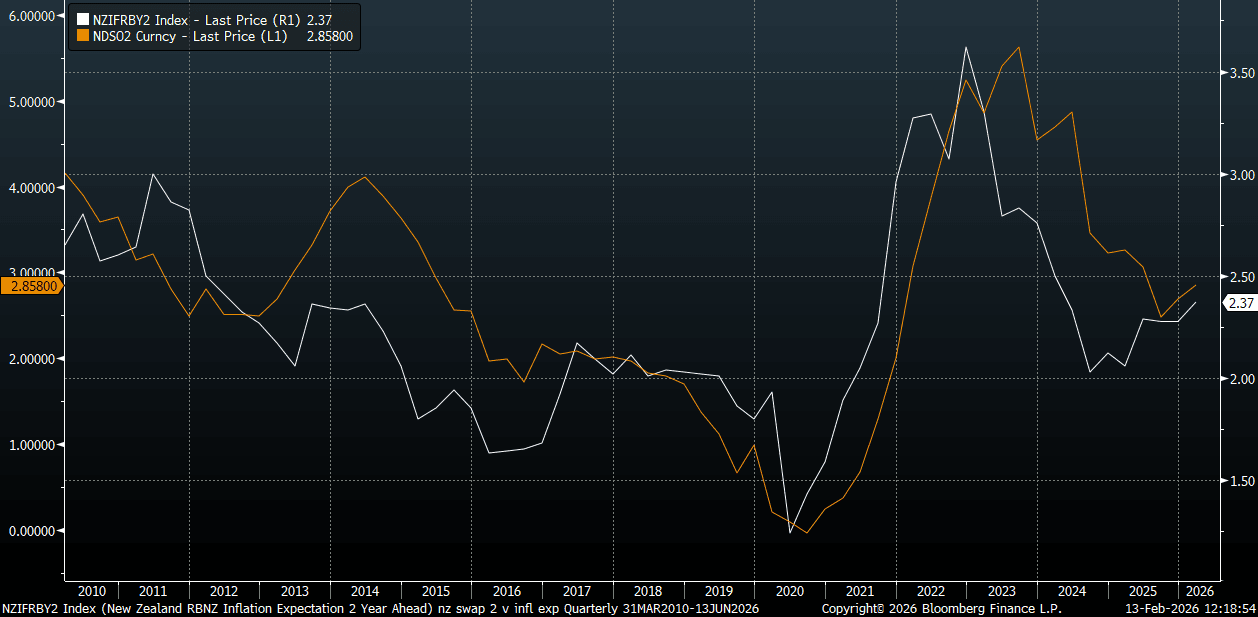

NEW ZEALAND: Inflation Expectations Edge Up But From Low Levels

New Zealand 2yr ahead inflation expectations rose to 2.37% (for the Q1 print) from 2.28% prior. This is highs back to Q1 2024 for the print, but the trend rise has been very modest over this period. The trough in 2yr ahead inflation expectations was near 2.0% in the second half of 2024, and we remain well off end 2022 highs of 3.62%. The chart below plots the 2yr ahead inflation expectations versus the NZ 2yr swap rate (which is the white line). 1yr ahead inflation expectations posted a firmer rise to 2.59% from 2.39%, but likewise remain well off end 2022 highs (just above 5.0%). The data point to an edging up in inflation expectations, but not a pace that is likely to alarm the RBNZ around the need to shift rates higher in the near term (the RBNZ meets next Wed, Feb 18).

- The 5yr and 10yr inflation expectations edged a little higher to around 2.30%. The cash rate expectation was at 2.58% for 1yr ahead, versus 2.31% prior.

Fig 1: NZ 2yr Ahead Inflation Expectations & NZ 2yr Swap Rate

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

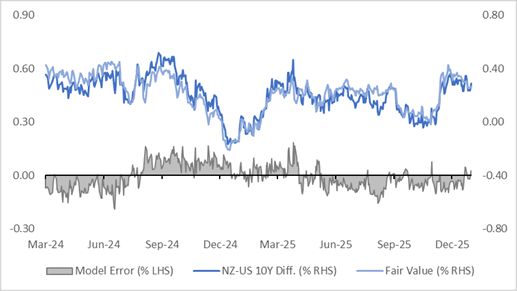

BONDS: NZGBS: NZ-US 10Y Differential In Top Half Two Year Range, But Cheap Vs FV

NZGBs are 2-4bps cheaper today, with the NZ–US 10-year yield differential 4bps wider at +29bps.

- At this level, the differential sits in the top half of the -20bps to +50bps range observed over the past two years. For context, it was around flat ahead of the RBNZ’s November Policy Meeting.

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggests the current differential is about 3bps above its estimated fair value of +26bps.

- The regression’s standard error has been ±15bps over that period, highlighting the inherent variability in the relationship.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

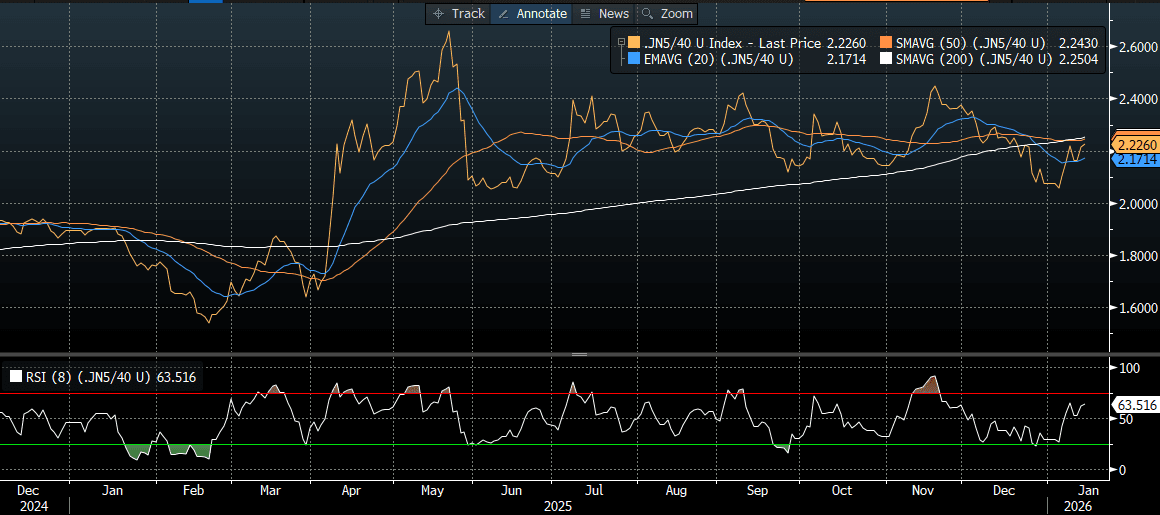

JGBS: Fresh Cycle High For 5YY Ahead Of Today's Supply

In Tokyo morning trade, JGB futures are weaker, -18 compared to settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are flat to 1.5bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.2bp higher at 1.616% versus today’s fresh cycle high of 1.622%.

- (Bloomberg) “Japan’s five-year government bond yield rises to its highest level since the tenor’s debut in 2000, as fiscal concerns deepened on Japanese Prime Minister Sanae Takaichi’s reported plans for a snap election.”

- Today’s moves leave the 5/40 yield curve in the middle of the 205bps to 265bps range it traded in for much of 2025.

- Swap rates are little changed.

Source: Bloomberg Finance LP

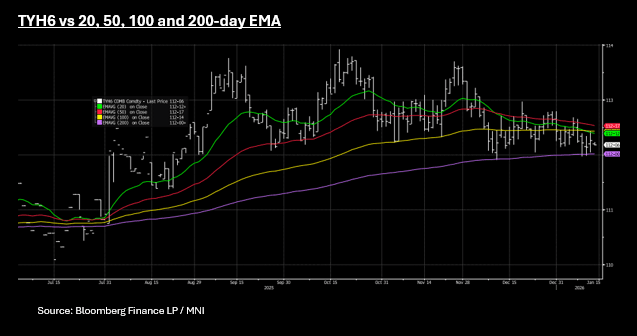

US TSYS: Yields Move Modest, TYH6 Wedged Between Key Tech Levels

US bond futures are modestly lower across all maturities this morning, with the 10-Yr down -02 at 112-06+. The 10-Yr (TYH6) remains near the mid-point of the 100-day EMA at 112-14 and its downside resistance in the 200-day EMA at 112. TYH6 has moved in very narrow range of 111-31+ to 112-14, whilst averaging 112-05+ over the last few days.

Cash is unchanged across most of the curve with just some modest moves higher in yield at the long end.

- The 2-Yr is down -0.4bps at 3.533%

- The 5-Yr is unch at 3.754%

- The 10-Yr is unch at 4.181%

- The 30-Yr is up +0.3bps at 4.841%

The 10-Yr has traded in a very tight range this week of 4.15 - 4.18% which is not atypical ahead of a FED meeting where little is expected.

Of focus tonight will be the Retail Sales Release. Consensus sees a strong rebound in headline retail sales growth in the key holiday shopping month of November, but a pullback in core metrics. Wednesday's report (0830ET) - while well-delayed due to the federal government shutdown - is expected to show 0.5% M/M retail sales growth (0.0% prior), but ex-auto/gas sales slowing slightly to 0.3% (0.5% prior) and the GDP-input Control Group likewise ebbing to 0.4% (0.8% prior).

The issuance schedule tonight sees US$69bn 17-week as the only auction announced at this stage.