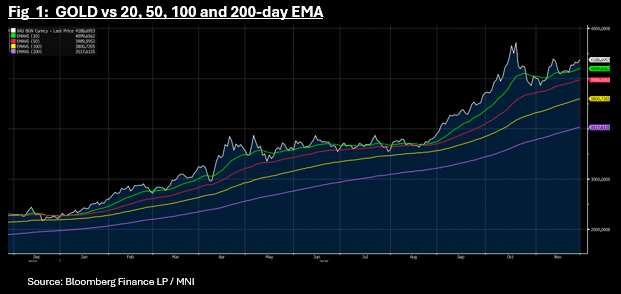

GOLD: Gold Set for Another Strong Month of Gains

- Gold has has a solid start to Friday in Asia with gains of +0.73% to US$4,188.06.

- Gold in on track for another weekly gain, currently up just on 3% and over 4.6% for November and maintains its position above all major moving averages, with the 20-day EMA below at US$4,099.

- Gold's fortunes at present are strongly correlated with US rate cut hopes and with US Treasury traders off for Thanksgiving, gold had little new queues overnight.

- The India Pension Fund Regulatory and Development Authority (PFRDA) is planning to permit investment in gold and silver exchange traded funds, according to the chairman of the regulatory body (per BBG)

- Deutsche Bank raised its 2026 forecast for gold to an average of $4,450 an ounce over the year, up from $4,000 previously. Goldman Sachs last month boosted its projection for the end of next year to $4,900 an ounce from $4,300, citing ETF inflows and central-bank buying. (per BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

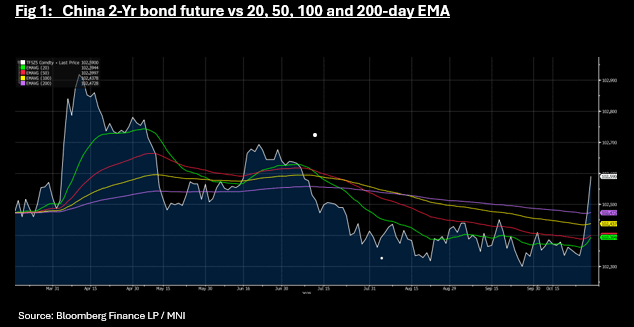

CHINA: Bond Futures Rally on Large Liquidity Injection

- The largest liquidity injection in recent weeks this morning has given bonds a boost, with bond futures up in morning trade.

- The 10-YR is up +0.19 to 108.61 trending back above all major moving averages.

- The 2-Yr bond future is up +0.11 to 102.58 for its largest one day jump since April. The move takes the 2-Yr above all major moving averages also.

- The CGB market hasn't reacted as strongly with the 10-Yr down -1bp to 1.80%.

- The PBOC governor indicated that the PBOC would re-enter the bond market and purchase CGB's according to Xinhua, without specify timing or amounts but with local commentators suggesting at present, amounts may not be significant. The 10-Yr CGB traded in a 1.60 -1.70% range from March through to July before breaking higher to 1.88% in late September. The PBOC has halted its bond buying this year, citing calm, stable markets and investors able to absorb issuance though with the move to equities from investors growing in strength, it seems likely that the PBOC may look to return the 10-Yr range back towards 1.60 -1.70%

FOREX: Higher Inflation Print Drives A$ & AUDNZD Higher, RBA Expected To Hold

Aussie is outperforming the G10 today after Q3 CPI printed higher than expected across the board and likely means that the RBA will be on hold on 4 November. The AUD OIS market has almost no chance of a cut priced in with only around 25% of 25bp for the 9 December decision. AUDUSD jumped to 0.6607 on the data release but has struggled to hold moves above 0.6600. It is currently up 0.2% to 0.6599. The USD index is flat and risk appetite mixed.

- The difference in Australia-NZ central bank expectations has pushed AUDNZD higher with it reaching 1.1427 following the Aussie CPI, highest since 9 October, and is now up 0.2% to around 1.1409. NZDUSD is slightly higher today at 0.5784 off the intraday low of 0.5772.

- The RBNZ is widely expected to ease in November but the RBA looks like being on hold as underlying inflation hit the top of its 2-3% band. The RBA has been more wary of the Q3 pickup in inflation than the RBNZ, which believes that spare capacity will bring it back towards 2%.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid.

- Acting RBNZ Governor Hawkesby speaks on central bank independence at 1705 NZT/1505 AEDT today. The speech will be published on the RBNZ website.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

FOREX: USD Stabilizes, Aided By Higher USD/CNH Levels

Softer USD sentiment from earlier has stabilized. The USD BBDXY index was last back above 1210.3, up from earlier lows near 1209. USD/CNH is up from fresh lows, while JPY and AUD have pared earlier gains. The AUD/NZD cross is still higher, holding above 1.1400 post the Q3 Australian CPI beat.

- USD/CNH has recovered some ground, with the market arguably looking for a lower USD/CNY fix (relative to mkt forecasts) to aid fresh downside. The pair was last back near 7.1000, with onshore spot also steady around 7.1000, another limit on CNH gains.

- US President Trump has spoken as travels to South Korea for the APEC summit (and meeting with China President Xi). He expressed confidence on the upcoming meeting with Xi and around lowering the tariff rate that China faces in relation to fentanyl. Market reaction has been limited though as the WSJ reported on such risks overnight. It stated tariff rates may come down to 10% from 20% (in relation to fentanyl), which would lower the average tariff rate China faces to around 45% from 55%.

- Elsewhere, AUD/USD is back under 0.6600 after spiking higher to 0.6607 post the stronger Q3 CPI print (which has seen RBA easing expectations move back close to flat). We were last 0.6590/95, but the A$ is outperforming versus NZD, the AUD/NZD cross back to 1.1415/20. NZD/USD was last under 0.5775

- USD/JPY got lows of 151.54, (which was still above the 20-day EMA) but last tracks around 151.95/00. US Tsy Bessent's earlier remarks aided the yen, as he stated the Japan government should give the BoJ the policy space it needs to keep inflation anchored and excessive FX volatility curbed.