ASIA STOCKS: Taiwan Leads Inflow Rebound, Tax Headlines Weigh On Kospi Flows

As the Nov trading month comes to an end, we have seen slightly better inflow momentum for tech sensitive plays South Korea and Taiwan. The last 3 trading days for Taiwan has seen almost $1.5bn in net offshore inflows. Still, this has only curbed Nov to date outflows to just over $10.5bn. As we enter into Dec, focus will be on broader equity trends (with the US Fed outlook an important driver), along with AI/chip demand into 2026. Local bellwether TSMC continues to recover from earlier Nov lows but remains off start of the month highs.

- For South Korea, we have seen close to $600mn in net inflows in the past 3 trading days. Interestingly today though is the contrast in Kospi and Kosdaq performance. The Kospi down 1.25%, but the Kosdaq up over 3.2%. This followed earlier reports via the Korea Economic Daily: "South Korea will push for an expansion of income tax deductions for Kosdaq venture funds, which invest a significant portion of their capital in venture cos." Per the NBUY function, offshore investors have sold around -$722mn of Kospi shares today, but added $230mn to the Kosdaq. To the extent this drives Kosdaq versus Kospi outperformance we may see more outflows from the Kospi by offshore investors.

- Indian inflow momentum is back positive for the past 5 days, with chunky inflows on Wednesday. This leaves Nov to date net inflows marginally in positive territory. The Nifty has consolidated its break above 26000 in recent sessions.

- In SEA, Indonesian inflow momentum has been pared slightly into month end. However, we still sit at a reasonable +$791mn for Nov as a whole. The JCI has been an outperformer in recent months amid hopes the government's pro-growth agenda boosts equity sentiment.

- Other SEA markets have seen outflows In Nov.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 46 | -1956 | -5279 |

| Taiwan (USDmn) | 687 | -2407 | -5692 |

| India (USDmn)* | 562 | 108 | -15712 |

| Indonesia (USDmn) | -17 | 119 | -1734 |

| Thailand (USDmn) | -27 | -97 | -3366 |

| Malaysia (USDmn) | 38 | -91 | -4543 |

| Philippines (USDmn) | -17 | -75 | -660 |

| Total (USDmn) | 1272 | -4398 | -36985 |

| * Data Up To Nov 26 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: “Material” CPI Miss & Consumer Recovery Drive Westpac To Exclude 2025 Cuts

The AUD OIS market has almost no chance of a cut priced in for the 4 November RBA decision with only around 25% of 25bp for the 9 December decision following the broadly higher-than-expected Q3 CPI data. The October Bloomberg survey showed that economists were not unanimous as to when they expected the next cut. Of the big four local banks, only Westpac forecasted a November easing but that has now changed.

- Given that inflation is higher than the RBA expected and the “emerging consumer recovery”, Westpac now expects rates to be unchanged over the rest of 2025. It is re-evaluating the 2026 outlook but sees the February meeting also in doubt given how much higher inflation is.

- It points out though that the labour market may surprise to the downside next year. The Q3 unemployment rate was higher than the RBA expected and employment growth slower.

- Westpac consumption data are suggesting “solid gains in Q3 and into Q4” and so it now expects the RBA to revise up its consumption profile.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum. However, it uses market rates in its model and they are higher which may allow inflation further out to return to the 2.5% band mid-point.

- RBA Governor Bullock said this week the Board remains cautious and more information is needed on inflation and the labour market given the volatility of the monthly numbers. She also described a 0.9% q/q Q3 CPI rise as a “material miss”.

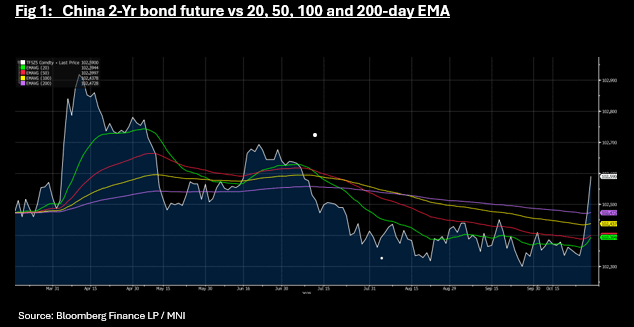

CHINA: Bond Futures Rally on Large Liquidity Injection

- The largest liquidity injection in recent weeks this morning has given bonds a boost, with bond futures up in morning trade.

- The 10-YR is up +0.19 to 108.61 trending back above all major moving averages.

- The 2-Yr bond future is up +0.11 to 102.58 for its largest one day jump since April. The move takes the 2-Yr above all major moving averages also.

- The CGB market hasn't reacted as strongly with the 10-Yr down -1bp to 1.80%.

- The PBOC governor indicated that the PBOC would re-enter the bond market and purchase CGB's according to Xinhua, without specify timing or amounts but with local commentators suggesting at present, amounts may not be significant. The 10-Yr CGB traded in a 1.60 -1.70% range from March through to July before breaking higher to 1.88% in late September. The PBOC has halted its bond buying this year, citing calm, stable markets and investors able to absorb issuance though with the move to equities from investors growing in strength, it seems likely that the PBOC may look to return the 10-Yr range back towards 1.60 -1.70%

FOREX: Higher Inflation Print Drives A$ & AUDNZD Higher, RBA Expected To Hold

Aussie is outperforming the G10 today after Q3 CPI printed higher than expected across the board and likely means that the RBA will be on hold on 4 November. The AUD OIS market has almost no chance of a cut priced in with only around 25% of 25bp for the 9 December decision. AUDUSD jumped to 0.6607 on the data release but has struggled to hold moves above 0.6600. It is currently up 0.2% to 0.6599. The USD index is flat and risk appetite mixed.

- The difference in Australia-NZ central bank expectations has pushed AUDNZD higher with it reaching 1.1427 following the Aussie CPI, highest since 9 October, and is now up 0.2% to around 1.1409. NZDUSD is slightly higher today at 0.5784 off the intraday low of 0.5772.

- The RBNZ is widely expected to ease in November but the RBA looks like being on hold as underlying inflation hit the top of its 2-3% band. The RBA has been more wary of the Q3 pickup in inflation than the RBNZ, which believes that spare capacity will bring it back towards 2%.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid.

- Acting RBNZ Governor Hawkesby speaks on central bank independence at 1705 NZT/1505 AEDT today. The speech will be published on the RBNZ website.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.