AUDNZD: Softer NZ Data Sees Break Above 1.1100, 2yr AU-NZ Swap Spreads Trending Towards Flat

AUD/NZD has started risen to fresh highs in early Friday dealings. The pair getting to 1.1115, we now sit just off these highs.

- The cross has had support from earlier weaker NZ Data releases. Notably the NZ PMI fell to 41.1 in June. This is the weakest level since Q3 2021 and continues the run of soft data outcomes, particularly on the survey side.

- BNZ noted: "While the weakness in these series have not been as deep as during the GFC the length of it has been longer, and it is not over yet'': BNZ

- ``Manufacturing activity is highly leveraged to domestic demand, particularly residential construction and household spending. Both of these are faltering” (per BBG)

- We also had card spending figures print lower in June, down 0.5%m/m for total spending and -0.6% for retail. May falls were also revised slightly weaker.

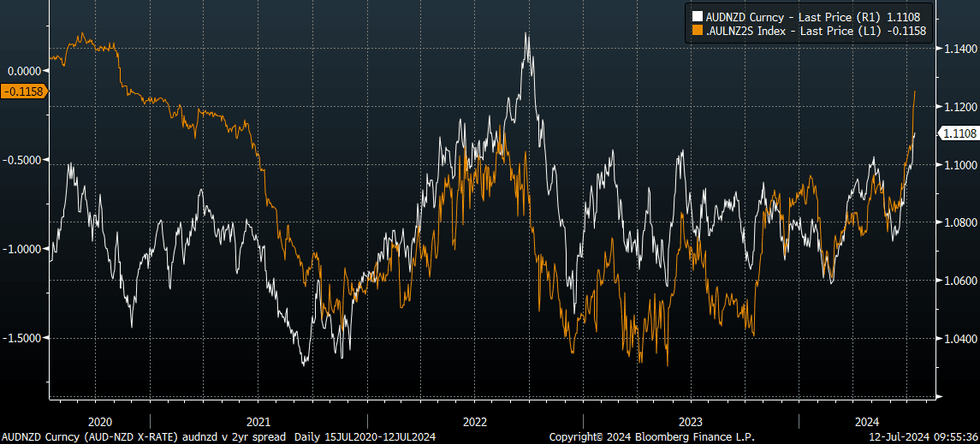

- The AU-NZ 2yr swap spread is trending towards flat, last -12bps, see the chart below.

- Levels wise for AUD/NZD, a sustained 1.1100 break would open up 1.1174 (July 2022 highs).

- Next week we have the all important NZ Q2 CPI release on Wednesday, then AU employment on Thursday.

Fig 1: AUD/NZD Looks To Maintain 1.1100 Break, AU-NZ 2yr Swap Spread Getting Close To Flat

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: JAPAN MAY CORP GOODS PRICE INDEX +2.4% Y/Y; APR REV +1.1%

- MNI: JAPAN MAY CORP GOODS PRICE INDEX +2.4% Y/Y; APR REV +1.1%

- JAPAN MAY CORP GOODS PRICE INDEX +0.7% M/M; APR REV +0.5%

JGBS: Futures Sharply Higher, US Tsys Buoyed By Haven Demand & Strong 10Y Auction

In post-Tokyo trade, JGB futures are sharply higher, closing +27 compared to settlement levels, after US tsys richened amid haven demand associated with European Parliament elections and the surprise snap election called in France.

- US tsys climbed further after a solid $39 billion tsy sale reflected speculation that today's inflation reading will help make the case for the Federal Reserve to cut rates this year. Demand at the 10-year auction was strong, with the bid-to-cover ratio of 2.67 being the highest since February 2022 — the month before the start of the tightening cycle.

- The 10-year yield finished 7bps lower at 4.40%, with 2-year was down 5bps to 4.83%. The curve ended at -44 bps from -42 bps.

- Looking ahead, US CPI is at 0830ET today, with the FOMC policy announcement at 1400ET and Fed Chairman Powell’s presser at 1430ET.

- The market ascribes no chance for a rate cut at this meeting but will be seeking guidance on the timing of the first rate cut. The dot plot projections are likely to show the median FOMC member expecting just one or two rate cuts this year (down from three previously projected).

- Today, the local calendar will see PPI data alongside BoJ Rinban Operations covering 1-10-year and 25-year+ JGBs.

OIL: OPEC Still Expects Robust H2 Demand But US Supply Rising

Oil prices not only kept its significant gains from Monday but rose a further 0.6% driven by OPEC’s unchanged expectations of a 2.3mbd increase in demand in H2. It also expects supply to be 2.7mbd below current production consistent with its plan to reduce output cuts. The market will now wait for today’s Fed decision, US CPI and the IEA’s monthly report. The USD index is up 0.2%.

- WTI rose 0.6% to $78.18 to be up 1.6% this month. It fell to a low of $77.22 before rallying to a high of $78.36. It has started today’s trading around $78.18. Initial resistance is at $78.38, 50-day EMA, and support at $72.48, June 4 low.

- Brent was also 0.6% higher at $82.12 to be +1.3% in June. It reached a high of $82.36 following a low of $81.19. Despite recovering from recent lows, the trend condition remains bearish and gains are seen as corrective. Initial resistance is at $85.52, 50-day EMA, while support is at $76.76, June 4 low.

- The EIA released its short-term energy outlook and revised up US crude output expectations by 40kbd from May to a 2024 annual increase of 310kbd to over 13.2mbd, a new record. Rising US production may derail OPEC’s plans to reduce its output cuts.

- Bloomberg reported a US crude stock drawdown of 2.4mn barrels last week, according to people familiar with the API data. Gasoline fell 2.5mn but distillate rose 1mn. The official EIA data is out later today.