AUSSIE BONDS: Cheaper, AU-US 10Y Diff Keeps Pushing Wider

ACGBs (YM -4.5 & XM -3.0) are cheaper and hovering near session lows.

- Private credit rose 0.7% m/m (estimate +0.6%) in October versus +0.6% in September. Private credit rose 7.3% y/y versus a revised +7.2% in September.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session, but volumes have been light given Thursday's Thanksgiving Day Holiday.

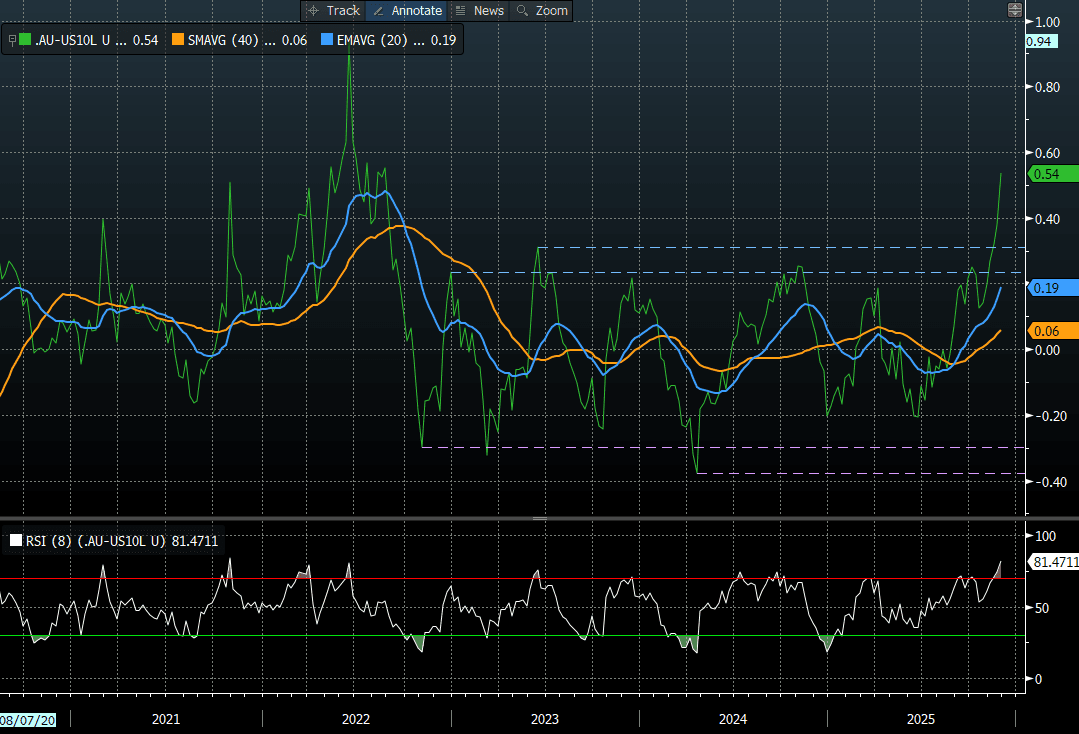

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +52bps. Today’s move has extended the differential’s push above the ±30bps range that had persisted since November 2022 (see chart).

- The bills strip is -2 to -6 across contracts, with a steepening bias.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 0% probability. Notably, the market has shifted to giving a 44% probability to 25bp easing by December 2026.

- On Monday, the local calendar will see Cotality Home Values, S&P Global PMI Mfg, Melbourne Institute Inflation, and ANZ-Indeed Job Advertisements monthly data, and Q3 Company Operating Profit and Inventories.

- Next week, the AOFM plans to sell A$1000mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold & Silver Higher Ahead Of Expected Fed Rate Cut

Gold has rallied during today’s APAC session ahead of the Fed decision later. While a 25bp rate cut is widely expected, monetary easing is positive for non-interest bearing bullion. It will be watching the tone of Chair Powell’s comments and is likely to strengthen if they come across as dovish but he’s unlikely to give much away. The market has almost another 25bp priced in for the December decision.

- Gold is up 0.3% to $3964.5/oz today following a high of $3982.33, remaining below $4000, despite a 0.1% rise in the USD BBDXY and stable US yields. Initial resistance is at $4161.4, 22 October high. With the metal remaining in overbought territory, it could correct further.

- Silver is also higher up 0.8% to $47.45 after reaching $47.610, but still below initial resistance at $49.456, 23 October high.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- Equities are mixed with the S&P e-mini up 0.2%, CSI 300 +0.5% but the Straits Times down 0.3%. Oil prices are slightly lower with WTI -0.1% to $60.10/bbl. Copper is down 0.1%.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Market pricing is close to flat for the meeting outcome. A full 25bps hike is not priced by the market until around the March 2026 meeting.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

RBA: “Material” CPI Miss & Consumer Recovery Drive Westpac To Exclude 2025 Cuts

The AUD OIS market has almost no chance of a cut priced in for the 4 November RBA decision with only around 25% of 25bp for the 9 December decision following the broadly higher-than-expected Q3 CPI data. The October Bloomberg survey showed that economists were not unanimous as to when they expected the next cut. Of the big four local banks, only Westpac forecasted a November easing but that has now changed.

- Given that inflation is higher than the RBA expected and the “emerging consumer recovery”, Westpac now expects rates to be unchanged over the rest of 2025. It is re-evaluating the 2026 outlook but sees the February meeting also in doubt given how much higher inflation is.

- It points out though that the labour market may surprise to the downside next year. The Q3 unemployment rate was higher than the RBA expected and employment growth slower.

- Westpac consumption data are suggesting “solid gains in Q3 and into Q4” and so it now expects the RBA to revise up its consumption profile.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum. However, it uses market rates in its model and they are higher which may allow inflation further out to return to the 2.5% band mid-point.

- RBA Governor Bullock said this week the Board remains cautious and more information is needed on inflation and the labour market given the volatility of the monthly numbers. She also described a 0.9% q/q Q3 CPI rise as a “material miss”.