at a reasonable +$791mn for Nov as a whole. The JCI has been an outperformer in recent months amid hopes the government's pro-growth agenda boosts equity sentiment.

- Other SEA markets have seen outflows In Nov.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 46 | -1956 | -5279 |

| Taiwan (USDmn) | 687 | -2407 | -5692 |

| India (USDmn)* | 562 | 108 | -15712 |

| Indonesia (USDmn) | -17 | 119 | -1734 |

| Thailand (USDmn) | -27 | -97 | -3366 |

| Malaysia (USDmn) | 38 | -91 | -4543 |

| Philippines (USDmn) | -17 | -75 | -660 |

| Total (USDmn) | 1272 | -4398 | -36985 |

| * Data Up To Nov 26 |

Source: Bloomberg Finance L.P./MNI

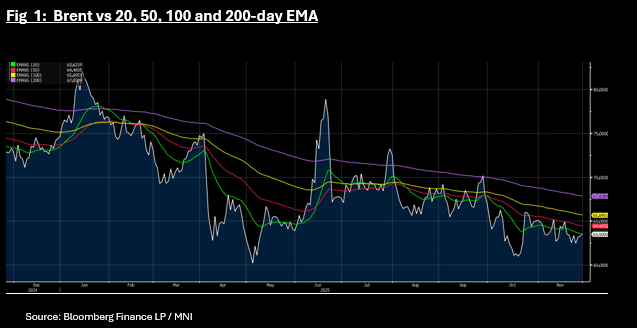

OIL: OPEC+ and Ukraine News Dominate After Poor Month for Oil

- Oil is up Friday in the Asia trading day with WTI posting gains of +0.73% to reach US$59.08. The gains sees WTI on track for a weekly gain, though November remains a very poor month with losses over -3%.

- Brent is up +0.25% Friday and near +1.5% for the week but down over 2% for the month. The move higher for Brent sees it near to the 20-day EMA of US$63.62 having traded below in the middle of the month.

- Oil prices are looking for a new catalyst and as the White House's optimism over a potential peace deal for Ukraine - and what that means for Russian supply of oil. The US Special Envoy Witkoff leads a delegation to Moscow next week with President Putin suggesting that the proposed deal still requires some amendments. Crude stocks stored at Russian oil fields rose to levels seen only twice since the country's invasion of Ukraine in early 2022, a sign that recent US sanctions are biting. More than 16 million barrels of crude was being held in storage tanks at oil fields as of Nov 20 and Nov 21, according to a person familiar with the data. (per BBG)

- OPEC+ meets over the weekend with little new news expected. Earlier this month eight of OPEC+ members agreed to a limit further new output in Q1 next year on concerns of oversupply.

- Petrobras has cut its 5-Year investment plan by 2% as oil price declines impact their forward forecasts.

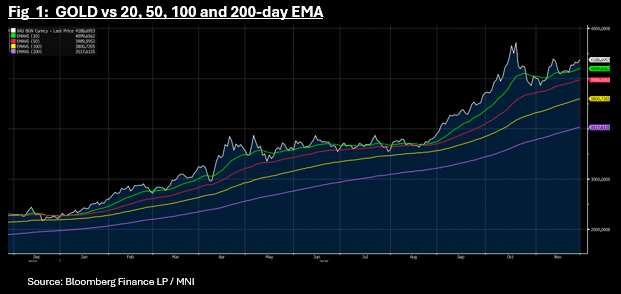

Gold Set for Another Strong Month of Gains

- Gold has has a solid start to Friday in Asia with gains of +0.73% to US$4,188.06.

- Gold in on track for another weekly gain, currently up just on 3% and over 4.6% for November and maintains its position above all major moving averages, with the 20-day EMA below at US$4,099.

- Gold's fortunes at present are strongly correlated with US rate cut hopes and with US Treasury traders off for Thanksgiving, gold had little new queues overnight.

- The India Pension Fund Regulatory and Development Authority (PFRDA) is planning to permit investment in gold and silver exchange traded funds, according to the chairman of the regulatory body (per BBG)

- Deutsche Bank raised its 2026 forecast for gold to an average of $4,450 an ounce over the year, up from $4,000 previously. Goldman Sachs last month boosted its projection for the end of next year to $4,900 an ounce from $4,300, citing ETF inflows and central-bank buying. (per BBG)

US: Trump - Will Permanently Pause Migration From 3rd World Countries

US President Trump has outlined in two Truth Social Posts that he will permanently pause all migration from all third world countries. Trump outlines the costs associated with migrant related benefits, along with other issues he states are impacted by immigration. This moves follows the recent attack on two National Guard Members in Washington. From a macro standpoint, some of the economic focus is likely to be on how this impacts/disrupts labour supply into the US economy. The full Truth Social Posts can be found at this link and here as well.

- Trump say the policy will allow the US system to recover. He states: "I will permanently pause migration from all Third World Countries to allow the U.S. system to fully recover, terminate all of the millions of Biden illegal admissions, including those signed by Sleepy Joe Biden’s Autopen, and remove anyone who is not a net asset to the United States, or is incapable of loving our Country, end all Federal benefits and subsidies to noncitizens of our Country, denaturalize migrants who undermine domestic tranquility, and deport any Foreign National who is a public charge, security risk, or non-compatible with Western Civilization."

CHINA: Data Preview: PMIs Set to Moderate, Services Still Robust

- Over the weekend and into next week, the key releases for China data will be the official PMIs on Sunday followed by the RatingDog PMIs on the 1st.

- The official PMIs give a snapshot of state owned enterprises whilst the RatingDog (formerly CAIXIN) reflects private and export oriented companies. There has been an ongoing divide between the two with the Official PMI Manufacturing in contraction since April whilst the Ratingdog Manufacturing has expanded for the last three releases.

- Expectations are for a continuance of these trend with Official PMI Manufacturing to remain modestly in contraction and the Ratingdog in line with last month at 50.5.

- Services for the Official PMIs have been anchored around 50 in recent releases and forecast to remain the same. The Ratingdog PMI Services in OCtober topped 52.6, its equal best for the year and is widely expected to moderate back towards 51.9 for November.

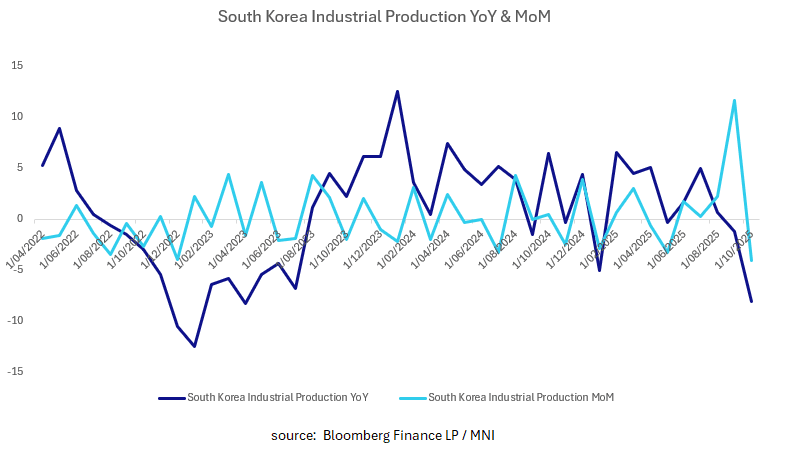

SOUTH KOREA: Industrial Production Has Biggest Decline in 2-Years

- Industrial production slumped in South Korea in October with the YoY decline the largest since early 2023.

- The MoM figure declined -4%; its biggest decline in 5-Years.

- Industrial production ramped up the month prior ahead of the Trump Xi meeting and the finalization of the Korea US trade agreement. The expansion in September was the largest in more than a year and suggests that the October result is as much a reaction to the ramping up of output.

- It was was widely expected that I/P would contract, though the size of the contraction was larger than forecast and we would look to next month's release for a clearer indication as to the full impact on production.

ASIA FX: CNH Up 0.50% For Week, USD/KRW Supported On Dips

In North East Asia FX, all currencies are tracking higher against the USD over the past week (although KRW and TWD have lost a little ground so far today). CNH is an outperformer (up 0.50%) after USD/CNH broke to fresh YTD lows under 7.0700 (7.0653). We have seen the USD/CNY fixing bias turn positive, i.e. no longer supporting yuan appreciation. This may slow yuan gains, although moves in USD/CNH above 7.0800 have drawn selling interest so far. Lower US-CH yield differentials, along with potential for fresh conversion of foreign currency into CNY as we approach year end and into early 2026, is aiding yuan sentiment. Downside focus in USD/CNH will be around the 7.0500 region.

- Spot USD/KRW is also down this week, but has remained volatile. We were last near 1465/66, still within striking distance of recent highs near 1480. The BoK left rates on hold as expected, but the hawkish (explicit removal of easing bias), drove SK rates higher, although benefit to KRW was only fleeting. The FinMin also disappointed with no fresh measures to improve FX supply/demand imbalances. BOK Governor Rhee stated NPS hedging flows are too predictable and lack macro impact. Uncertainty around how the authorities will improve these imbalances is keep USD/KRW dips under 1460 supported for now.

- Spot USD/TWD sits off its recent highs, last near 31.35. Recent highs in the pair were around 31.49. The better equity tone (with nearly $1.5bn in offshore inflows) has helped sentiment. Note the 20-day EMA is around 31.17, as a potential downside support point. BBG notes: "At end of October, Taiwan life insurers’ hedging ratio dropped to 58.55%, an FSC official says at briefing" (which is the lowest since 202 per BBG).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/11/2025 | 0700/0800 | *** | GDP | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0700/0800 | ** | Import/Export Prices | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0745/0845 | *** | HICP (p) | |

| 28/11/2025 | 0745/0845 | ** | PPI | |

| 28/11/2025 | 0745/0845 | *** | GDP (f) | |

| 28/11/2025 | 0745/0845 | ** | Consumer Spending | |

| 28/11/2025 | 0745/0845 | Payrolls | ||

| 28/11/2025 | 0800/0900 | *** | HICP (p) | |

| 28/11/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 28/11/2025 | 0800/0900 | *** | GDP | |

| 28/11/2025 | 0855/0955 | ** | Unemployment | |

| 28/11/2025 | 0900/1000 | *** | GDP (f) | |

| 28/11/2025 | 0900/1000 | *** | Bavaria CPI | |

| 28/11/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 28/11/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 28/11/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/11/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1330/0830 | *** | GDP - Canadian Economic Accounts | |

| 28/11/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 28/11/2025 | 1330/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 28/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 28/11/2025 | 1600/1100 | Finance Dept monthly Fiscal Monitor (expected) |