JAPAN: Honda- BoJ Board Spots Don't Need To Be Filled With Reflationists - Rtrs

Headlines have crossed from Rtrs after an interview with Etsuro Honda, an economic advisor to Japan PM Takaichi (Honda was also an economic advisor to former Japan PM Abe). Honda states that there is scope for the BoJ to raise rates this year, but the next move is unlikely to come in March. Via Rtrs: "While acknowledging the chance of another rate hike this year, Honda said the BOJ will likely avoid raising rates in March as it needs to scrutinise the impact of its hike in December." Yen may have seen some negative spill over on this headline. USD/JPY is back to 153.30, versus earlier lows of 152.67, although broader cross asset also look a little better, with gold, silver and US equity futures all up from earlier lows. March BoJ hike odds, per OIS pricing, look a touch lower, but haven't got above 30% in recent sessions.

- Honda also stated that upcoming BoJ board vacancies don't need to be filled by reflationists, as the country has exited deflation. Via RTrs: ""I don't necessarily think they need to be reflationists who are proposing powerful monetary easing," Honda said, when asked who should be chosen as new BOJ board members."

- Honda added that he thinks Takaichi understands that the economy is in a different phase from the Abe era.

- This is important in the context that Japan officials, including Takaichi, were stating late last year the country hadn't exited deflation. This is likely to reaffirm market viewpoints that the government may not push back on further BoJ policy normalization in 2026.

- Rtrs added: "Sources have told Reuters the government is set to submit to parliament as early as February 25 a nominee to replace Asahi Noguchi, whose term ends on March 31. Another board member, Junko Nakagawa, will also see her term expire at the end of June. Nominees must be approved by both chambers of parliament."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

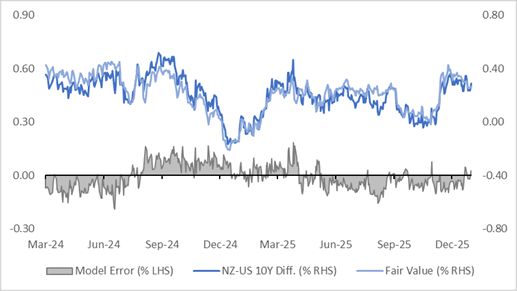

BONDS: NZGBS: NZ-US 10Y Differential In Top Half Two Year Range, But Cheap Vs FV

NZGBs are 2-4bps cheaper today, with the NZ–US 10-year yield differential 4bps wider at +29bps.

- At this level, the differential sits in the top half of the -20bps to +50bps range observed over the past two years. For context, it was around flat ahead of the RBNZ’s November Policy Meeting.

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggests the current differential is about 3bps above its estimated fair value of +26bps.

- The regression’s standard error has been ±15bps over that period, highlighting the inherent variability in the relationship.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

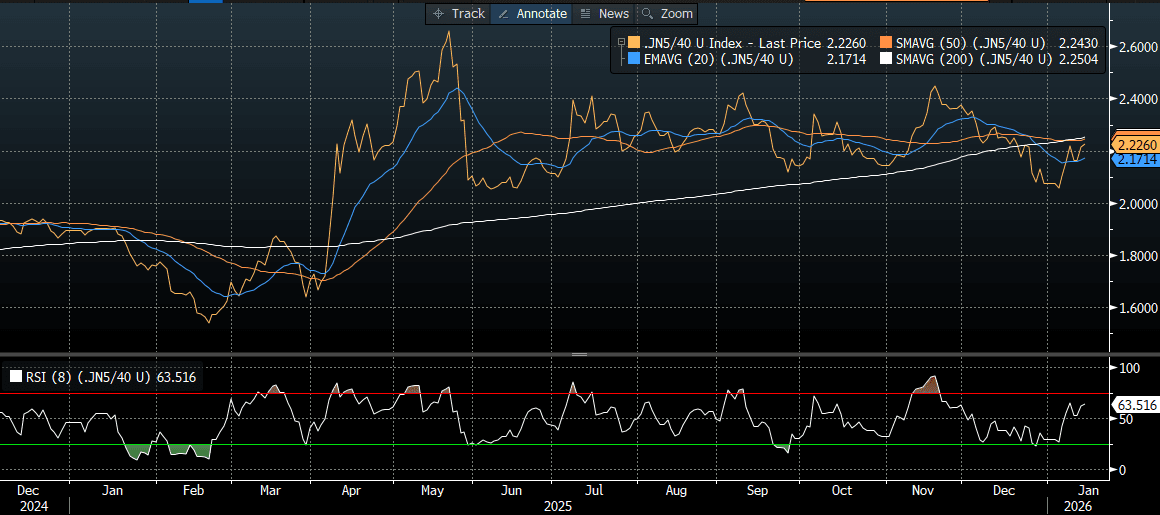

JGBS: Fresh Cycle High For 5YY Ahead Of Today's Supply

In Tokyo morning trade, JGB futures are weaker, -18 compared to settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are flat to 1.5bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.2bp higher at 1.616% versus today’s fresh cycle high of 1.622%.

- (Bloomberg) “Japan’s five-year government bond yield rises to its highest level since the tenor’s debut in 2000, as fiscal concerns deepened on Japanese Prime Minister Sanae Takaichi’s reported plans for a snap election.”

- Today’s moves leave the 5/40 yield curve in the middle of the 205bps to 265bps range it traded in for much of 2025.

- Swap rates are little changed.

Source: Bloomberg Finance LP

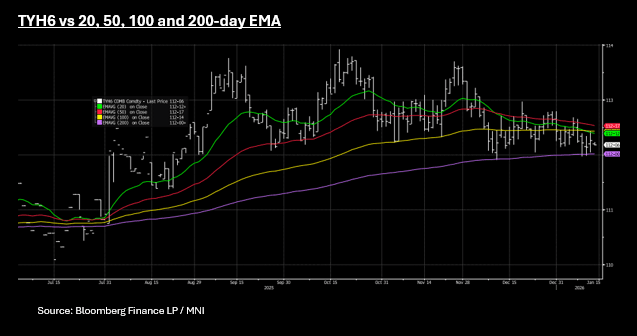

US TSYS: Yields Move Modest, TYH6 Wedged Between Key Tech Levels

US bond futures are modestly lower across all maturities this morning, with the 10-Yr down -02 at 112-06+. The 10-Yr (TYH6) remains near the mid-point of the 100-day EMA at 112-14 and its downside resistance in the 200-day EMA at 112. TYH6 has moved in very narrow range of 111-31+ to 112-14, whilst averaging 112-05+ over the last few days.

Cash is unchanged across most of the curve with just some modest moves higher in yield at the long end.

- The 2-Yr is down -0.4bps at 3.533%

- The 5-Yr is unch at 3.754%

- The 10-Yr is unch at 4.181%

- The 30-Yr is up +0.3bps at 4.841%

The 10-Yr has traded in a very tight range this week of 4.15 - 4.18% which is not atypical ahead of a FED meeting where little is expected.

Of focus tonight will be the Retail Sales Release. Consensus sees a strong rebound in headline retail sales growth in the key holiday shopping month of November, but a pullback in core metrics. Wednesday's report (0830ET) - while well-delayed due to the federal government shutdown - is expected to show 0.5% M/M retail sales growth (0.0% prior), but ex-auto/gas sales slowing slightly to 0.3% (0.5% prior) and the GDP-input Control Group likewise ebbing to 0.4% (0.8% prior).

The issuance schedule tonight sees US$69bn 17-week as the only auction announced at this stage.