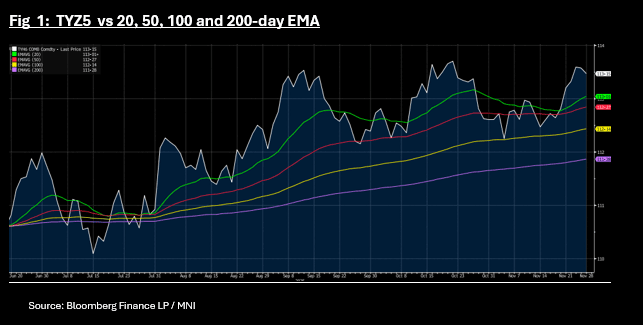

US TSYS: Bond Futures Down; 10-Yr UST Back Above 4%

US bond futures had a low volume day today as expected with the 10-Yr down -03 at 113-15+. TYZ5 maintains its position above all moving averages with the 20-day EMA below at 113-01+ and up for the week by +0-10.

Cash is lower with yields 1-1.5bps higher across the curve. The movement higher in yield takes the 10-Yr back above 4.00%. This is the fourth time over the last two months the 10-Yr has traded below the 4.00% level, but has been unable to maintain it there for very long.

- The US 2-Yr is at 3.495% - +1.6bps

- The US 5-Yr is at 3.579% - +0.9bps

- The US 10-Yr is at 4.013% - +1.7bps

- The US 30-Yr is at 4.658% - +1.5bps

It is widely anticipated that the market will remain quiet overnight with no auctions scheduled until next week, or economic data releases.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Q3 CPI Beat Curbs 2025 Easing Pricing, 3yr Yield Eyeing 3.6% Test

Aussie bond futures have slumped, led by the front end, post the stronger than forecast Q3 CPI outcome. RBA easing expectations have been curbed dramatically. The end year implied rate is close to 3.54% (versus the current policy rate of 3.60%), with little easing risk seen in Nov. At the end of last week, the implied end year rate was around 3.37%. A full easing is not priced until the May meeting next year.

- ACGB yields have surged, led by the front with the 3yr up 12bps. This puts us at 3.57%, with focus on whether we can test above the policy rate of 3.60%. The 10yr is up 5bps to 4.22%.

- In the futures space, 3yr (YM) is off 12.5bps to 96.415, which is not too far away from late Sep/Early Oct lows sub 96.40. The 10yr (XM) is down 5.5bps to 95.76, piercing 20-day EMA support.

- For the cash 3yr bond, we made see buying interest emerge on a test of the 3.60% region, given risks of RBA easing into 2026. Focus will be on the next jobs report due on Nov 13th for Oct. A turn back lower in the unemployment rate is likely to push out easing expectations further, while a further rise could bring Q1 rate cut risks back into view.

- The AU 3/10s curve has flattened further to +65bps, down 7bps. The AU-US 10yr spread is up to +25bps, eyeing a fresh test around the +30bps level.

- Tomorrow on the data front we have Q3 trade prices.

US TSYS: Treasuries Fail to Feature, As Markets Await APEC / FOMC

The US bond futures saw little or no movement in price today with volumes in the region mostly below average. TYZ5 is where it started the day at 113-15+, having inched up to 113-16+ briefly.

Cash was subdued also, with little expectations ahead of the FOMC meeting. Yields drifted marginally higher by up half a basis point.

- The US 2-Yr is at 3.498% (+0.6bps)

- The US 5-Yr is at 3.615% (+0.3bp)

- The US 10-Yr is at 3.981% (+0.4bp)

- The US 30-Yr is at 4.543% (+0.1bp)

Tonight markets focus on auctions for US$44bn of 2-Yr FRNs and various bills and notes.

Key data focus prior to FOMC will be mortgage applications, pending home sales and wholesale inventories. With much priced in now for bonds, the key risks remain any hawkish rhetoric from Powell, bringing into question future rate cuts. The 10-Yr continues to consolidate below 4.00% but any sense of uncertainty for future rate cuts could see the 4.00-4.15% reestablished. With so much riding on this week's cut and futures, the risks now are for disappointment and could see a move higher quicker in yields.

OIL: Crude Heading For Another Monthly Fall; Fed, EIA, US-CH & OPEC Key Events

Crude benchmarks are little changed today ahead of the Fed decision later and the release of EIA US oil market data. Prices have been supported by industry data showing a large US crude inventory drawdown. Brent is down 0.1% to $64.33/bbl after a high of $64.70 early in the APAC session before falling to $64.23. WTI is also 0.1% lower at $60.09/bbl after reaching $60.41. It fell to $59.95 but breaks below $60 have been short-lived. The USD index is up 0.1%.

- Bloomberg reported that US oil inventories fell a larger than expected 4mn barrels last week, after declining the previous week, according to people familiar with the API data. Gasoline and distillate were both lower down 6.3mn and 4.4mn respectively.

- With the focus on excess supply, a soft EIA report is likely to drive oil prices lower. They are down over 2.5% in October, which would be the third consecutive monthly decline.

- After today’s events, the market will be watching Sunday’s OPEC decision and the impact of the latest sanctions against Russia, as they cloud the outlook. Indian Oil said it wouldn’t discontinue its Russian crude purchases as long as they complied with sanctions. With restrictions focussed on the large Rosneft and Lukoil, both China and India refiners are looking to buy from smaller producers, according to Bloomberg.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.