MNI EUROPEAN MARKETS ANALYSIS: Focus On US CPI Later

EXECUTIVE SUMMARY

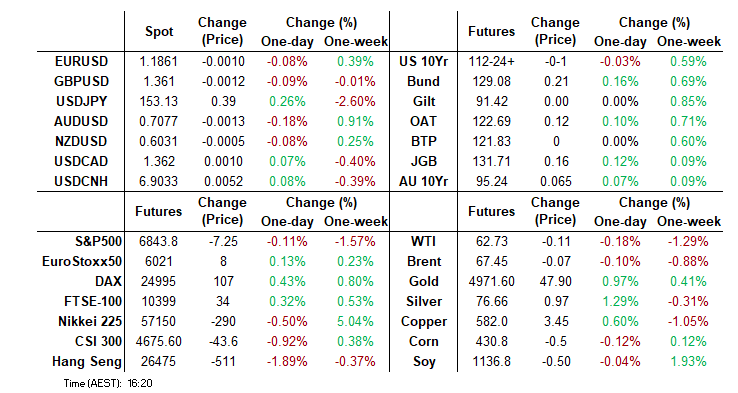

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's risk-off induced rally.

- NZGB yields follow global bond yields lower despite solid manufacturing PMI print and rising inflationary expectations.

- USD/JPY continues to be faded on any bounces as risk has turned lower.

- During the Asian trading day today gold prices have staged a moderate rebound. On Thursday, the precious metal plunged more than 3%, crashing below the psychologically significant $5,000 per ounce mark to a near one-week low.

- Friday’s focus shifts to Eurozone GDP, labour market and trade data, alongside remarks from BOE’s Pill. Globally, attention will centre on the US CPI release.

US TSYS: Risks Build for Higher CPI

For the bond market, the next filter to assess the future path of interest rates by is Friday's CPI (see MNI CPI Preview here). According to our US team, consensus is for a modest pick up in core prices MoM helped by a typical start of year price reset and normalization of activity since the government shutdown.

Treasuries have shown their willingness to rally with most maturities approaching Friday near to weekly lows in yield, thereby making CPI a critical test.

Cash is weak in Asia today with yields up +1-1.5bps across the curve.

- The 2-Yr is up +1.2bps at 3.47% : lower by -3.1bps for the week.

- The 5-Yr is up +1.2bps at 3.673%: lower by -8.7bps for the week.

- The 10-Yr is up +1.3bps at 4.113%: lower by -8.6bps for the week.

- The 30-Yr is up +1.3bps at 4.749%: lower by -10.2bps for the week.

The US 10-Yr future has fallen -01 today to 112-24+ on reasonably high volumes, suggesting good two way flow.

The risks now are to a higher CPI. Yields have moved considerably lower over the week and if our US team are correct and and there is an acceleration in prices, yields could give back much of those gains Friday.

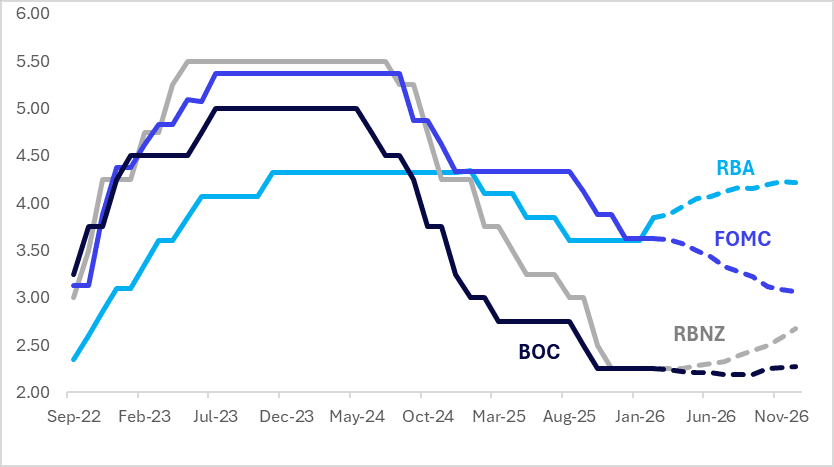

STIR: $-Bloc Pricing Little Changed Over Past Week

Interest-rate expectations across the $-bloc over the past week, looking out to December 2026, have been little changed.

- The key data release across the $-bloc over the past week was Wednesday’s release of Non-Farm Payrolls. Nonfarm payrolls growth was far stronger than expected in January at 130k (cons 65k) after negligible two-month revisions of -17k (mainly in Nov). Private payrolls saw a larger beat, both with the 172k (68k cons) in January but with also a two-month revision of +49k (fairly evenly split over Dec and Nov).

- The Household survey showed a stronger labor market than expected, with the unrounded unemployment rate of 4.283% not just below the consensus of 4.4% and 4.375% prior, but also the lowest since July.

- Today sees the release of January CPI data.

- The next major regional policy event is the RBNZ meetings on 18 February. No tightening is priced for February, while December 2026 assigns 43bps.

- Looking ahead to December 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.07%, -56bps; Canada (BOC): 2.27%, +2bps; Australia (RBA): 4.12%, +27bps; and New Zealand (RBNZ): 2.67%, +42bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Early Risk-Off Induced Gains Pared Ahead Of US CPI

JGB futures are stronger, +9 compared to settlement levels, but hovering just above session cheaps.

- MNI BRIEF: BOJ's Tamura See Higher Rate; No Timeframe: The Bank of Japan will continue raising policy interest rates to adjust the degree of monetary easing, said Board Member Naoki Tamura Friday, without committing to a specific timeframe. He added that inflation appears to be becoming more “endogenous and sticky,” reflecting the Bank’s targeted mechanism in which wages and prices rise interactively.

- "Japanese government bonds are largely shrugging off the latest remarks from central bank board member Naoki Tamura as those of a hawk, but they are eventually vulnerable to losses as his comments -- especially around the neutral rate -- underscore how far the policy rate may have to rise in this cycle." - BBG

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's risk-off induced rally. Focus is on the release of US CPI data later today.

- Cash JGBs have twist-steepened across benchmarks, with yields 1bp lower (5-10-year zone) to 2bps higher (30-year).

- Swap rates are 1-4bps higher, with a steeper curve.

- On Monday, the local calendar will see Q4 (P) GDP alongside Industrial Production (Dec F) and Capacity Utilization (Dec).

Source: Bloomberg Finance LP

JAPAN: Honda- BoJ Board Spots Don't Need To Be Filled With Reflationists - Rtrs

Headlines have crossed from Rtrs after an interview with Etsuro Honda, an economic advisor to Japan PM Takaichi (Honda was also an economic advisor to former Japan PM Abe). Honda states that there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. Via Rtrs: "While acknowledging the chance of another rate hike this year, Honda said the BOJ will likely avoid raising rates in March as it needs to scrutinise the impact of its hike in December." Yen may have seen some negative spill over on this headline. USD/JPY is back to 153.30, versus earlier lows of 152.67, although broader cross asset also look a little better, with gold, silver and US equity futures all up from earlier lows. March BoJ hike odds, per OIS pricing, look a touch lower, but haven't got above 30% in recent sessions.

- Honda also stated that upcoming BoJ board vacancies don't need to be filled by reflationists, as the country has exited deflation. Via RTrs: ""I don't necessarily think they need to be reflationists who are proposing powerful monetary easing," Honda said, when asked who should be chosen as new BOJ board members."

- Honda added that he thinks Takaichi understands that the economy is in a different phase from the Abe era.

- This is important in the context that Japan officials, including Takaichi, were stating late last year the country hadn't exited deflation. This is likely to reaffirm market viewpoints that the government may not push back on further BoJ policy normalization in 2026.

- Rtrs added: "Sources have told Reuters the government is set to submit to parliament as early as February 25 a nominee to replace Asahi Noguchi, whose term ends on March 31. Another board member, Junko Nakagawa, will also see her term expire at the end of June. Nominees must be approved by both chambers of parliament."

JAPAN DATA: Offshore Investors Sell Bonds Ahead Of Election, Equity Inflows Up

Last week saw the first week of net outflows from local Japan bonds by offshore investors since the end of 2025. Compared to earlier Jan inflows, the outflow was modest though and cumulative net inflows 2026 to date still sit near ¥4.75trln. This of course came ahead of last weekend's Japan election. The price action in JGBs this week has been encouraging amid assurances around the fiscal/bond issuance outlook and expectations that the government won't stand in the way of BoJ policy normalization. The 10yr JGB is around 2.20%, while longer dated yields continue to correct of Jan highs (30yr back to 3.41%). Focus will be on whether we see further foreign interest come into this space for this past week.

- Offshore interest in Japan equities continues, with a further firm inflow last week. This takes the consecutive weeks of net buying of Japan stocks to seven. Given the break higher in local stock indices this week, that trend may well have continued.

- In terms of Japan outbound flows, we saw local investors selling offshore bonds. Since the start of the year cumulative outflows in this space have been close to flat. Global bond returns have picked up this week amid the US Tsy yield retreat.

- Local investors continued to buy offshore stocks, albeit in more modest size compared to the prior week.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Feb 6 | Prior Week |

| Foreign Buying Japan Stocks | 543.2 | 494.6 |

| Foreign Buying Japan Bonds | -464.1 | 2081.1 |

| Japan Buying Foreign Bonds | -365.7 | 713.7 |

| Japan Buying Foreign Stocks | 162.7 | 454.6 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Richer But Off Bests Ahead Of US CPI Data, Curve Flattens Further

ACGBs (YM +5.5 & XM +6.5) are stronger but off session bests.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session. Focus is on the release of US CPI data later today.

- “Angus Taylor faces a byelection test in the NSW seat of Farrer after wresting leadership from Sussan Ley. One Nation will run a "strong candidate" in Farrer, and other parties including the Liberals, Nationals, and teals are also expected to contest. Taylor was entrusted by colleagues to salvage the Liberal Party with a strong victory in Friday's leadership ballot, beating Ley by 34 votes to 17.” - BBG

- Cash ACGBs are 5-6bps richer with the AU-US 10-year yield differential at +64bps.

- Cash 3/10 curve flattens to lowest since end-2024.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 16% for March to 93% by June and 148% by December 2026.

- Tomorrow, the local calendar will be empty ahead of RBA Minutes of Feb. Policy Meeting on Tuesday.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 3.25% 21 April 2029 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Richer With A Flatter Swap Curve After Higher Infl Expns

NZGBs closed 4-5bps richer across benchmarks, albeit slightly off session bests.

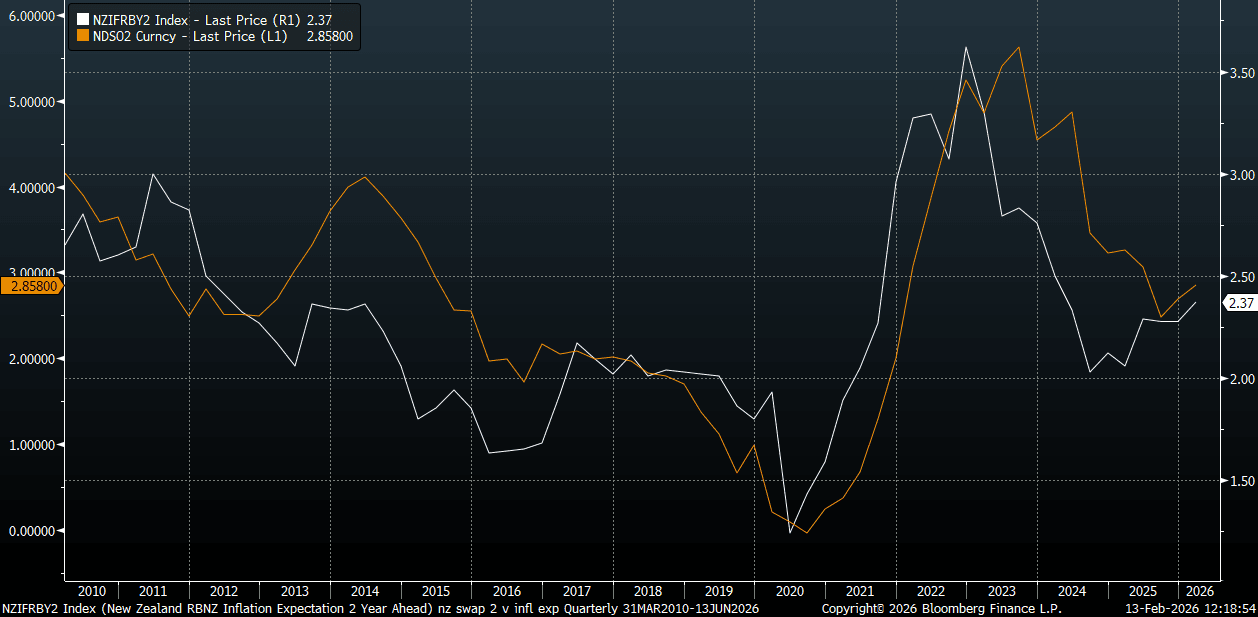

- NZ 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This was the highest since Q1 2024 for the print. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%.

- 1yr ahead inflation expectations posted a firmer rise to 2.59% from 2.39%, but likewise remain well off end 2022 highs (just above 5.0%). The data point to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term (the RBNZ meets next Wed, Feb 18).

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's risk-off induced rally. Focus is on the release of US CPI data later today.

- NZ-US and NZ-AU 10-year yield differentials finished ~1bp wider.

- Swap rates closed 2-4bps lower, with a flatter 2s10s curve and wider implied swap spreads.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 42bps.

- On Monday, the local calendar will see the Performance Services Index and Card Spending data.

Bloomberg Finance LP

NEW ZEALAND: Inflation Expectations Edge Up But From Low Levels

New Zealand 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This is highs back to Q1 2024 for the print, but the trend rise has been very modest over this period. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%. The chart below plots the 2yr ahead inflation expectations versus the NZ 2yr swap rate (which is the white line). 1yr ahead inflation expectations posted a firmer rise to 2.59% from 2.39%, but likewise remain well off end 2022 highs (just above 5.0%). The data point to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term (the RBNZ meets next Wed, Feb 18).

- The 5yr and 10yr inflation expectations edged a little higher to around 2.30%. The cash rate expectation was at 2.58% for 1yr ahead, versus 2.31% prior.

Fig 1: NZ 2yr Ahead Inflation Expectations & NZ 2yr Swap Rate

Source: Bloomberg Finance L.P./MNI

FOREX: USD - BBDXY Trying To Bounce Off 1180

The BBDXY has had a range today of 1181.81 - 1183.05 in the Asia-Pac session; it is currently trading around 1182. The USD continues to hold above 1178-1180 and with risk turning lower it is attempting to move higher. We have seen this movie before with respect to a potential correction in risk and recency bias tends to dismiss it evolving into anything more. The market is very bearish the USD and if we should get some form of a deeper correction in risk and the USD finds demand as a hedge, the market is not positioned for this. Most shorts will be eagerly awaiting the potential ruling by the Supreme court on the Tariffs next week, 20 February. On the day, the first resistance is toward the 1185-1187 area and then 1195 where I suspect we could see sellers return. A sustained break below 1175-1180 is needed to potentially signal the start of another leg lower targeting 1150 first and then potentially 1115.

- EUR/USD - Asian range 1.1863-1.1873, Asia is currently trading 1.1870. The pair traded sideways below 1.1900 albeit with a heavy tone. Price action remains constructive, can it build a base above 1.1800 and then find the momentum to push on? On the day, the first support is back toward 1.1820-1.1850 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 is needed to give it the thrust it needs to have another look toward the 1.2000 area. Quite a lot of optionality is expiring in the 1.1800-1.1850 area today.

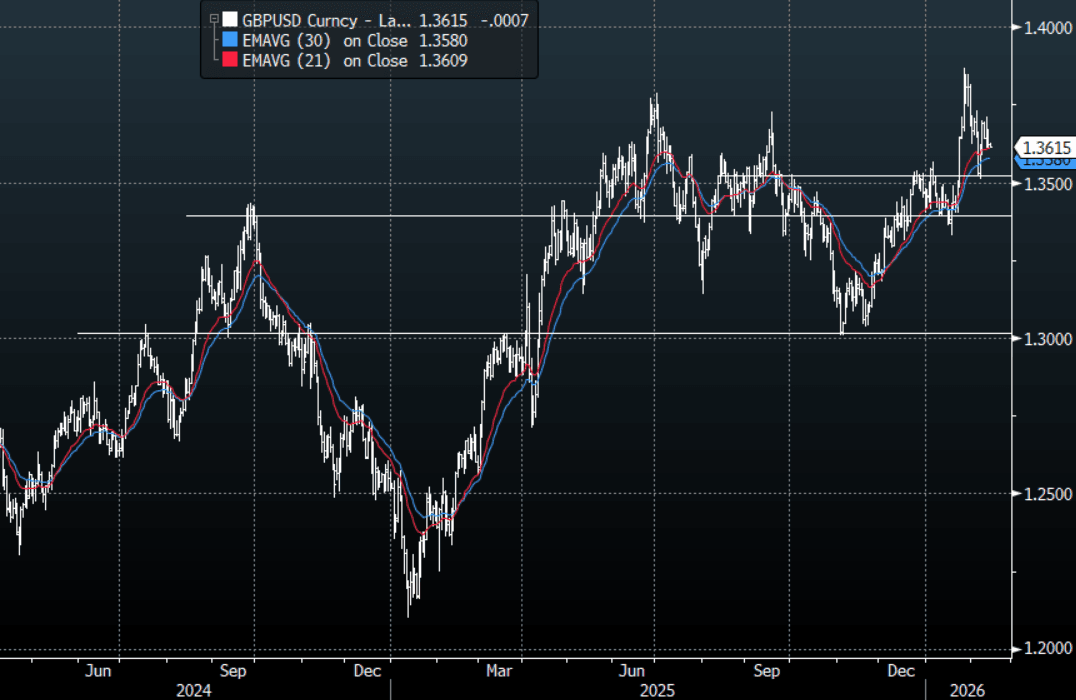

- GBP/USD - Asian range 1.3612-1.3627, Asia is currently dealing around 1.3620. The pair is trading pretty poorly considering how weak the USD has been. GBP continues to look like 1.3580-1.3730 to me for now as we wait to see how the big USD trades as risk stumbles, could CPI today give it the nudge it needs ?

- Cross asset : SPX -0.05%, Gold $4975, US 10-Year 4.11%, BBDXY 1182, Crude Oil $62.75

- Data/Events : Germany Wholesale Price Index, Spain CPI, EZ GDP/Trade Balance/Employment

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

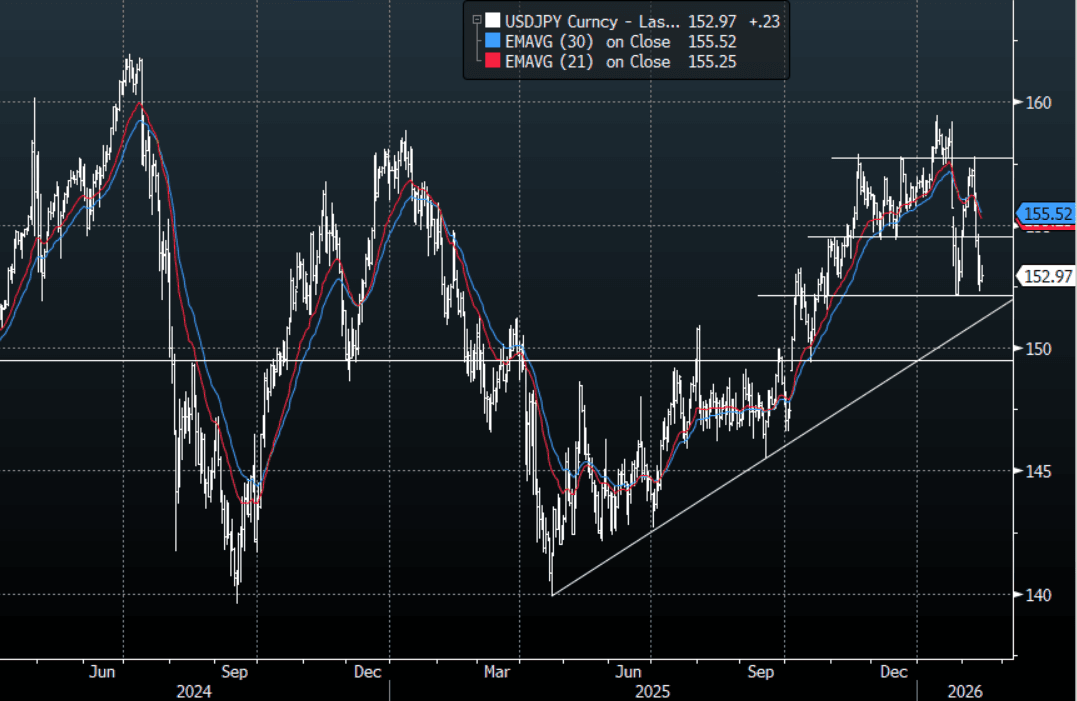

JPY: USD/JPY - Chops Around 153.00 As Longs Continue To Be Pared Back

The USD/JPY range today has been 152.67-153.35 in the Asia-Pac session, it is currently trading around 152.95, -0.15%. USD/JPY continues to be faded on any bounces as risk has turned lower. The headwinds for Yen shorts are growing and squeezing out the leveraged funds. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.25-153.75 and then 154.50-155.00 area as the market pares back its overextended USD longs and looks for another base to form from which to potentially move higher again.

- "BOJ BOARD MEMBER TAMURA: PERSONALLY FEEL JAPAN'S RECENT INFLATION IS BECOMING STICKY, TO KEEP RAISING RATES IF OUTLOOK IS MET” - BBG (tamura sits on the hawkish side)

- "BOJ'S TAMURA: I HAVE SAID NEUTRAL RATE IS AT LEAST AROUND 1%" - BBG

- MNI AU - Honda- BoJ Board Spots Don't Need To Be Filled With Reflationists - Rtrs: Honda states that there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. Via Rtrs: "While acknowledging the chance of another rate hike this year, Honda said the BOJ will likely avoid raising rates in March as it needs to scrutinise the impact of its hike in December.". March BoJ hike odds, per OIS pricing, look a touch lower, but haven't got above 30% in recent sessions

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.00($1.78b). Upcoming Close Strikes : 149.60($869m Feb 17), 151.00($986m Feb 17),156.00($1.87b Feb 17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 161 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

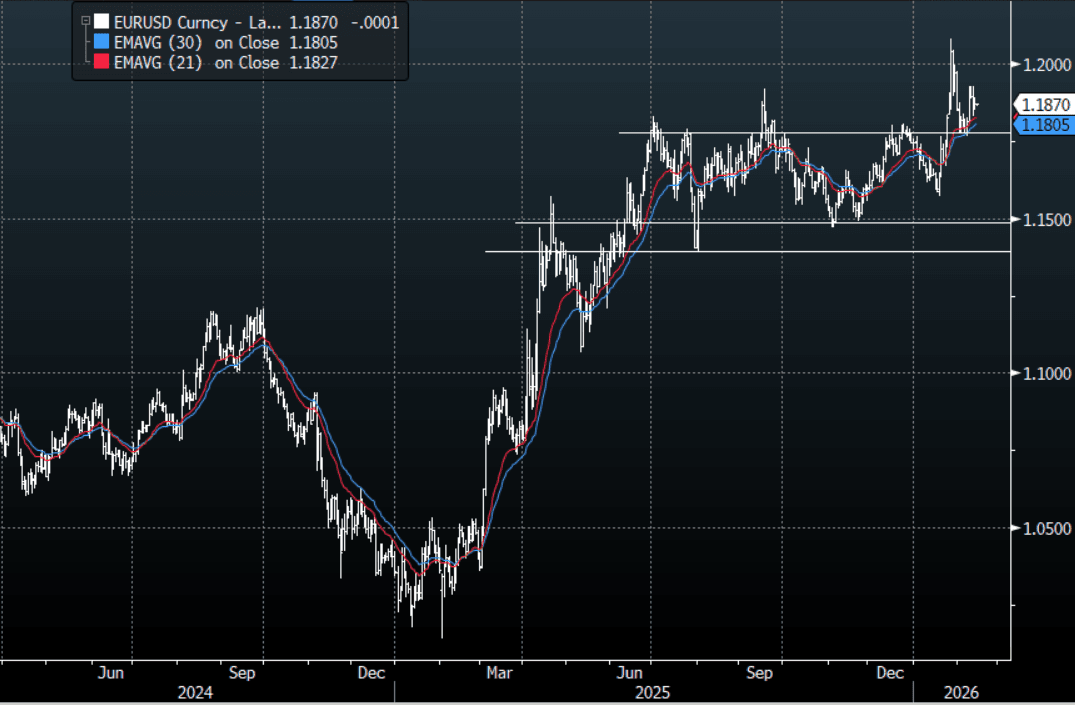

EURUSD: EUR/USD - Trading Sideways, Decent Optionality Toward 1.1800-1.1850

The EUR/USD range overnight was 1.1856-1.1890, Asia is currently trading around 1.1870. The pair trades sideways below 1.1900 albeit with a heavy tone. Price action though remains overall constructive, can it build a base above 1.1800 and then find the momentum to push on? On the day, the first support is back toward 1.1820-1.1850 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 is needed to give it the thrust it needs to have another look toward the 1.2000 area. Quite a lot of optionality is expiring in the 1.1800-1.1850 area today.

- “BofA boosted its year-end target for German 10-year yields to 3%, from 2.75%, citing stronger domestic economic growth and the ECB keeping rates on hold.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.1800(EU3.24b), 1.1850(EU5.25b), 1.1950(EU2.66b). Upcoming Close Strikes : 1.1900(EU1.22b Feb 17), 1.1950(EU999m Feb 17), 1.2000(EU1.36b Feb 18 ) - BBG

- The EUR/USD Average True Range for the last 10 Trading days: 61 Points

Fig 1 : EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

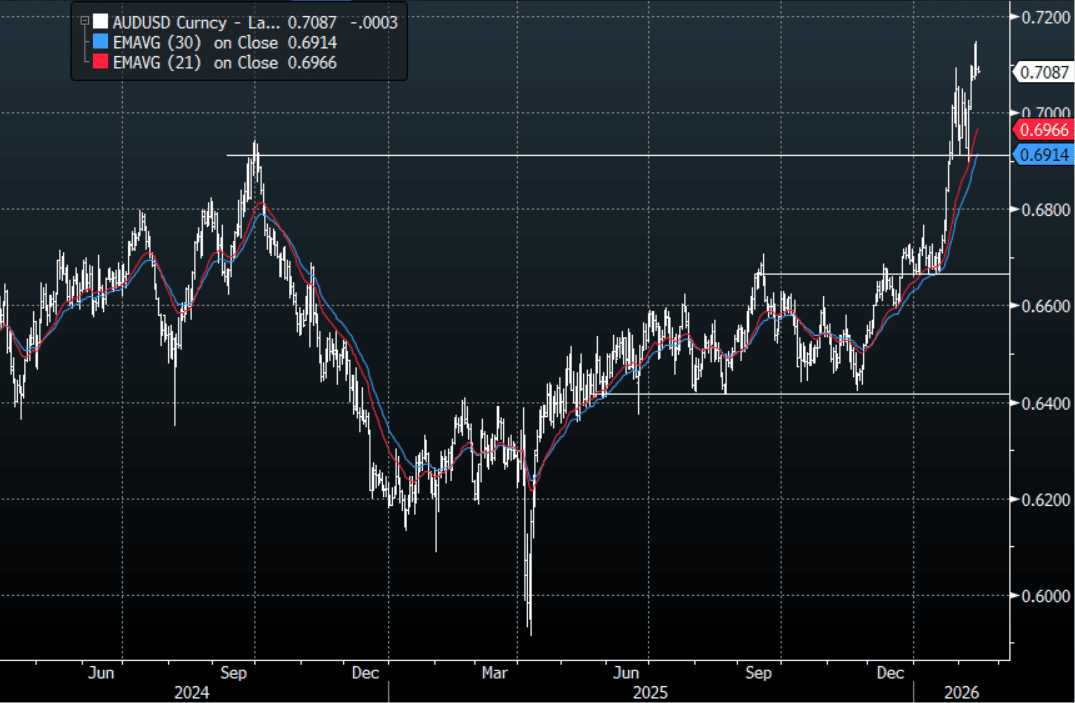

AUD/USD - Drifts Below 0.7100 As Risk Wobbles Into US CPI

The AUD/USD has had a range today of 0.7081 - 0.7097 in the Asia- Pac session, it is currently trading around 0.7088. The AUD move higher finally stalled toward 0.7150 as we had a “traditional risk-off” session in New York as stocks got sold, treasuries bought and the USD drifted higher. The AUD fell back below 0.7100 pretty easily and the bulls will be hoping for risk to firm up as they will be vulnerable if it builds into anything more than a pullback. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward 0.7035–0.7065, a break below here could signal a deeper pullback as the 0.7100-0.7200 continues to cap the move higher. The US CPI tonight will be closely watched and could add to the headwinds already building for risk.

- Bloomberg - “Australians’ Spending Set to Slow as Rate Hikes Bite, CBA Warns. “While consumers have continued to spend, higher interest rates and easing income growth are likely to slow that momentum as the year progresses,” CBA said in the report.”

- MNI BRIEF: Miran Says Fed Is Biggest Risk To U.S. Growth. "I think it's us," Miran said in Q&A at a Dallas Fed event, when asked about the biggest risk to growth. "The biggest risk I think to the economy is that we're misconstruing just how tight monetary policy is."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6800(AUD1.55b), 0.6825(AUD791m). Upcoming Close Strikes : 0.6980(AUD644m Feb 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 78 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

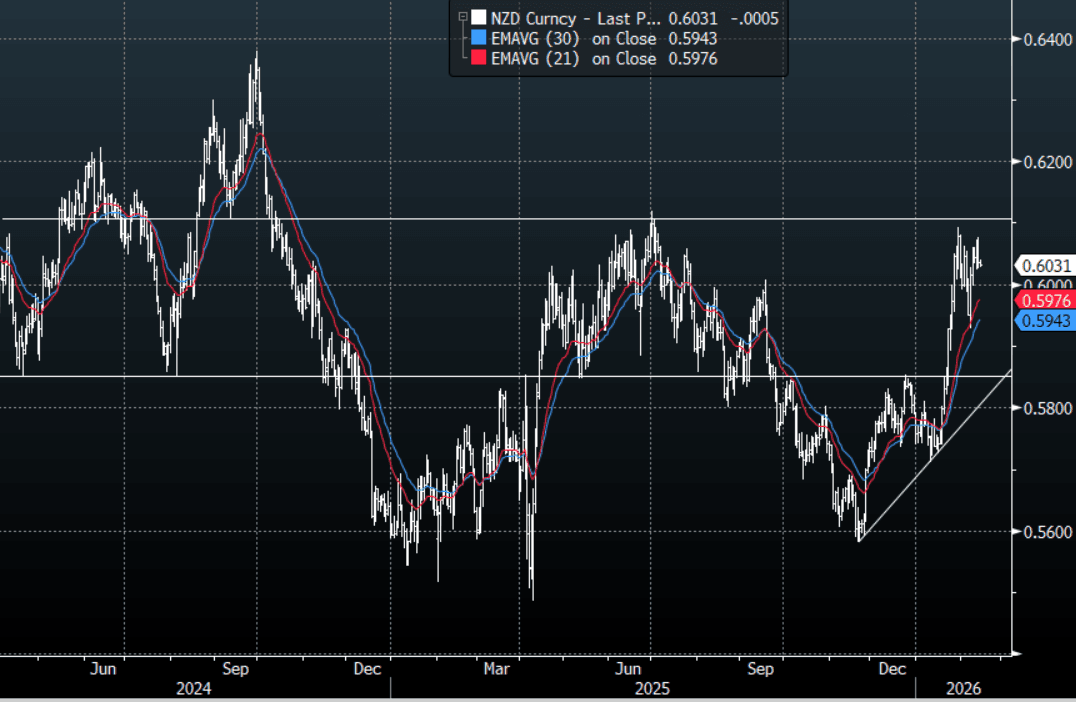

NZD/USD - Drifts Back Towards 0.6000 As Risk Turns Lower

The NZD/USD had a range today of 0.6028-0.6040 in the Asia-Pac session, it is currently trading around 0.6032. The NZD has again failed back toward the 0.6100 area as risk topped out again last night and the USD pulled back. We have seen this movie before so the question is whether risk actually breaks down and we get a decent correction or are the dips once again supported and we continue to chop sideways. Recency bias suggests the latter but there does seem to be some trouble brewing under the hood. On the day, the first support is back toward 0.5985-0.6015 a break below here could signal a deeper pullback toward 0.5900. For now the 0.6100 area continues to cap but the bulls will be hoping for risk to firm up to have another go.

- MNI AU - PMI Off Dec Highs But Still Pointing To Firm Growth Outlook: The BusinessNZ manufacturing PMI eased slightly in Jan, but maintained the bulk of the improvement we saw late last year. We printed at 55.2, versus 56.1 in Dec (the 56.1 read was the highest print since late 2021). The Jan outcome is still pointing to supportive cyclical conditions. The sub indices moved off Dec highs, with new orders at 56.4, versus 59.9 prior. The employment index printed at 52.9 (versus 53.7 prior), but we are above 2025 lows.

- MNI AU - NZ Inflation Expectations Edge Up But From Low Levels: New Zealand 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This is back to Q1 2024 highs for the print, but the trend rise has been very modest over this period. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%. 1yr ahead inflation expectations posted a firmer rise to 2.59% from 2.39%, but likewise remain well off end 2022 highs (just above 5.0%). The data points to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD400m Feb18), 0.6050(NZD395m Feb 16), 0.6200(NZD430m Feb 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 57 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Asia's Chip Surge Collides with US Tech Tremors

Major Asian equity markets fell today as a global sell-off in technology shares triggered by concerns over artificial intelligence (AI) valuations, dampened risk appetite. A sharp overnight slide in U.S. tech shares—specifically the Nasdaq falling 2%—spilled over into Asia. Investors are reassessing high AI-linked valuations following disappointing margin outlooks from major tech firms like Cisco, which cited surging memory chip costs. Despite the daily losses, many regional benchmarks are on track to end the week with significant gains, supported by recent strong corporate earnings and massive AI-related capital expenditure plans.

After a spectacular start to the week following a decisive election victory for the LDP, the NIKKEI closed Tuesday at fresh highs of 57,650. Nearing the end of the week it is at 57,256 around -0.70% lower. Major tech company Softbank fell heavily Friday by -7.7% yet remains higher on the week following earlier gains.

As the Lunar New Year holiday approaches and following strong gains to start the week, China's major bourses are down -0.80-1.80% Friday whilst holding onto gains of +1.8% for tech heavy Shenzhen.

The KOSPI is the outlier today posting gains of +1% and +9.6% for the week with Samsung Electronics up over +13% as the company announced it had commenced mass production and shipment of sixth-generation High-Bandwidth Memory (HBM4) chips, critical for next-generation AI accelerators.

The tech sell off has erased gains at the start of the week for the NIFTY 50 as it now faces its third week out of four of losses; down -0.54% currently.

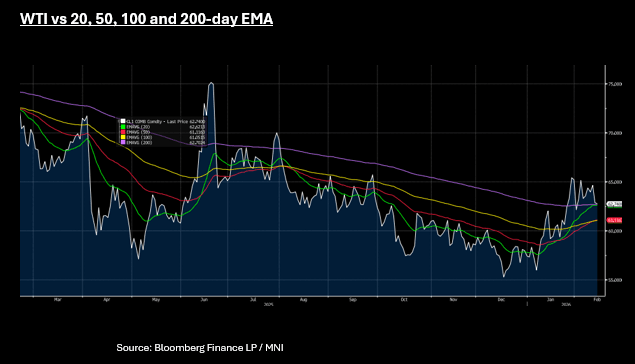

Oil Set for Weekly Loss as US Iran Tensions Moderate

- Oil prices slipped marginally in the Asia trading day and are set to finish down for the week as immediate US Iran concerns moderate.

- Following meetings with Israel's President Netanyahu this week, US President Trump suggested that negotiations with Tehran could last as long as a month, but cautioned that failure to reach an agreement could be 'very traumatic' for Iran.

- The weak is ending on a softer note for investor sentiment, dragging equities and oil with it. WTI is down modestly today and -1.2% for the week at US$62.75 bbl having traded in a tight range of $62.39 - $65.83

- WTI is currently near its downside resistance via the merged 20-day / 200-day EMA at $62.70. A break below sees resistance via the 50-day EMA of $61.11

- Brent is down just -0.07% today at US$67.47 bbl, and down -0.85% for the week. Brent has traded in a relatively narrow range of $67.02 - $70.72 over the last 5 trading days.

- For both WTI and Brent at present, momentum indicators are broadly neutral.

- US Energy Secretary said that energy companies who lost billions when Venezuela nationalized the oil industry in the 70s. Secretary Wright said on BBG TV that “They are in active discussions with ConocoPhillips — the people that lost assets in the before, are all in active dialog right now to recoup losses.”

- In the short term oil markets will likely return focus back to the issue of oversupply until further news breaks on US Iran discussions.

- Most forecasters see oil finishing lower by year end once geopolitical tension with Iran subside.

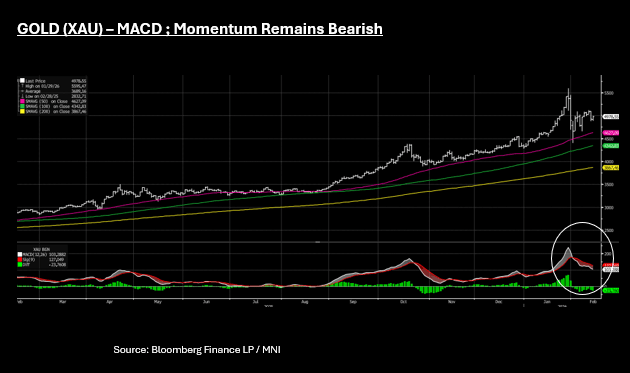

Gold Up; Remains Below $5,000 Awaiting US CPI

- During the Asian trading day today gold prices have staged a moderate rebound, climbing +1.2% to US$4,985. This follows a dramatic sell-off on Thursday where the precious metal plunged more than 3%, crashing below the psychologically significant $5,000 per ounce mark to a near one-week low. Market commentators were left scratching their heads as to the driver of Thursday's sell off, with the reality likely that the ripples of the late January falls are still being felt.

- Gold is holding on to weekly gains of just +0.3% as investors wait for the January CPI report in the US later, looking for clues as to the future direction for interest rates. The bullish case for gold in the near term hinges on a weak US CPI bringing rate cuts into play whilst a stronger CPI takes them off the table.

- The current market sentiment remains cautious and likely supported by dip buyers today as bullion holds above the $4,900 support level. Some momentum indicators point a different picture with the MACD (white) line below the Signal (red) line - a bearish sign for prices.

- Geopolitical tensions have taken a backseat in recent days with fresh news from US Iran talks limited with any spike in tensions likely to remain supportive for gold prices.

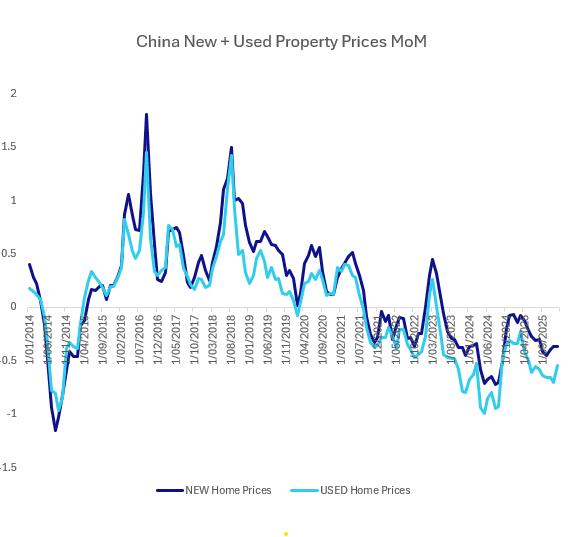

CHINA: No Let Up in Property Declines

- January property price data showed no let up in the fall of new and used prices, marking almost 3-years of declines.

- New home prices declined -0.37% MoM in January, with Shanghai flat and Beijing down -0.30%.

- New homes have now declined -3.3% YoY, accelerating from the December release of -3.05%

- Used home prices declined -0.54% in January, less than December but down -6.2% YoY, from -6.07 in Dec.

- Whilst overall sentiment remains weak, some major cities saw a jump in sales of used properties. In Shenzhen, transactions reached a 10-month high in January, suggesting that lower prices are finally starting to tempt some buyers back into the market.

- Reports surfaced this week suggest the Shenzhen government is considering a rescue package to prevent a default by China Vanke. According to stories in Reuters and Macao News which report that local authorities are drafting a package worth approximately 80 billion yuan ($11.58 billion) The preliminary plan reportedly includes a CNY20bn share placement to inject immediate liquidity into the developer. This move follows specific central government guidance aimed at preventing further defaults among state-backed developers as the property sector remains under severe strain.

- Investors look ahead to the upcoming party meeting in March for the next steps in policy to support the economy.

CHINA: CGB10-YR Below 1.8%; Expectations for RRR Cut Post LNY

- China's bond futures are lower Friday, but set to finish the week higher ahead of the lunar new year holiday.

- This week the PBOC has injected considerable liquidity with over CNY1tn via the daily OMO and today through the sale of CNY 1tn 6-month o/r reverse repo.

- CGB 10-Yr ended the week last week at 1.81% and with forecasts for significant liquidity injections proving correct, looks set to consolidate below 1.80% for the first time since November. The CGB 10-Yr is currently at 1.785%

- The 10-Yr bond future is down -.21 today at 108.47, flat for the for the week.

- The 2-Yr bond future is down -.01 today at 102.49 and up +.02 for the week.

- Onshore reports suggest that post LNY markets could see a RRR cut. Consensus being for a 50bps reduction to 8.50% and the release of CNY1tn of liquidity.

- The release of capital would help facilitate further bank lending and support bond yields as issuance plans ramp up for the government in March.

- This could see the range for the 10-Yr reset down to 1.70 -1.80%, having been in the 1.80 -1.90% range since November.

SOUTH KOREA: Yields Track Global Leads, 3Yr Yields to Remain Elevated

- As JGB futures open strong again Friday, SK bond futures have followed the lead higher and have gained for four days straight.

- Earlier this week we noted momentum for yields on the upside was firm but value demand might emerge in a risk off scenario or directional change in JGBs. See here post from the start of the week https://www.mnimarkets.com/articles/near-term-bias-for-higher-as-valuations-looking-attractive-1770607777752

- 10-Yr bond futures are up +.37 at the open as equity sentiment appears heavy for the day ahead.

- SK government officials have commented on SK bond yields (specifically 3-Yr) in recent day suggesting its is 'just market forces'.

- From a Feb 9 high of 3.27% the KTB 3-Yr yield has declined -14bps in recent days currently near 3.13%

- Yields in the 1-3 year maturities have been impacted by vast issuance by the government in the first 6 weeks of the year. The turn lower is driven by correlations to JGBs which are rallying given the easing of fiscal concerns.

- The issuance in the front seems set to continue, putting a floor under yields. We see cause of 3% as a natural floor in the 3-Yr thanks to global leads, but ultimately yields to stay elevated due to government bond issuance.

KRW: Equity Dip May Weigh Ahead of LNY Break, But USD/KRW Well Under Feb Highs

Spot USD/KRW lows on Thursday got close to the 200-day EMA support point, 1431.45. We finished up higher at 1439.1, with tech led equity market risk off aiding USD related safe have demand (JPY and CHF were outperformers in the G10 FX space though). The SOX lost 2.5% in Thursday US trade, while the MSCI IT index fell by 2.59%. The Kospi finished above 5500 yesterday, fresh record highs, while offshore investors added +$2bn to local stocks, further paring back recent outflows. Reversal of these trends, to some extent today, given US Thursday moves, may create upside USD/KRW pressure.

- Still, we are some distance from earlier Feb highs (just above 1475). Before then we have 1445.5, the 100-day EMA, which may now act as a resistance point, while moves above 1460 may also draw selling interest. On the downside, late Jan lows were close to 1420.

- South Korean markets are closed for the LNY break from next Mon through Wed, returning Thursday, Feb 19). Via BBG: "Finance Minister Koo Yun Cheol will hold a meeting at 8am local time to review financial market trend ahead of Lunar New Year holiday. "

- On the data front, earlier we had Jan trade prices, with import prices up 0.4%m/m, but down -1.2% y/y. Export prices were up 4.0%m/m, +7.8%y/y.

- Later on we get Dec money supply figures.

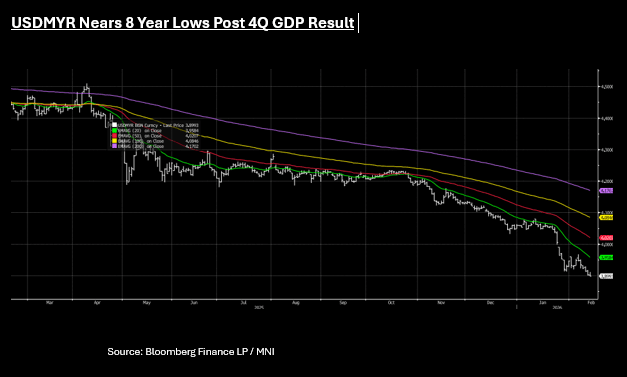

MALAYSIA: GDP Beat Gives Ringgit a Boost

- As the Malaysian growth outlook goes from strength to strength, so to does the Ringgit.

- Against expectations of 4Q expansion of +5.7%, the Malaysian economy grew +6.3% in the 4Q according to today's release. Against a government target for 2026 of 4 - 4.5% the 4Q result could see upward revisions coming.

- Growth was broad-based across major sectors: Manufacturing grew by 6.1% (up from 4.1% in 3Q), driven by electrical and electronic (E&E) products and food processing. Construction maintained double-digit growth at 11.0%, supported by non-residential and specialized construction activities. Services expanded by 6.3%, led by wholesale and retail trade, as well as tourism and agriculture saw a marked improvement to 5.4% due to higher oil palm production.

- Despite moving higher earlier in the day, USDMYR has moved lower post the release by -.0035 to be near 3.8980 / 3.9025 and daily gains for the Ringgit of +.09% and near 8 year lows for the cross.

- The last time USDMYR was sub 3.90 was back in 2018 when GDP expanded +4.7% for the year.

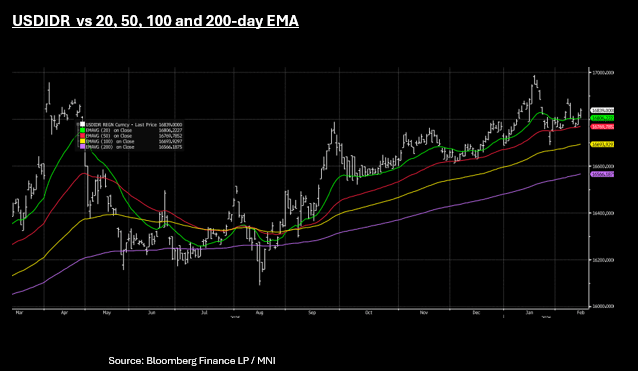

IDR: Rupiah Weakens Further, BI on Hold Next Week

- A second day of losses sees the Rupiah holding on to small gains for the week.

- USDIDR is up +15 today to be near 16,838 /16,848 as it consolidates back above the 20-day EMA of 16,813.

- Weekly Rupiah gains are hard to come by and the ailing currency is holding onto gains of +.21%

- The BI meets on Feb 19 next week with current consensus from forecasters for no change. With 150bps of cuts last year, the BI is focused on improving the transmission mechanism for rates and stabilizing the Rupiah, with both challenges needing considerable attention. We see the BI on hold next week in further support of the currency and in a week impacted by lunar new year, expect the rupiah to trade in a Rp16,750 - 16,900 range.

- On Wednesday this week the central bank reiterated its commitment to stabilizing the rupiah through measured interventions in the spot market and domestic non-delivery forward (DNDF) markets as the next meeting to decide monetary policy approaches.

- The Ministry of Finance stated this week that it is working closely with BI to synchronize fiscal and monetary policies to ensure the rupiah remains within a projected 2026 range of IDR 16,500 to 16,900 per dollar.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 13/02/2026 | 0700/0800 | * | Wholesale Prices | |

| 13/02/2026 | 0730/0830 | *** | CPI | |

| 13/02/2026 | 0800/0900 | *** | HICP (f) | |

| 13/02/2026 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 13/02/2026 | 1000/1100 | * | Employment | |

| 13/02/2026 | 1000/1100 | * | Trade Balance | |

| 13/02/2026 | 1000/1100 | ECB's de Guindos Lecture At Academia Europea Leadership | ||

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event | ||

| 13/02/2026 | - | BOE MPG Minutes Released | ||

| 13/02/2026 | - | *** | New Loans | |

| 13/02/2026 | - | *** | Money Supply | |

| 13/02/2026 | - | *** | Social Financing | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1330/0830 | ** | US CPI Annual Revised | |

| 13/02/2026 | 1330/0830 | *** | CPI | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |