AUDNZD: Relative Data Outcomes Driving Spot Towards 1.1000 Test

The AUD/NZD cross remains on the front foot supported by recent data outcomes skewed in the AUD's favor. Resistance is at 1.0989 (July 2 high), a break here would open a move to 1.100 (May 13 high), beyond that lies May 7 highs of 1.1031.

- This morning's firmer retail sales data, coupled with stronger building approvals data, has supported AU yield momentum. Risks of an August hike have risen, although we remain sub last week's highs.

- We have the RBNZ meeting next week, where no changes are expected. Still, survey data has pointed towards NZ being on a more favorable path to achieve its inflation target than Australia.

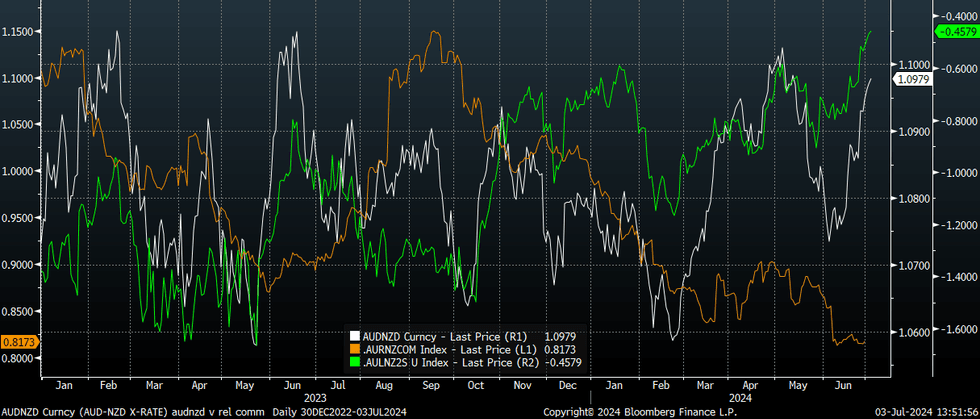

- The chart below plots AUD/NZD versus both the 2yr AU-NZ swap spread and relative commodity prices. The 2yr spread is still negative but has clearly trended in AUD's favor and remains the strongest correlator with AUD/NZD moves. (63% in levels terms for 2024 to date)

- Relative commodity prices may also swing more in AUD's favor. Iron ore prices are up from recent lows, while dairy prices faltered during the overnight auction. Still the correlation between relative commodity prices (proxied by Duetsche Bank (for AU) and CBA (for NZ) series) have a negative correlation with AUD/NZD movements so far this year.

- Milk powder prices fell to $3,218 from $3,394, while the weighted average price for all milk products was $3,782 per ton, with the GDT price index dropping 6.9%. This was the second largest drop on record, although it should be noted we are still 11.2% higher than the lows made around this time last year.

Fig 1: AUD/NZD Versus Au-NZ 2yr Swap Spreads & Relative Commodity Prices

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

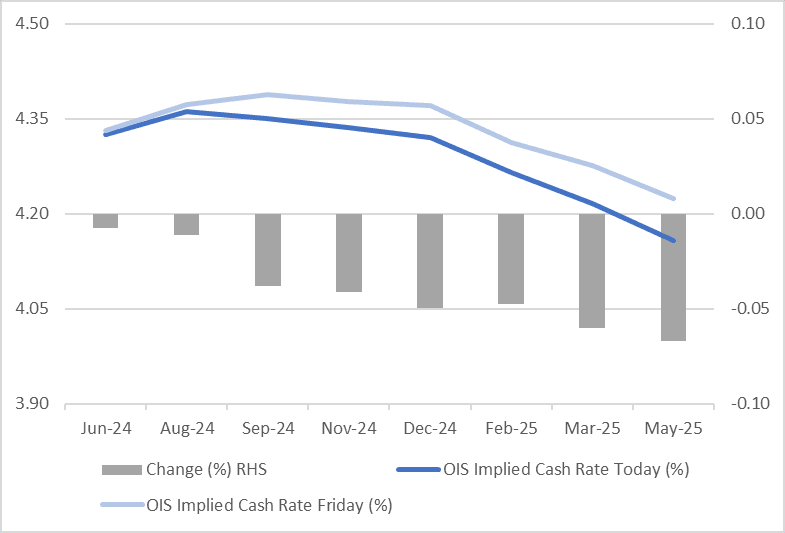

STIR: RBA Dated OIS Softer After Friday's US PCE Deflator Data Prints In-Line

RBA-dated OIS pricing is 1-6bps softer across meetings.

- This comes after no upside surprise in the much-awaited US PCE deflator data on Friday prevented further erosion in the Fed outlook. The market is still priced for at least one rate cut this year, though it is not fully priced until December.

- In Australia, 4bps of easing is priced by year-end from an expected terminal rate of 4.36%.

Figure 1: RBA-Dated OIS – Today Vs. Friday

Source: Bloomberg / MNI - Market News

GOLD: Lower Despite Friday’s Benign US PCE Deflator

Gold is 0.2% lower in the Asia-Pac session, after closing 0.7% lower at $2327.33 on Friday. The yellow metal was marginally lower on the week.

- In terms of fundamental drivers, the market has embraced the idea that the Federal Reserve will stick to recent signalling that it needs more evidence that inflation is cooling before it can pivot to rate cuts.

- On Friday, no upside surprise in the much-awaited PCE price data prevented further erosion in the Fed outlook. The market is still priced for at least one rate cut this year, though it is not fully priced until December.

- According to MNI’s technicals team, a short-term bear cycle in gold remains in play, for now, although the recent move down appears to be a correction that is allowing an overbought condition to unwind.

- A resumption of gains would open $2452.5 next, a Fibonacci projection. The 50-day EMA, at $2307.8, represents a key support.

MNI EXCLUSIVE: How The RBA Is Responding To Recent Data

MNI looks at how the RBA is responding to recent data --On MNI Policy MainWire now, for more details please contact sales@marketnews.com.