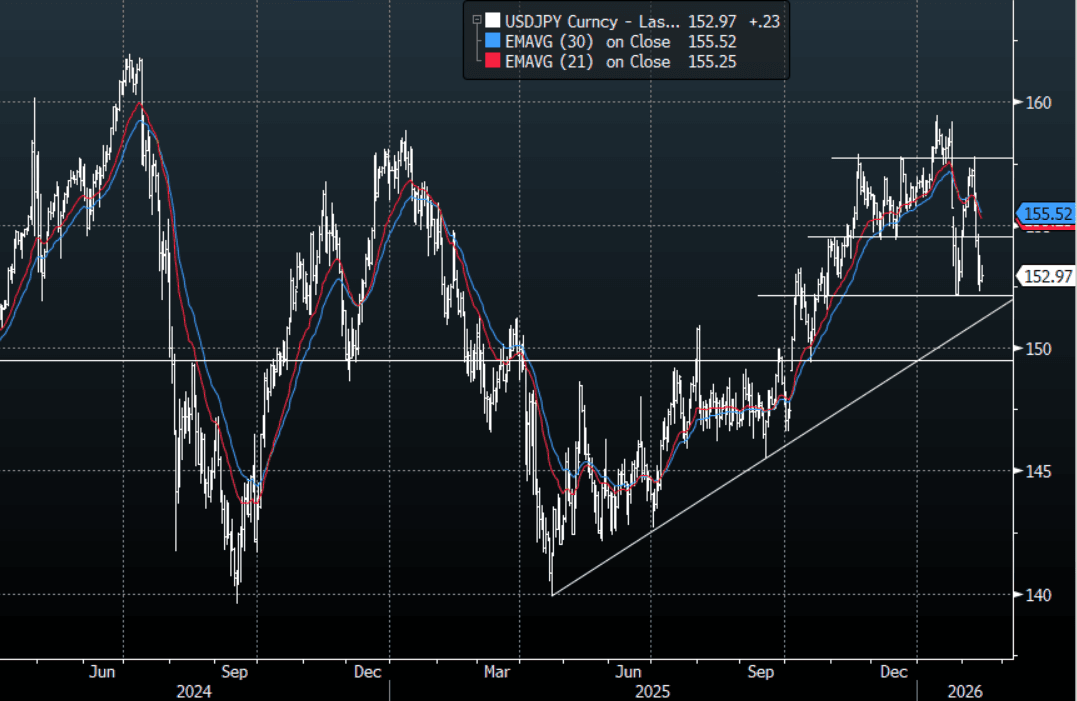

JPY: USD/JPY - Chops Around 153.00 As Longs Continue To Be Pared Back

The USD/JPY range today has been 152.67-153.35 in the Asia-Pac session, it is currently trading around 152.95, -0.15%. USD/JPY continues to be faded on any bounces as risk has turned lower. The headwinds for Yen shorts are growing and squeezing out the leveraged funds. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.25-153.75 and then 154.50-155.00 area as the market pares back its overextended USD longs and looks for another base to form from which to potentially move higher again.

- "BOJ BOARD MEMBER TAMURA: PERSONALLY FEEL JAPAN'S RECENT INFLATION IS BECOMING STICKY, TO KEEP RAISING RATES IF OUTLOOK IS MET” - BBG (tamura sits on the hawkish side)

- "BOJ'S TAMURA: I HAVE SAID NEUTRAL RATE IS AT LEAST AROUND 1%" - BBG

- MNI AU - Honda- BoJ Board Spots Don't Need To Be Filled With Reflationists - Rtrs: Honda states that there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. Via Rtrs: "While acknowledging the chance of another rate hike this year, Honda said the BOJ will likely avoid raising rates in March as it needs to scrutinise the impact of its hike in December.". March BoJ hike odds, per OIS pricing, look a touch lower, but haven't got above 30% in recent sessions

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.00($1.78b). Upcoming Close Strikes : 149.60($869m Feb 17), 151.00($986m Feb 17),156.00($1.87b Feb 17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 161 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 5-Year Supply Shows Lacklustre Demand Metrics

Today’s 5-year JGB auction delivered weakish demand signals. The low price was below expectations at 99.81, the bid-to-cover ratio fell to 3.0811x from 3.1676x, and the tail widened to 0.05 from 0.04.

- The result aligns with the weakish results seen at this month’s 10-year and 30-year auctions, and last month’s poor 2-year auction.

- Back in December, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance rose by around Y100bn today. Reuters also noted that there was no changes to the planned issuance for 10-40-year tenors.

- Overall, with an outright yield and the 2s/5s curve near cycle highs, today’s outcome points to generally poor demand conditions.

- In the aftermath, the 5-year sector is slightly cheaper in afternoon trading.

JGBS AUCTION: 5-Year JGB Auction Results

The Japanese Ministry Of Finance (MoF) sells Y1,928.0bn 5-Year JGBs:

- Average Yield (%): 1.639 (prev. 1.435)

- Average Price: 99.82 (prev. 99.84)

- High Yield (%): 1.650 (prev. 1.444)

- Low price: 99.77 (prev. 99.80)

- % Allotted At High Yield (%): 0.4826 (prev. 37.7565)

- Bid/Cover: 3.0811x (prev. 3.1676x)

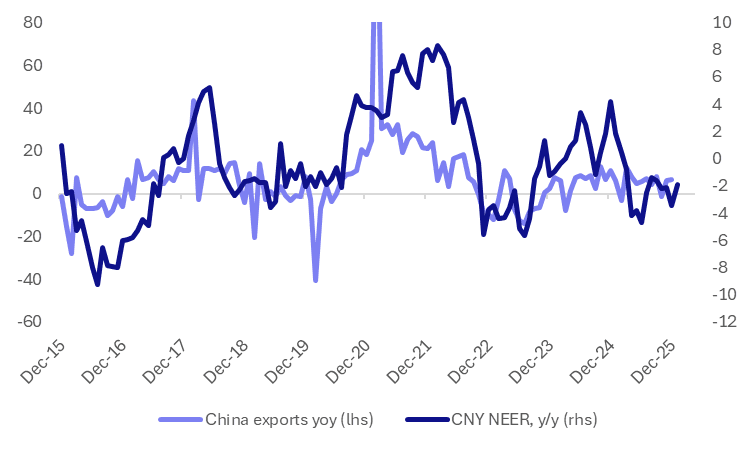

CNY: Scope For More Outperformance Before It Threatens Export Outlook

Export growth was better than forecast at +6.6%y/y, remaining positive for much of 2025 and a bright spot in terms of broader growth drivers. More broadly, the trade outlook for 2026 faces uncertainty in terms of broader economic relations, along with external demand. The yuan has been outperforming against its trading peer in basket terms. Most prominent in recent dealings has been the break higher in CNY/JPY to above 22.80 (fresh highs sicne the 1990s). Still, current CNY CFETS basket tracker levels, 98.76, are sub Jan 2025 levels (100.7). So we arguably need to see more sustained CNY outperformance before it threatens the export outlook.

- The chart below plots the CNY CFETS basket tracker in y/y terms, against China export growth. There has been period over the past decade where the basket gains have coincided with periods of weaker or declining export growth momentum. However, these are often at y/y rates notably higher than those currently prevailing.

- If current basket levels hold then we will be back in positive y/y territory by April. The basket is around 3.9% higher than July lows from last year as well.

- Still, it is difficult to make the case that CNY outperformance will derail export growth currently. On top of this, arguments may also continue to be made of the yuan's cheapness relative to the strength of its external balances.

Fig 1: CNY CFETS Basket Tracker Y/Y & China Export Growth

Source: Bloomberg Finance L.P./MNI