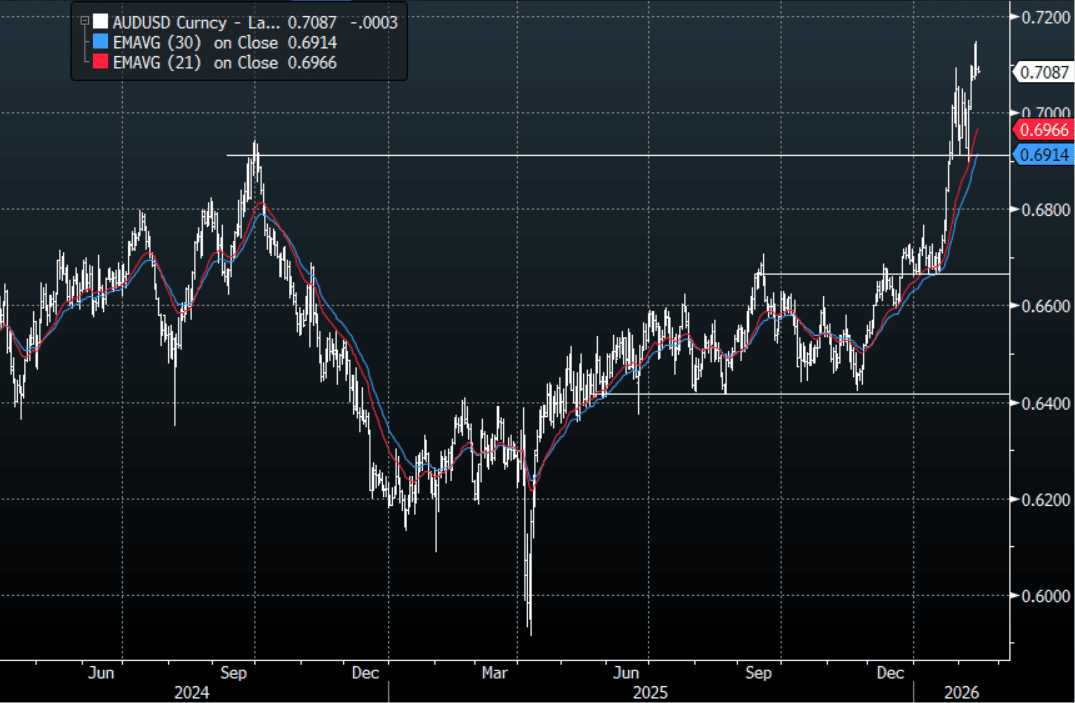

AUD: AUD/USD - Drifts Below 0.7100 As Risk Wobbles Into US CPI

The AUD/USD has had a range today of 0.7081 - 0.7097 in the Asia- Pac session, it is currently trading around 0.7088. The AUD move higher finally stalled toward 0.7150 as we had a “traditional risk-off” session in New York as stocks got sold, treasuries bought and the USD drifted higher. The AUD fell back below 0.7100 pretty easily and the bulls will be hoping for risk to firm up as they will be vulnerable if it builds into anything more than a pullback. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward 0.7035–0.7065, a break below here could signal a deeper pullback as the 0.7100-0.7200 continues to cap the move higher. The US CPI tonight will be closely watched and could add to the headwinds already building for risk.

- Bloomberg - “Australians’ Spending Set to Slow as Rate Hikes Bite, CBA Warns. “While consumers have continued to spend, higher interest rates and easing income growth are likely to slow that momentum as the year progresses,” CBA said in the report.”

- MNI BRIEF: Miran Says Fed Is Biggest Risk To U.S. Growth. "I think it's us," Miran said in Q&A at a Dallas Fed event, when asked about the biggest risk to growth. "The biggest risk I think to the economy is that we're misconstruing just how tight monetary policy is."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6800(AUD1.55b), 0.6825(AUD791m). Upcoming Close Strikes : 0.6980(AUD644m Feb 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 78 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 5-Year Supply Shows Lacklustre Demand Metrics

Today’s 5-year JGB auction delivered weakish demand signals. The low price was below expectations at 99.81, the bid-to-cover ratio fell to 3.0811x from 3.1676x, and the tail widened to 0.05 from 0.04.

- The result aligns with the weakish results seen at this month’s 10-year and 30-year auctions, and last month’s poor 2-year auction.

- Back in December, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance rose by around Y100bn today. Reuters also noted that there was no changes to the planned issuance for 10-40-year tenors.

- Overall, with an outright yield and the 2s/5s curve near cycle highs, today’s outcome points to generally poor demand conditions.

- In the aftermath, the 5-year sector is slightly cheaper in afternoon trading.

JGBS AUCTION: 5-Year JGB Auction Results

The Japanese Ministry Of Finance (MoF) sells Y1,928.0bn 5-Year JGBs:

- Average Yield (%): 1.639 (prev. 1.435)

- Average Price: 99.82 (prev. 99.84)

- High Yield (%): 1.650 (prev. 1.444)

- Low price: 99.77 (prev. 99.80)

- % Allotted At High Yield (%): 0.4826 (prev. 37.7565)

- Bid/Cover: 3.0811x (prev. 3.1676x)

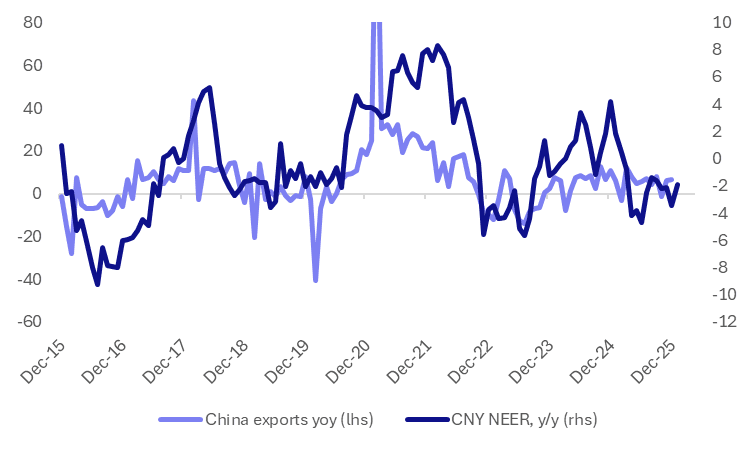

CNY: Scope For More Outperformance Before It Threatens Export Outlook

Export growth was better than forecast at +6.6%y/y, remaining positive for much of 2025 and a bright spot in terms of broader growth drivers. More broadly, the trade outlook for 2026 faces uncertainty in terms of broader economic relations, along with external demand. The yuan has been outperforming against its trading peer in basket terms. Most prominent in recent dealings has been the break higher in CNY/JPY to above 22.80 (fresh highs sicne the 1990s). Still, current CNY CFETS basket tracker levels, 98.76, are sub Jan 2025 levels (100.7). So we arguably need to see more sustained CNY outperformance before it threatens the export outlook.

- The chart below plots the CNY CFETS basket tracker in y/y terms, against China export growth. There has been period over the past decade where the basket gains have coincided with periods of weaker or declining export growth momentum. However, these are often at y/y rates notably higher than those currently prevailing.

- If current basket levels hold then we will be back in positive y/y territory by April. The basket is around 3.9% higher than July lows from last year as well.

- Still, it is difficult to make the case that CNY outperformance will derail export growth currently. On top of this, arguments may also continue to be made of the yuan's cheapness relative to the strength of its external balances.

Fig 1: CNY CFETS Basket Tracker Y/Y & China Export Growth

Source: Bloomberg Finance L.P./MNI