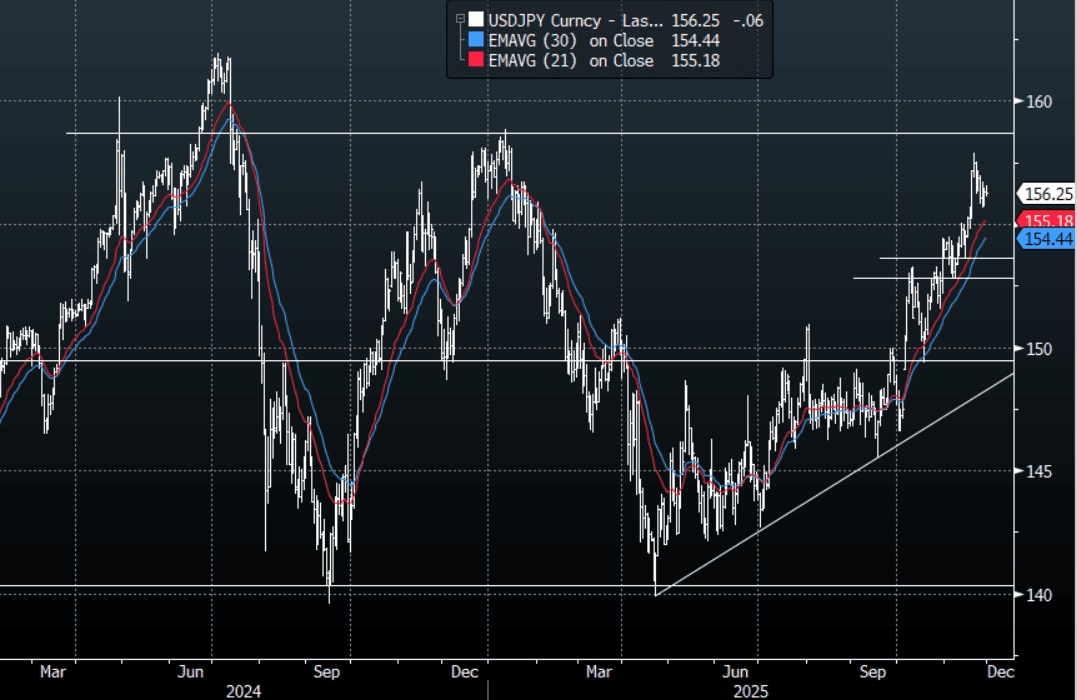

JPY: USD/JPY - Holding Above 156.00, Support Back Towards 154-155

The USD/JPY range today has been 156.10 - 156.58 in the Asia-Pac session, it is currently trading around 156.20, -0.05%. The pair has traded sideways in a very subdued session. The move in the Yen looks like it might force the BOJ into action in December and we now have the market pricing in imminent cuts in the US. This could have an impact or at least slow what looked like a situation that was about to get out hand. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 154-155 area which I suspect would be bought at first. Look for the consolidation to continue as the market contemplates if these moves by central banks are going to be enough to challenge the weakening Yen trajectory.

- MNI AU - Nov Tokyo CPI Close To Forecast, Services Y/Y Steady At 1.56% y/y: Japan's Nov Tokyo CPI print was fairly close to market expectations. Headline rose 2.7%y/y, in line with the consensus (while the Oct outcome was also revised down to this level, from 2.8%). Ex fresh food and energy printed 2.8%y/y (a touch above the 2.7% forecast), while the ex fresh food, energy measure was 2.8%y/y, in line with the prior and consensus forecast for today. We are off earlier 2025 highs, but remain close to 3%.

- MNI AU - Job-To-Applicant Ratio Downtrend Continues, Risking Higher U/E Rates: Japan Oct jobless rate and job to applicant ratio figures were weaker than expected. The unemployment rate held steady at 2.6%, against a market forecast of 2.5%. The job to applicant ratio ticked down further to 1.18, versus 1.20 forecast (which was also the Sep outcome). The continued trend decline in the job-to-applicant ratio points to further upside in the unemployment rate, all else equal. This will be a watch point for the authorities, given on-going focus around positive real wage gains and the importance of this in sustainably reaching the 2% inflation target. It will be hoped the government's stimulus package gives the economy a boost as we progress into 2026.

- Options : Close significant option expiries for NY cut, based on DTCC data: 154.00($665m),156.50($516m). Upcoming Close Strikes : 155.00($2.25b Dec 2) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 95 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold & Silver Higher Ahead Of Expected Fed Rate Cut

Gold has rallied during today’s APAC session ahead of the Fed decision later. While a 25bp rate cut is widely expected, monetary easing is positive for non-interest bearing bullion. It will be watching the tone of Chair Powell’s comments and is likely to strengthen if they come across as dovish but he’s unlikely to give much away. The market has almost another 25bp priced in for the December decision.

- Gold is up 0.3% to $3964.5/oz today following a high of $3982.33, remaining below $4000, despite a 0.1% rise in the USD BBDXY and stable US yields. Initial resistance is at $4161.4, 22 October high. With the metal remaining in overbought territory, it could correct further.

- Silver is also higher up 0.8% to $47.45 after reaching $47.610, but still below initial resistance at $49.456, 23 October high.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- Equities are mixed with the S&P e-mini up 0.2%, CSI 300 +0.5% but the Straits Times down 0.3%. Oil prices are slightly lower with WTI -0.1% to $60.10/bbl. Copper is down 0.1%.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Market pricing is close to flat for the meeting outcome. A full 25bps hike is not priced by the market until around the March 2026 meeting.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

RBA: “Material” CPI Miss & Consumer Recovery Drive Westpac To Exclude 2025 Cuts

The AUD OIS market has almost no chance of a cut priced in for the 4 November RBA decision with only around 25% of 25bp for the 9 December decision following the broadly higher-than-expected Q3 CPI data. The October Bloomberg survey showed that economists were not unanimous as to when they expected the next cut. Of the big four local banks, only Westpac forecasted a November easing but that has now changed.

- Given that inflation is higher than the RBA expected and the “emerging consumer recovery”, Westpac now expects rates to be unchanged over the rest of 2025. It is re-evaluating the 2026 outlook but sees the February meeting also in doubt given how much higher inflation is.

- It points out though that the labour market may surprise to the downside next year. The Q3 unemployment rate was higher than the RBA expected and employment growth slower.

- Westpac consumption data are suggesting “solid gains in Q3 and into Q4” and so it now expects the RBA to revise up its consumption profile.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum. However, it uses market rates in its model and they are higher which may allow inflation further out to return to the 2.5% band mid-point.

- RBA Governor Bullock said this week the Board remains cautious and more information is needed on inflation and the labour market given the volatility of the monthly numbers. She also described a 0.9% q/q Q3 CPI rise as a “material miss”.