CHINA: CGB10-YR Below 1.8%; Expectations for RRR Cut Post LNY

- China's bond futures are lower Friday, but set to finish the week higher ahead of the lunar new year holiday.

- This week the PBOC has injected considerable liquidity with over CNY1tn via the daily OMO and today through the sale of CNY 1tn 6-month o/r reverse repo.

- CGB 10-Yr ended the week last week at 1.81% and with forecasts for significant liquidity injections proving correct, looks set to consolidate below 1.80% for the first time since November. The CGB 10-Yr is currently at 1.785%

- The 10-Yr bond future is down -.21 today at 108.47, flat for the for the week.

- The 2-Yr bond future is down -.01 today at 102.49 and up +.02 for the week.

- Onshore reports suggest that post LNY markets could see a RRR cut. Consensus being for a 50bps reduction to 8.50% and the release of CNY1tn of liquidity.

- The release of capital would help facilitate further bank lending and support bond yields as issuance plans ramp up for the government in March.

This could see the range for the 10-Yr reset down to 1.70 -1.80%, having been in the 1.80 -1.90% range since November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

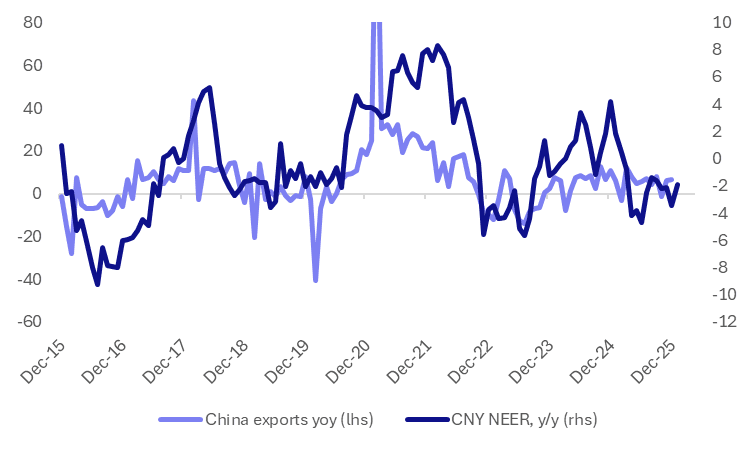

CNY: Scope For More Outperformance Before It Threatens Export Outlook

Export growth was better than forecast at +6.6%y/y, remaining positive for much of 2025 and a bright spot in terms of broader growth drivers. More broadly, the trade outlook for 2026 faces uncertainty in terms of broader economic relations, along with external demand. The yuan has been outperforming against its trading peer in basket terms. Most prominent in recent dealings has been the break higher in CNY/JPY to above 22.80 (fresh highs sicne the 1990s). Still, current CNY CFETS basket tracker levels, 98.76, are sub Jan 2025 levels (100.7). So we arguably need to see more sustained CNY outperformance before it threatens the export outlook.

- The chart below plots the CNY CFETS basket tracker in y/y terms, against China export growth. There has been period over the past decade where the basket gains have coincided with periods of weaker or declining export growth momentum. However, these are often at y/y rates notably higher than those currently prevailing.

- If current basket levels hold then we will be back in positive y/y territory by April. The basket is around 3.9% higher than July lows from last year as well.

- Still, it is difficult to make the case that CNY outperformance will derail export growth currently. On top of this, arguments may also continue to be made of the yuan's cheapness relative to the strength of its external balances.

Fig 1: CNY CFETS Basket Tracker Y/Y & China Export Growth

Source: Bloomberg Finance L.P./MNI

MNI: CHINA 2025 EXPORTS +6.1% Y/Y IN YUAN TERM: CUSTOMS

- CHINA 2025 EXPORTS +6.1% Y/Y IN YUAN TERM: CUSTOMS

- CHINA 2025 IMPORTS +0.5% Y/Y IN YUAN TERM: CUSTOMS

- CHINA 2025 TRADE SURPLUS +CNY8.51 TRLN: MNI CAL

JGBS AUCTION: Poll: 5-Year JGB Auction

*JAPAN 5Y GOVT BOND AUCTION MAY HAVE 99.81 LOWEST PRICE:POLL – BLOOMBERG