US TSYS: Risks Build for Higher CPI

For the bond market, the next filter to assess the future path of interest rates by is Friday's CPI. According to our US team, consensus is for a modest pick up in core prices MoM helped by a typical start of year price reset and normalization of activity since the government shutdown.

Treasuries have shown their willingness to rally with most maturities approaching Friday near to weekly lows in yield, thereby making CPI a critical test.

Cash is weak in Asia today with yields up +1-1.5bps across the curve.

- The 2-Yr is up +1.2bps at 3.47% : lower by -3.1bps for the week.

- The 5-Yr is up +1.2bps at 3.673%: lower by -8.7bps for the week.

- The 10-Yr is up +1.3bps at 4.113%: lower by -8.6bps for the week.

- The 30-Yr is up +1.3bps at 4.749%: lower by -10.2bps for the week.

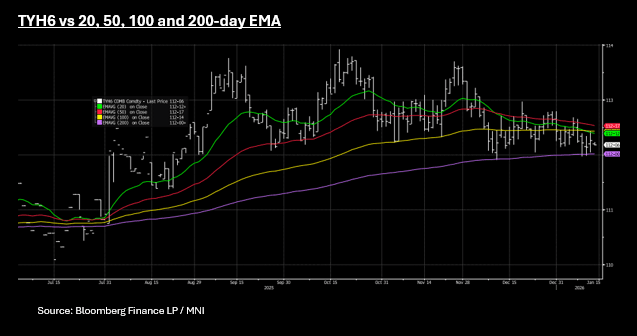

The US 10-Yr future has fallen -01 today to 112-24+ on reasonably high volumes, suggesting good two way flow.

The risks now are to a higher CPI. Yields have moved considerably lower over the week and if our US team are correct and and there is an acceleration in prices, yields could give back much of those gains Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: WED's Data Unlikely to Change Rate Outlook, Yields Grind on Low Volumes

US Treasury futures have been subdued in the Asia trading day as equities remain strong, and key major currencies struggle again. The 10-YR US future is down just -01 at 112-07+ to remain near the mid-point of the 100-day EMA above at 112-14+ and downside resistance from the 200-day EMA at 112-00.

Yield movement in cash saw modest declines out to 10-Yr USTs whilst longer bonds were flat to modestly higher in yields.

- The 2-Yr is down -0.6bps at 3.531%

- The 5-Yr is down -0.5bps at 3.748%

- The 10-Yr is down -0.4bps at 4.177%

- The 30-Yr is up +0.2bps at 4.84%

The 10-Yr has traded in a very tight range this week of 4.15 - 4.18% which is not atypical ahead of a FED meeting where little is expected.

Of focus tonight will be the Retail Sales Release. Consensus sees a strong rebound in headline retail sales growth in the key holiday shopping month of November, but a pullback in core metrics. Wednesday's report (0830ET) - while well-delayed due to the federal government shutdown - is expected to show 0.5% M/M retail sales growth (0.0% prior), but ex-auto/gas sales slowing slightly to 0.3% (0.5% prior) and the GDP-input Control Group likewise ebbing to 0.4% (0.8% prior).

The issuance schedule tonight sees US$69bn 17-week as the only auction announced at this stage

ASIA STOCKS: NKY Reaches New High As NIFTY's Falls Challenge Key Tech Level

As global fund managers look to China equities in 2026, onshore stock exchanges Wednesday said they would raise the minimum margin requirement for new margin financing trades to 100% from 80%, effective January 19, according to official statements from the bourses. Japan's equities rallied again on further expectations for a snap election to bolster her support for a fiscal stimulus. As part of its attempts to broaden its global appeal, the Korea Exchange aims to extend trading hours to 24 hours from Dec. 2027, according to a statement. In what is another strong day for equities across the region, many bourses again posted new record highs.

- The NIKKEI is up +1.18% to a record high of 54,154 and has gained over 5% year to date.

- China's major bourses are all up, seemingly brushing off the margin increase news as the onshore lead the way. Shenzhen is up over 1.4%, whilst the CSI 300 0.7% and the Hang Seng trails, rising by +0.50%.

- Korea's KOSPI is up modestly by +0.30% and continues to lead the way with year to date gains of over 8%.

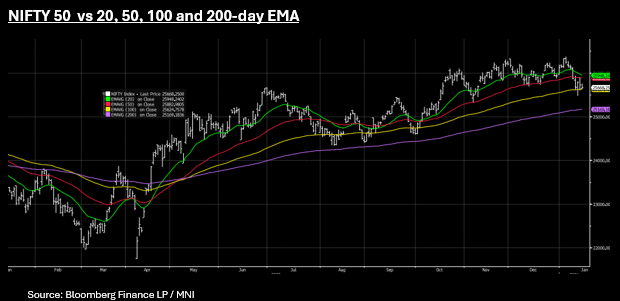

- The NIFTY 50 has fallen for seven out of the last eight trading sessions as it moderates from new all time highs set on January 2, falling over -2.5% since, nearing downside resistance via the 100-day EMA of 25,624.

- SE Asia's bourses are mixed with the FTSE Malay doing little, SE Thai is up +.8% and Jakarta Comp +.90%

JGBS: Slightly Cheaper, BOJ Ueda: Hikes As Economy Improves

JGB futures are holding weaker, -14 compared to settlement levels, after trading in a relatively narrow range in today’s session.

- (Bloomberg) “Japan’s inflation and wages are likely to keep rising moderately after the economy showed resilience last year, according to Bank of Japan Governor Kazuo Ueda. The BOJ will keep raising its benchmark rate in line with the improvement in the economy if its outlook materializes, Ueda says at a New Year conference in Tokyo. An appropriate adjustment of monetary easing will lead to long-term economic growth”

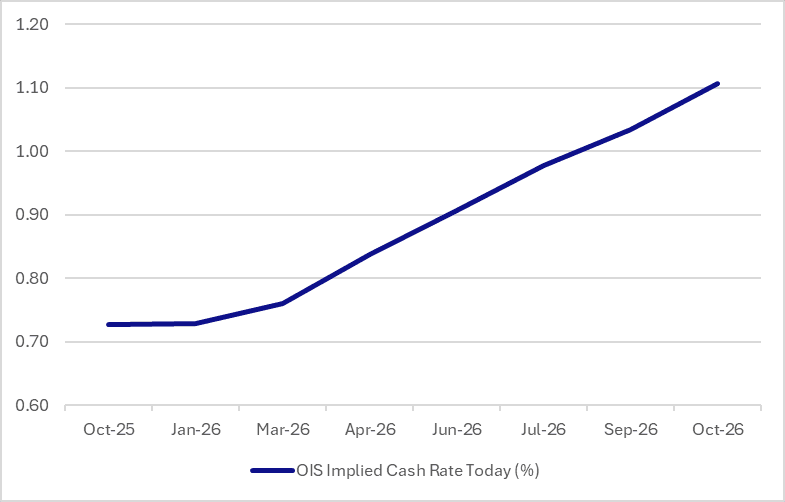

- BOJ-dated OIS assigns a 0% probability to a 25bp hike at the January MPM and around 14% by March 2026, with a full 25bp hike priced in by July.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session.

- Cash JGBs are slightly cheaper across benchmarks. The benchmark 5-year yield is 0.1bp higher at 1.615% versus today’s fresh cycle high of 1.622%.

- Today’s 5-year JGB auction delivered weakish demand signals. The low price was below expectations at 99.81, the bid-to-cover ratio fell to 3.0811x from 3.1676x, and the tail widened to 0.05 from 0.04.

- Swap rates are little changed.

- Tomorrow, the local calendar will see PPI data.

Figure 1: BoJ-Dated OIS – Today

Source: Bloomberg Finance LP / MNI