ASIA STOCKS: US Rate Cut Underpins Sentiment, Mixed End to November

Expectations that the US will cut rates at the December meeting continue to underpin investor sentiment across the region in what was a mostly positive day. News out of Korea gave the KOSDAQ a boost after The Korea Economic Daily reported that the government is seeking to implement tax incentives for KOSDAQ venture funds and exempting pension funds and foreign institutional investors from taxes on stock trading. Tech stocks are still key in investors minds with many key tech names down today, yet overall for the month returns continue to be strong. Despite falls for the HSI, Alibaba's release of smart glasses powered by AI saw its stock jump in Hong Kong. The key themes for Japanese stocks on November 28, 2025, were mixed market performance, persistent inflation figures, a weakening yen, and concerns over the economic impact of rising tensions with China. Chinese stocks continue to have the persistent property market concerns over them, sparked by debt issues at developer China Vanke. Reports in local press suggest that further policy support for the property sector could be expedited given Vanke's woes. This weighed down the mainland and Hong Kong markets, despite some positive long-term economic plans announced by Beijing.

- The NIKKEI finished November with barely a whimper, down just -0.07% to 50,125; and down just -0.18% for the month. The NIKKEI remains over 4% below the October high for the year with signs that investors are rotating out of tech into broader sector allocations.

- China's major bourses were mixed today the the Hang Seng down -0.22%, whilst onshore bourses are all up. Vanke's worries weighed heavy on other property stocks in Hong Kong with China Overseas Land the biggest faller. Shenzhen is up the most with gains of +0.70% today, with Shanghai and CSI 300 up around 0.20%. For the month all major China bourses are lower with losses between 1.80-3.50% as the CSI 300 underperformed its onshore peers in November.

- The KOSPI finished November on the back foot as attention was elsewhere on taxation news. The KOSP is down -1.3% today taking it's November declines to -1.9%. The falls are on the back of over 25% gains in the last two months and likely are as much a reflection of profit taking than anything else.

- SE Asia's bourses were mixed Friday with Malaysia and Jakarta falling whilst the SE Thai delivered gains. The FTSE Malay KLCI opened quite timidly before the selloff picked up steam to be down -0.70% whilst the JCI fell -0.32%. For November the JCI was the star with gains above 5% whilst the FTSE Malay KLCI is down -0.45% and the SE THai over 4%.

- The NIFTY 50 has started Friday off slowly touching a new high of 26,234 on modest gains of 0.05%. Markets continue to wait for news of US trade deal yet are pushing ahead as economic data remains robust. For November, the NIFTY is up over 1% and over 8% for the year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Market pricing is close to flat for the meeting outcome. A full 25bps hike is not priced by the market until around the March 2026 meeting.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

RBA: “Material” CPI Miss & Consumer Recovery Drive Westpac To Exclude 2025 Cuts

The AUD OIS market has almost no chance of a cut priced in for the 4 November RBA decision with only around 25% of 25bp for the 9 December decision following the broadly higher-than-expected Q3 CPI data. The October Bloomberg survey showed that economists were not unanimous as to when they expected the next cut. Of the big four local banks, only Westpac forecasted a November easing but that has now changed.

- Given that inflation is higher than the RBA expected and the “emerging consumer recovery”, Westpac now expects rates to be unchanged over the rest of 2025. It is re-evaluating the 2026 outlook but sees the February meeting also in doubt given how much higher inflation is.

- It points out though that the labour market may surprise to the downside next year. The Q3 unemployment rate was higher than the RBA expected and employment growth slower.

- Westpac consumption data are suggesting “solid gains in Q3 and into Q4” and so it now expects the RBA to revise up its consumption profile.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum. However, it uses market rates in its model and they are higher which may allow inflation further out to return to the 2.5% band mid-point.

- RBA Governor Bullock said this week the Board remains cautious and more information is needed on inflation and the labour market given the volatility of the monthly numbers. She also described a 0.9% q/q Q3 CPI rise as a “material miss”.

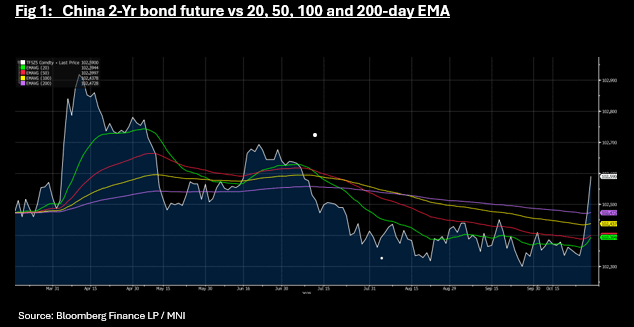

CHINA: Bond Futures Rally on Large Liquidity Injection

- The largest liquidity injection in recent weeks this morning has given bonds a boost, with bond futures up in morning trade.

- The 10-YR is up +0.19 to 108.61 trending back above all major moving averages.

- The 2-Yr bond future is up +0.11 to 102.58 for its largest one day jump since April. The move takes the 2-Yr above all major moving averages also.

- The CGB market hasn't reacted as strongly with the 10-Yr down -1bp to 1.80%.

- The PBOC governor indicated that the PBOC would re-enter the bond market and purchase CGB's according to Xinhua, without specify timing or amounts but with local commentators suggesting at present, amounts may not be significant. The 10-Yr CGB traded in a 1.60 -1.70% range from March through to July before breaking higher to 1.88% in late September. The PBOC has halted its bond buying this year, citing calm, stable markets and investors able to absorb issuance though with the move to equities from investors growing in strength, it seems likely that the PBOC may look to return the 10-Yr range back towards 1.60 -1.70%