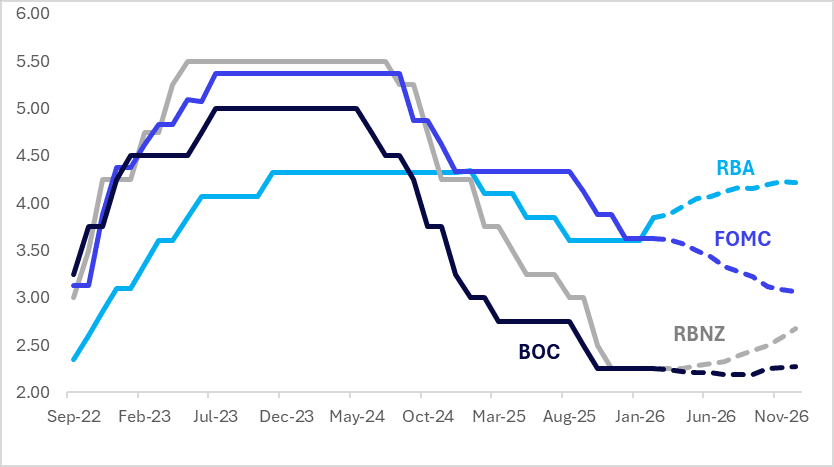

STIR: $-Bloc Pricing Little Changed Over Past Week

Interest-rate expectations across the $-bloc over the past week, looking out to December 2026, have been little changed.

- The key data release across the $-bloc over the past week was Wednesday’s release of Non-Farm Payrolls. Nonfarm payrolls growth was far stronger than expected in January at 130k (cons 65k) after negligible two-month revisions of -17k (mainly in Nov). Private payrolls saw a larger beat, both with the 172k (68k cons) in January but with also a two-month revision of +49k (fairly evenly split over Dec and Nov).

- The Household survey showed a stronger labor market than expected, with the unrounded unemployment rate of 4.283% not just below the consensus of 4.4% and 4.375% prior, but also the lowest since July.

- Today sees the release of January CPI data.

- The next major regional policy event is the RBNZ meetings on 18 February. No tightening is priced for February, while December 2026 assigns 43bps.

- Looking ahead to December 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.07%, -56bps; Canada (BOC): 2.27%, +2bps; Australia (RBA): 4.12%, +27bps; and New Zealand (RBNZ): 2.67%, +42bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

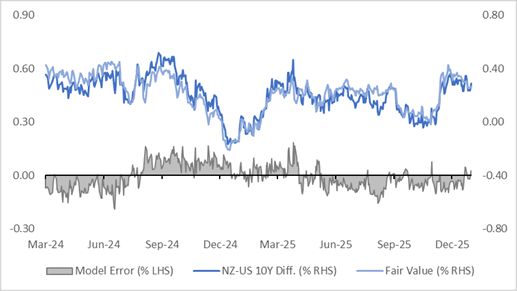

BONDS: NZGBS: NZ-US 10Y Differential In Top Half Two Year Range, But Cheap Vs FV

NZGBs are 2-4bps cheaper today, with the NZ–US 10-year yield differential 4bps wider at +29bps.

- At this level, the differential sits in the top half of the -20bps to +50bps range observed over the past two years. For context, it was around flat ahead of the RBNZ’s November Policy Meeting.

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggests the current differential is about 3bps above its estimated fair value of +26bps.

- The regression’s standard error has been ±15bps over that period, highlighting the inherent variability in the relationship.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

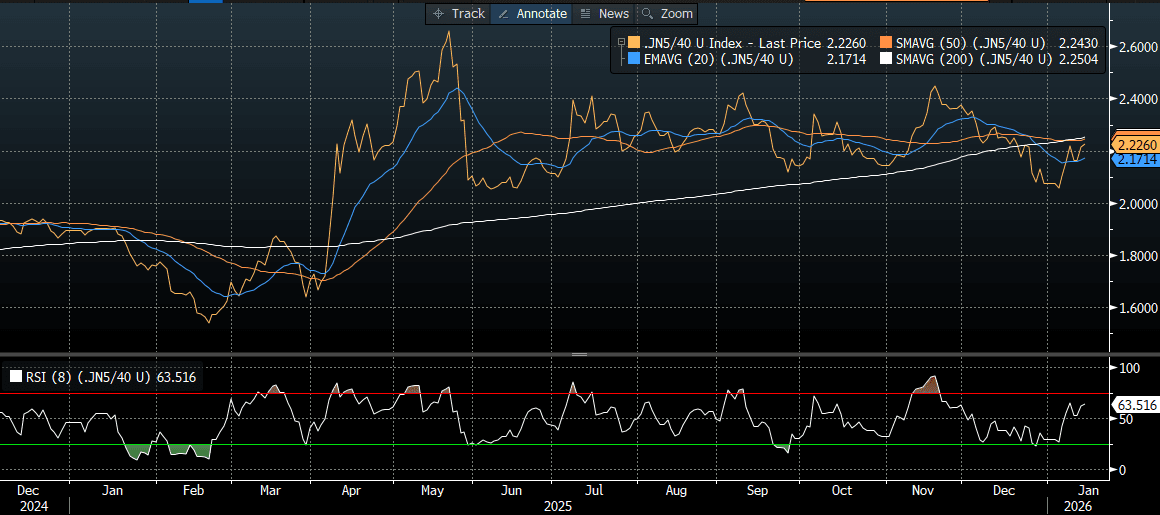

JGBS: Fresh Cycle High For 5YY Ahead Of Today's Supply

In Tokyo morning trade, JGB futures are weaker, -18 compared to settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are flat to 1.5bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.2bp higher at 1.616% versus today’s fresh cycle high of 1.622%.

- (Bloomberg) “Japan’s five-year government bond yield rises to its highest level since the tenor’s debut in 2000, as fiscal concerns deepened on Japanese Prime Minister Sanae Takaichi’s reported plans for a snap election.”

- Today’s moves leave the 5/40 yield curve in the middle of the 205bps to 265bps range it traded in for much of 2025.

- Swap rates are little changed.

Source: Bloomberg Finance LP

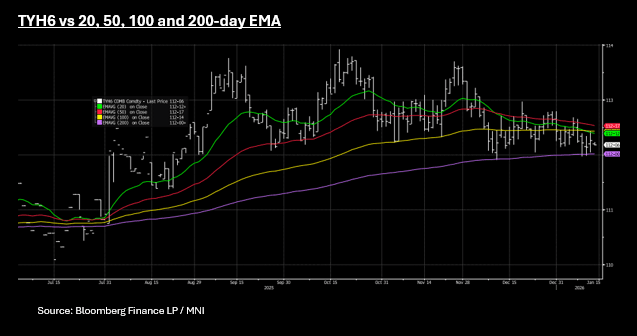

US TSYS: Yields Move Modest, TYH6 Wedged Between Key Tech Levels

US bond futures are modestly lower across all maturities this morning, with the 10-Yr down -02 at 112-06+. The 10-Yr (TYH6) remains near the mid-point of the 100-day EMA at 112-14 and its downside resistance in the 200-day EMA at 112. TYH6 has moved in very narrow range of 111-31+ to 112-14, whilst averaging 112-05+ over the last few days.

Cash is unchanged across most of the curve with just some modest moves higher in yield at the long end.

- The 2-Yr is down -0.4bps at 3.533%

- The 5-Yr is unch at 3.754%

- The 10-Yr is unch at 4.181%

- The 30-Yr is up +0.3bps at 4.841%

The 10-Yr has traded in a very tight range this week of 4.15 - 4.18% which is not atypical ahead of a FED meeting where little is expected.

Of focus tonight will be the Retail Sales Release. Consensus sees a strong rebound in headline retail sales growth in the key holiday shopping month of November, but a pullback in core metrics. Wednesday's report (0830ET) - while well-delayed due to the federal government shutdown - is expected to show 0.5% M/M retail sales growth (0.0% prior), but ex-auto/gas sales slowing slightly to 0.3% (0.5% prior) and the GDP-input Control Group likewise ebbing to 0.4% (0.8% prior).

The issuance schedule tonight sees US$69bn 17-week as the only auction announced at this stage.