ASIA FX: CNH Up 0.50% For Week, USD/KRW Supported On Dips

In North East Asia FX, all currencies are tracking higher against the USD over the past week (although KRW and TWD have lost a little ground so far today). CNH is an outperformer (up 0.50%) after USD/CNH broke to fresh YTD lows under 7.0700 (7.0653). We have seen the USD/CNY fixing bias turn positive, i.e. no longer supporting yuan appreciation. This may slow yuan gains, although moves in USD/CNH above 7.0800 have drawn selling interest so far. Lower US-CH yield differentials, along with potential for fresh conversion of foreign currency into CNY as we approach year end and into early 2026, is aiding yuan sentiment. Downside focus in USD/CNH will be around the 7.0500 region.

- Spot USD/KRW is also down this week, but has remained volatile. We were last near 1465/66, still within striking distance of recent highs near 1480. The BoK left rates on hold as expected, but the hawkish (explicit removal of easing bias), drove SK rates higher, although benefit to KRW was only fleeting. The FinMin also disappointed with no fresh measures to improve FX supply/demand imbalances. BOK Governor Rhee stated NPS hedging flows are too predictable and lack macro impact. Uncertainty around how the authorities will improve these imbalances is keep USD/KRW dips under 1460 supported for now.

- Spot USD/TWD sits off its recent highs, last near 31.35. Recent highs in the pair were around 31.49. The better equity tone (with nearly $1.5bn in offshore inflows) has helped sentiment. Note the 20-day EMA is around 31.17, as a potential downside support point. BBG notes: "At end of October, Taiwan life insurers’ hedging ratio dropped to 58.55%, an FSC official says at briefing" (which is the lowest since 202 per BBG).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Focus on US Tech Earnings as Regional Bourses Strong Again

The coming days will see key US tech stocks Microsoft Corp., Alphabet Inc., Meta Platforms Inc., Amazon.com Inc. and Apple Inc report earnings with key regional tech stocks looking to add to recent gains. Tech stocks like Samsung, SK Hynix Inc and TSMC have reached new highs in recent days as ongoing tech optimism is a key driver for Asia's major bourses. Investors will focus on new from the APEC Summit with hopes resting on the cooling of relations between the US and China, coupled with the announcement of various trade deals with Asian trading partners.

- The NIKKEI was again the star today up almost 2.00% with tech stocks leading with the US President's visit to Japan interpreted as positive for the tech stocks as their potential to become important in US supply chains.

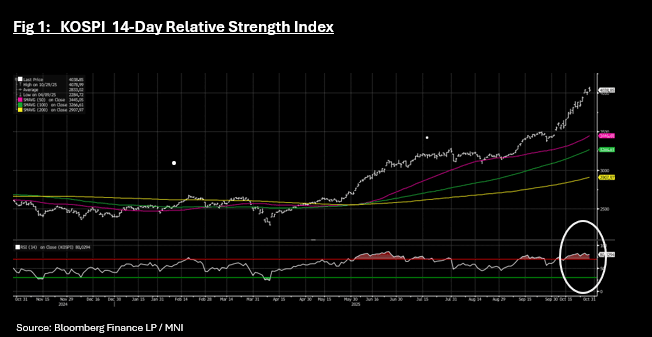

- The KOSPI bounced back from a rare down day yesterday to be up +0.71% today, and maintain its position above all major moving averages and for a second consecutive week maintain its position in overbought territory according to the 14-day RSI.

- China's major bourses saw an onshore offshore divide again with the HSI down -0.33% whilst the CSI 300 rose +0.48%, Shanghai up +0.37% and Shenzhen up +0.56%. The Hang Seng continues to lag its onshore counterparts down almost 2% over the last month whilst the CSI 300 is up over 2%.

- The Jakarta Composite is having it's worst run in some time, putting together four successive days of falls, after hitting recent new high of 8.274%. Today's modest losses sees the JCI maintain its position below the 20-day EMA.

- The hopes for a trade deal for India sees the NIFTY 50 reaching yet another new all time high of 25,993 and tips it into overbought area. P/E's on historical basis now are looking stretched and with a lot priced in in terms of optimism, any shortfall in trade deal could see a material retracement.

JGBS: Cash Curve Flatter, BoJ Seen On Hold, Focus on Dec/Jan Hike Risks

JGB futures are holding weaker, last 136.12, -.10 versus settlement levels. Some negative spillover has been likely today from the lunge in Aussie bond futures (post the CPI beat), while US futures have been quite steady ahead of the Fed later. For JGBs, we haven't been able to test under 136.00 at this stage, while important resistance is still some distance away on the upside.

- We also saw some modest downside pressure following earlier US Tsy Secretary remarks. Via X he said: "The Government’s willingness to allow the Bank of Japan policy space will be key to anchoring inflation expectations and avoiding excess exchange rate volatility."

- This comes ahead of tomorrow's policy meeting outcome, where little hike risks are seen by the economic consensus or market pricing. Focus will be on Dec/Jan hike risks and whether we see further dissenters who are in favour of a rate hike. We had 2 at the Sep board meeting, a shift to 3 would likely raise Dec hike risks.

- In the cash JGB space, the bias remains for flatter curves, the 2/30s down to +211bps. The 30-yr JGB yield looking to close under its 100-day EMA support (around 3.07% and we currently trade at 3.05%). The 10yr yield is relatively steady at 1.65%.

AUSSIE BONDS: Q3 CPI Beat Curbs 2025 Easing Pricing, 3yr Yield Eyeing 3.6% Test

Aussie bond futures have slumped, led by the front end, post the stronger than forecast Q3 CPI outcome. RBA easing expectations have been curbed dramatically. The end year implied rate is close to 3.54% (versus the current policy rate of 3.60%), with little easing risk seen in Nov. At the end of last week, the implied end year rate was around 3.37%. A full easing is not priced until the May meeting next year.

- ACGB yields have surged, led by the front with the 3yr up 12bps. This puts us at 3.57%, with focus on whether we can test above the policy rate of 3.60%. The 10yr is up 5bps to 4.22%.

- In the futures space, 3yr (YM) is off 12.5bps to 96.415, which is not too far away from late Sep/Early Oct lows sub 96.40. The 10yr (XM) is down 5.5bps to 95.76, piercing 20-day EMA support.

- For the cash 3yr bond, we made see buying interest emerge on a test of the 3.60% region, given risks of RBA easing into 2026. Focus will be on the next jobs report due on Nov 13th for Oct. A turn back lower in the unemployment rate is likely to push out easing expectations further, while a further rise could bring Q1 rate cut risks back into view.

- The AU 3/10s curve has flattened further to +65bps, down 7bps. The AU-US 10yr spread is up to +25bps, eyeing a fresh test around the +30bps level.

- Tomorrow on the data front we have Q3 trade prices.