FOREX: USD - BBDXY Move Lower Stalls Toward 1218

The BBDXY has had a range today of 1218.76 - 1220.19 in the Asia-Pac session; it is currently trading around 1219, +0.05%. A very subdued Friday Asian session for currencies to end the week. This week the standout has been the huge bounce in global risk together with a repricing of more potential US rate cuts. The USD has played catch up to this but has found some bids initially around the 1218 area overnight stalling the move in a quiet overnight session thanks to the US being off. On the day I suspect a range of 1218-1224 should cover a subdued end of the week as we move back toward the middle or lower end of the 1210-1230 range, first support seen toward 1218 and then the 1208-1214 area.

- EUR/USD - Asian range 1.1582 - 1.1602, Asia is currently trading 1.1590. The pair is consolidating just below 1.1600. On the day I suspect dips could now be supported first up as the market tries to work through the resistance around 1.1600-25, above here and the focus could turn back toward the 1.1700 area.

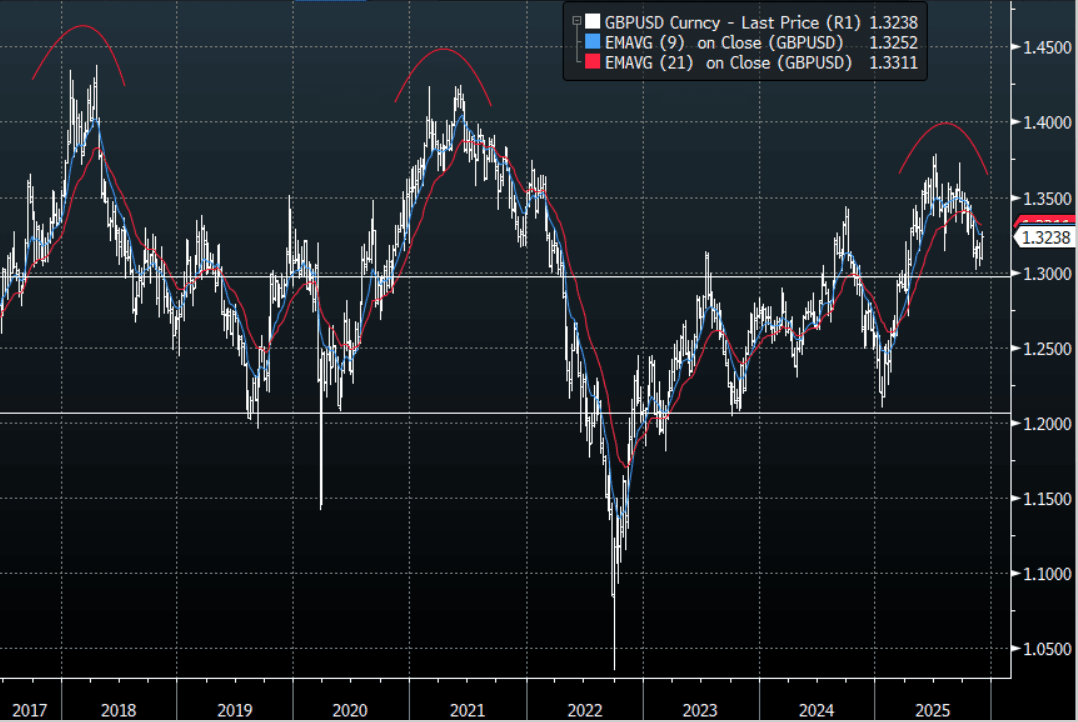

- GBP/USD - Asian range 1.3229 - 1.3245, Asia is currently dealing around 1.3240. The pair is consolidating its recent gains around 1.3250. I remain skewed toward shorts but I feel this move does signal the need to be patient as it could first move a little higher. I will be watching the price action back toward 1.3300-1.3400 for signs of a top should we get back up there.

- Cross asset : SPX +0.40%, Gold $4185, US 10-Year 4.006%, BBDXY 1219, Crude Oil $59.10

- Data/Events : Germany Retail Sales/Unemployment Change/CPI, France CPI/PPI/GDP, Spain CPI/Retail Sales/Current Account Balance, EZ ECB 1&3 Yr CPI Expectations, Italy GDP/CPI

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: 2yr Swap Above 20-day EMA Post Aust CPI Spillover

NZGB yields are higher across the benchmarks, led by the back end, positive spill over has been evident from the ACGB yield surge post the higher than forecast Q3 CPI print (ACGB yields are 4-11.5bps firmer led by the front end). NZGB 2yr is back to close to 2.57%, while the 10yr is near 4.04%, both benchmarks tracking towards 20-day EMA resistance tests (2.61% for the 2yr, around 4.07% for the 10yr).

- The 2yr swap rate is already testing through the 20-day EMA resistance point, last near 2.41%, up 5bps for the session. The 50-day is at 2.53%. The AU-NZ 2yr swap rate differential continues to climb, up to 106bps.

- There hasn't been much of a shift in RBNZ pricing expectations. We are still close to 100% priced for a Nov 25bps cut.

- Earlier, RBNZ Director of Financial Markets Richardson spoke on the transmission of the 300bp of easing since August 2024. The MPC discussed this at the October meeting, implying they are concerned that the pass through of rate cuts to the economy has not been as efficient as expected. Richardson said today that global factors have increased NZ long-end yields, which have put upward pressure on domestic rates and thus financial conditions, the RBNZ could "adapt" policy to ease them again in order to achieve its 2%-mid-point inflation target.

- The NZGB 2/10s curve is holding elevated, last +147bps. In recent years we have struggled to maintain +150bps steepness. This may become more of a policy focus point if the NZ economy struggles for further positive traction in 2026.

- Note tomorrow we get the Oct ANZ activity outlook and business confidence prints.

GOLD: Gold & Silver Higher Ahead Of Expected Fed Rate Cut

Gold has rallied during today’s APAC session ahead of the Fed decision later. While a 25bp rate cut is widely expected, monetary easing is positive for non-interest bearing bullion. It will be watching the tone of Chair Powell’s comments and is likely to strengthen if they come across as dovish but he’s unlikely to give much away. The market has almost another 25bp priced in for the December decision.

- Gold is up 0.3% to $3964.5/oz today following a high of $3982.33, remaining below $4000, despite a 0.1% rise in the USD BBDXY and stable US yields. Initial resistance is at $4161.4, 22 October high. With the metal remaining in overbought territory, it could correct further.

- Silver is also higher up 0.8% to $47.45 after reaching $47.610, but still below initial resistance at $49.456, 23 October high.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- Equities are mixed with the S&P e-mini up 0.2%, CSI 300 +0.5% but the Straits Times down 0.3%. Oil prices are slightly lower with WTI -0.1% to $60.10/bbl. Copper is down 0.1%.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Market pricing is close to flat for the meeting outcome. A full 25bps hike is not priced by the market until around the March 2026 meeting.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK