JGBS: Cheaper With 10Y Leading, 10YY Back At Cycle Highs

JGB futures are weaker, -17 compared to settlement levels.

- The 2-year bond auction delivered weak results today. The low price cleared below the Bloomberg-surveyed forecast of 100.05, while the cover ratio dropped to 3.5310x from 4.4665x. The tail also lengthened to 0.012 from 0.002 last month.

- Reuters reported yesterday that the Japanese government will increase issuance of 2-year and 5-year JGBs from January, with around ¥100bn of additional supply in each tenor. There are no changes expected for 10–40-year issuance.

- Japan's Nov Tokyo CPI print was fairly close to market expectations.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session, but volumes have been light given Thursday's Thanksgiving Day Holiday.

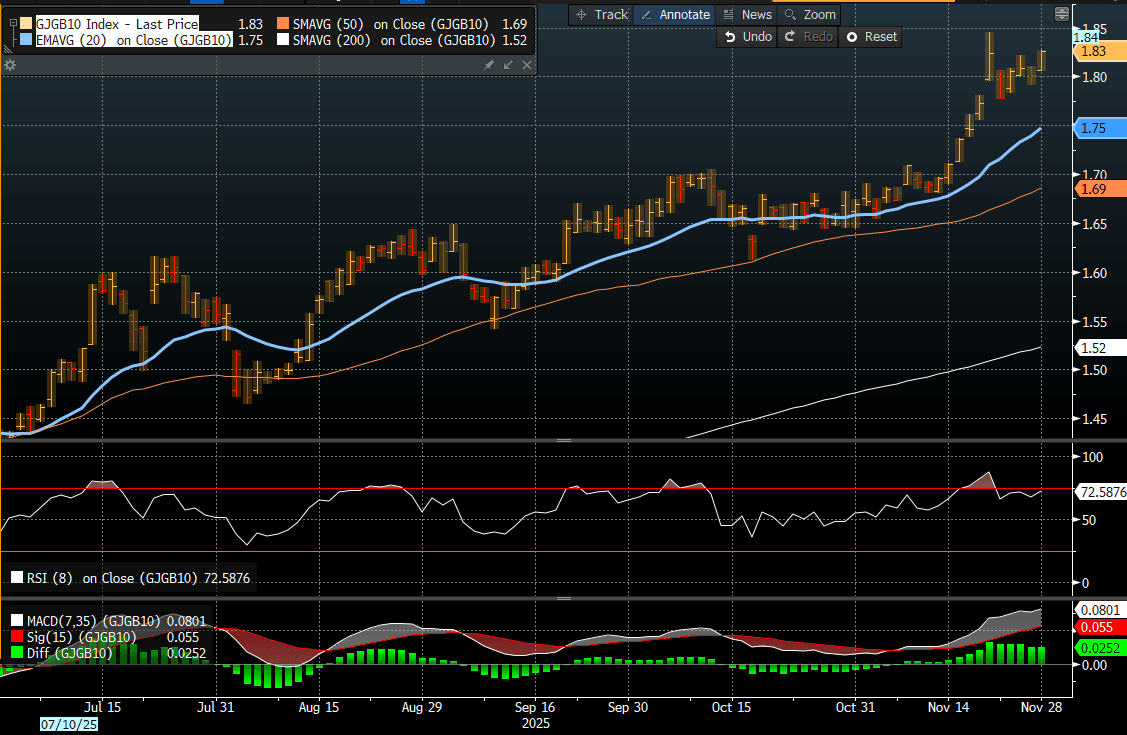

- Cash JGBs are flat to 2.5bps across benchmarks, with the 10-year underperforming. The benchmark 10-year yield is 2.5bps higher at 1.826% versus the cycle high of 1.84%. (see chart)

- Swap rates are 1-2bps higher.

- Tomorrow, the local calendar will see Q3 Capital Spending, Q3 Company Sales and S&P Global PMI Mfg alongside a BOJ Governor Ueda Speech in Nagoya.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: 2yr Swap Above 20-day EMA Post Aust CPI Spillover

NZGB yields are higher across the benchmarks, led by the back end, positive spill over has been evident from the ACGB yield surge post the higher than forecast Q3 CPI print (ACGB yields are 4-11.5bps firmer led by the front end). NZGB 2yr is back to close to 2.57%, while the 10yr is near 4.04%, both benchmarks tracking towards 20-day EMA resistance tests (2.61% for the 2yr, around 4.07% for the 10yr).

- The 2yr swap rate is already testing through the 20-day EMA resistance point, last near 2.41%, up 5bps for the session. The 50-day is at 2.53%. The AU-NZ 2yr swap rate differential continues to climb, up to 106bps.

- There hasn't been much of a shift in RBNZ pricing expectations. We are still close to 100% priced for a Nov 25bps cut.

- Earlier, RBNZ Director of Financial Markets Richardson spoke on the transmission of the 300bp of easing since August 2024. The MPC discussed this at the October meeting, implying they are concerned that the pass through of rate cuts to the economy has not been as efficient as expected. Richardson said today that global factors have increased NZ long-end yields, which have put upward pressure on domestic rates and thus financial conditions, the RBNZ could "adapt" policy to ease them again in order to achieve its 2%-mid-point inflation target.

- The NZGB 2/10s curve is holding elevated, last +147bps. In recent years we have struggled to maintain +150bps steepness. This may become more of a policy focus point if the NZ economy struggles for further positive traction in 2026.

- Note tomorrow we get the Oct ANZ activity outlook and business confidence prints.

GOLD: Gold & Silver Higher Ahead Of Expected Fed Rate Cut

Gold has rallied during today’s APAC session ahead of the Fed decision later. While a 25bp rate cut is widely expected, monetary easing is positive for non-interest bearing bullion. It will be watching the tone of Chair Powell’s comments and is likely to strengthen if they come across as dovish but he’s unlikely to give much away. The market has almost another 25bp priced in for the December decision.

- Gold is up 0.3% to $3964.5/oz today following a high of $3982.33, remaining below $4000, despite a 0.1% rise in the USD BBDXY and stable US yields. Initial resistance is at $4161.4, 22 October high. With the metal remaining in overbought territory, it could correct further.

- Silver is also higher up 0.8% to $47.45 after reaching $47.610, but still below initial resistance at $49.456, 23 October high.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- Equities are mixed with the S&P e-mini up 0.2%, CSI 300 +0.5% but the Straits Times down 0.3%. Oil prices are slightly lower with WTI -0.1% to $60.10/bbl. Copper is down 0.1%.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Market pricing is close to flat for the meeting outcome. A full 25bps hike is not priced by the market until around the March 2026 meeting.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK