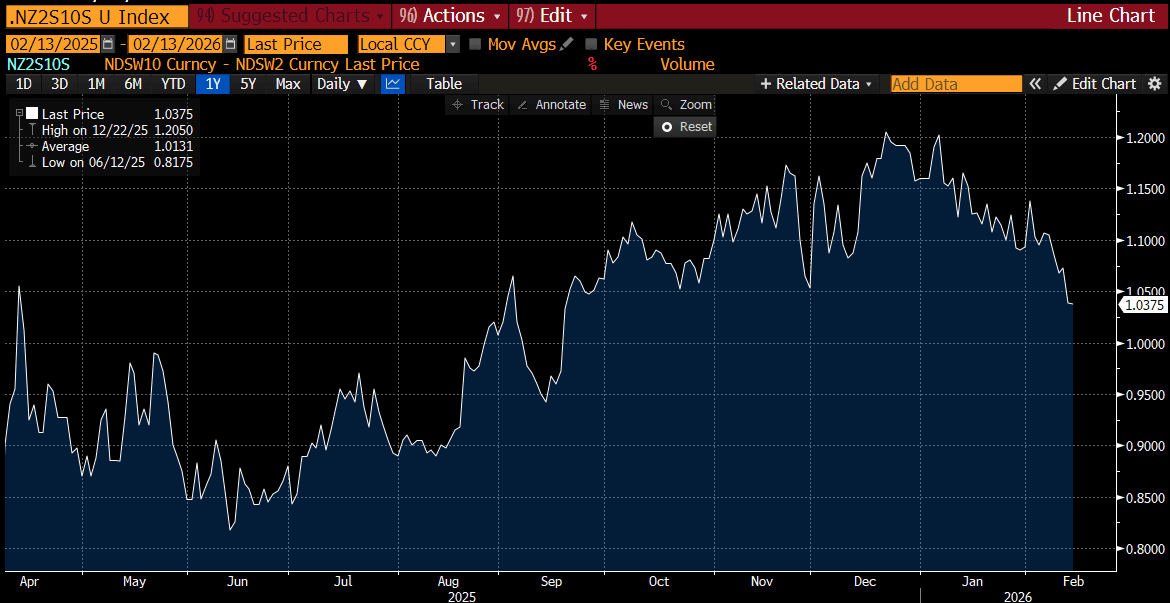

BONDS: NZGBS: Richer With A Flatter Swap Curve After Higher Infl Expns

NZGBs closed 4-5bps richer across benchmarks, albeit slightly off session bests.

- NZ 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This was the highest since Q1 2024 for the print. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%.

- 1yr ahead inflation expectations posted a firmer rise to 2.59% from 2.39%, but likewise remain well off end 2022 highs (just above 5.0%). The data point to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term (the RBNZ meets next Wed, Feb 18).

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's risk-off induced rally. Focus is on the release of US CPI data later today.

- NZ-US and NZ-AU 10-year yield differentials finished ~1bp wider.

- Swap rates closed 2-4bps lower, with a flatter 2s10s curve and wider implied swap spreads.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 42bps.

- On Monday, the local calendar will see the Performance Services Index and Card Spending data.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 5-Year Supply Shows Lacklustre Demand Metrics

Today’s 5-year JGB auction delivered weakish demand signals. The low price was below expectations at 99.81, the bid-to-cover ratio fell to 3.0811x from 3.1676x, and the tail widened to 0.05 from 0.04.

- The result aligns with the weakish results seen at this month’s 10-year and 30-year auctions, and last month’s poor 2-year auction.

- Back in December, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance rose by around Y100bn today. Reuters also noted that there was no changes to the planned issuance for 10-40-year tenors.

- Overall, with an outright yield and the 2s/5s curve near cycle highs, today’s outcome points to generally poor demand conditions.

- In the aftermath, the 5-year sector is slightly cheaper in afternoon trading.

JGBS AUCTION: 5-Year JGB Auction Results

The Japanese Ministry Of Finance (MoF) sells Y1,928.0bn 5-Year JGBs:

- Average Yield (%): 1.639 (prev. 1.435)

- Average Price: 99.82 (prev. 99.84)

- High Yield (%): 1.650 (prev. 1.444)

- Low price: 99.77 (prev. 99.80)

- % Allotted At High Yield (%): 0.4826 (prev. 37.7565)

- Bid/Cover: 3.0811x (prev. 3.1676x)

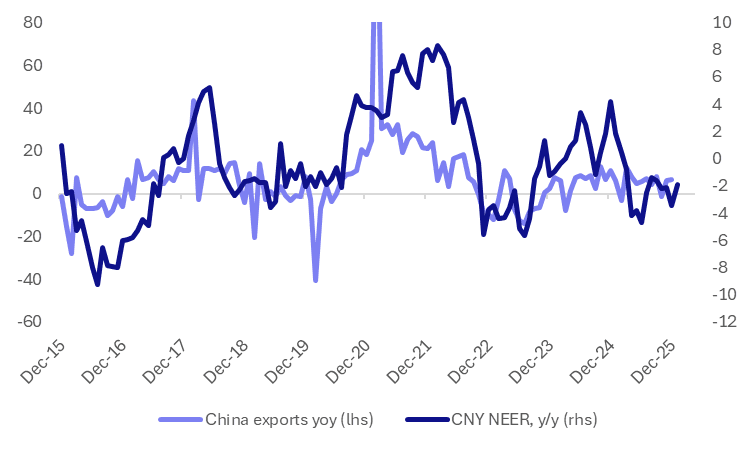

CNY: Scope For More Outperformance Before It Threatens Export Outlook

Export growth was better than forecast at +6.6%y/y, remaining positive for much of 2025 and a bright spot in terms of broader growth drivers. More broadly, the trade outlook for 2026 faces uncertainty in terms of broader economic relations, along with external demand. The yuan has been outperforming against its trading peer in basket terms. Most prominent in recent dealings has been the break higher in CNY/JPY to above 22.80 (fresh highs sicne the 1990s). Still, current CNY CFETS basket tracker levels, 98.76, are sub Jan 2025 levels (100.7). So we arguably need to see more sustained CNY outperformance before it threatens the export outlook.

- The chart below plots the CNY CFETS basket tracker in y/y terms, against China export growth. There has been period over the past decade where the basket gains have coincided with periods of weaker or declining export growth momentum. However, these are often at y/y rates notably higher than those currently prevailing.

- If current basket levels hold then we will be back in positive y/y territory by April. The basket is around 3.9% higher than July lows from last year as well.

- Still, it is difficult to make the case that CNY outperformance will derail export growth currently. On top of this, arguments may also continue to be made of the yuan's cheapness relative to the strength of its external balances.

Fig 1: CNY CFETS Basket Tracker Y/Y & China Export Growth

Source: Bloomberg Finance L.P./MNI