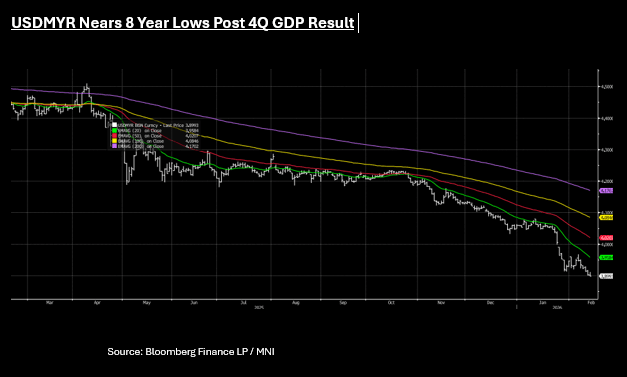

MALAYSIA: GDP Beat Gives Ringgit a Boost

- As the Malaysian growth outlook goes from strength to strength, so to does the Ringgit.

- Against expectations of 4Q expansion of +5.7%, the Malaysian economy grew +6.3% in the 4Q according to today's release. Against a government target for 2026 of 4 - 4.5% the 4Q result could see upward revisions coming.

- Growth was broad-based across major sectors: Manufacturing grew by 6.1% (up from 4.1% in 3Q), driven by electrical and electronic (E&E) products and food processing. Construction maintained double-digit growth at 11.0%, supported by non-residential and specialized construction activities. Services expanded by 6.3%, led by wholesale and retail trade, as well as tourism and agriculture saw a marked improvement to 5.4% due to higher oil palm production.

- Despite moving higher earlier in the day, USDMYR has moved lower post the release by -.0035 to be near 3.8980 / 3.9025 and daily gains for the Ringgit of +.09% and near 8 year lows for the cross.

- The last time USDMYR was sub 3.90 was back in 2018 when GDP expanded +4.7% for the year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Cheaper, Recent Narrowing In AU-US 10Y Diff Reverses

ACGBs (YM -1.0 & XM -2.0) are modestly weaker.

- Job vacancies were down -0.2%q/q (ending in Nov). Job vacancies remain around 30% off 2022 highs, but the trend though was only down modestly, to end Nov just under 327k.

- Cash US tsys are slightly richer, with a steepening bias, in today’s Asia-Pac session.

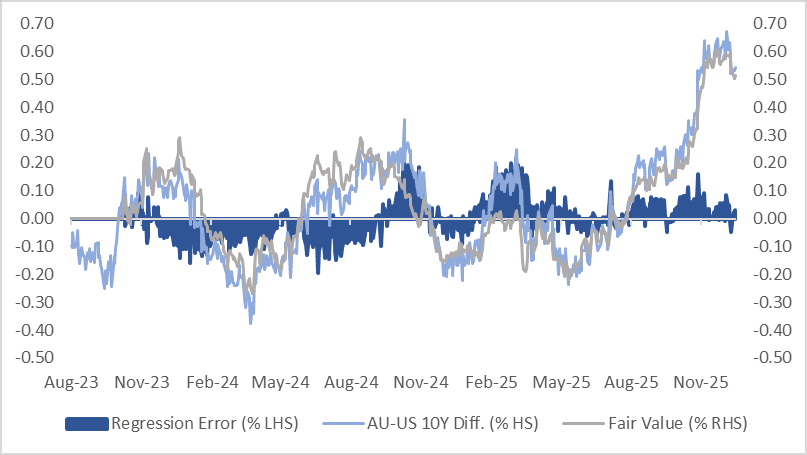

- Cash ACGBs are 1-2bps cheaper with the AU-US 10-year yield differential at at +55bps. A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month (1Y3M) swap spread over the past two years suggests the current spread sits 3bps above its regression-implied fair value.

- Today’s Oct-36 auction result extended the recent trend of firm pricing for ACGBs, with the weighted average yield printing 0.22bps through prevailing mids, according to Yieldbroker. However, demand was weaker, as reflected by a cover ratio of 3.1950x, down from the prior 3.7100x. The AOFM plans to sell A$700mn 3.25% 2029 bond on Friday.

- The bills strip is little changed.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 30% for February to 90% by June and 144% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data.

Bloomberg Finance LP

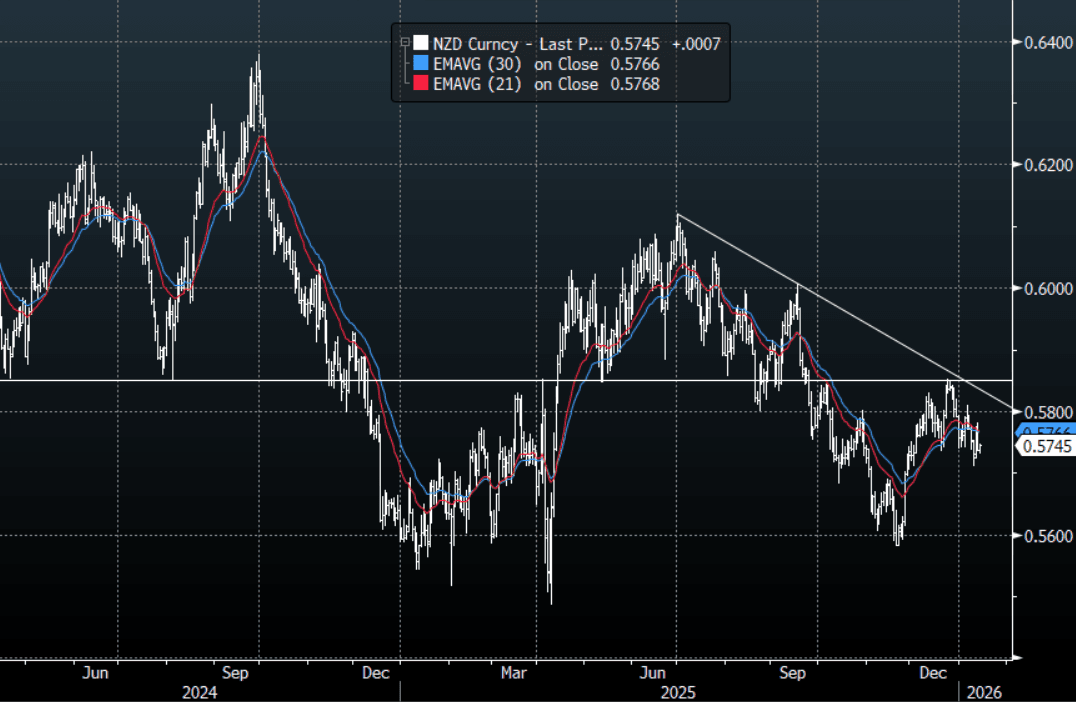

NZD: NZD/USD-Looking To Re-Establish Downward Momentum While Below 0.5800

The NZD/USD had a range today of 0.5731-0.5747 in the Asia-Pac session, it is currently trading around {NZD Curncy}. The NZD has drifted a little higher during our session as Asian stocks, Crypto and Metals outperform. The NZD has put in what looks like a top around 0.5850 and while this continues to cap I suspect the short-term could see bounces initially faded. On the day, the NZD bears will be feeling a little better, looking for sellers again back toward 0.5760-0.5780 as the shorts look for some momentum to build for a retest of the 0.5700 area.

- (Bloomberg) -- New Zealand’s home-building approvals rose 2.8% m/m in November versus a revised 0.7% decline in October, according to Statistics New Zealand.

- MNI AU - Filled Jobs Best M/M Rise Since Late 2023, But Still Down Y/Y: New Zealand filled jobs rose 0.3%m/m in Nov last year after a revised -0.1% outcome for Oct (originally reported as flat). Nov's rise was the best m/m gain since Oct 2023. This signifies some progress in better jobs growth momentum, although it follows a long period of softer momentum through much of 2024 and 2025. In y/y terms, jobs filled were still down 0.4%. The data, along with a rise in building permits, should add to the sense of improved economic momentum for NZ in 2026, suggesting an early wait and see approach for the RBNZ. Note we get Q4 2025 inflation next week on Friday.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5745(NZD349m). Upcoming Close Strikes : 0.5600(NZD351m Jan 16), 0.5800(NZD420m Jan 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Pares Back Early Spike Toward 159.50

The USD/JPY range today has been 159.45 - 159.09 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. USD/JPY popped up trading just short of 159.50 on what looked like strong USD demand into the Japanese Fix, it has spent the rest of the session drifting back to where it started. The BOJ is in a tough spot, and they are going to need to do something significant to turn around the market's perception of a weak Yen. A test of the BOJ/MOF resolve looks inevitable at the moment as the market moves its focus back toward the important 160.00 area. In today's session, first support is back toward 158.50 and then the 157.50-158.00 area as dips continue to be supported. It's almost a case of when not if we get intervention now. In my experience though they tend to come in a lot later than most expect so would not be surprised to see new highs above 162.00 before we start seeing them get involved. Until then it's tough to see what turns this ship around, looks like some decent optionality around 160.00 coming up which might see it chop some wood first.

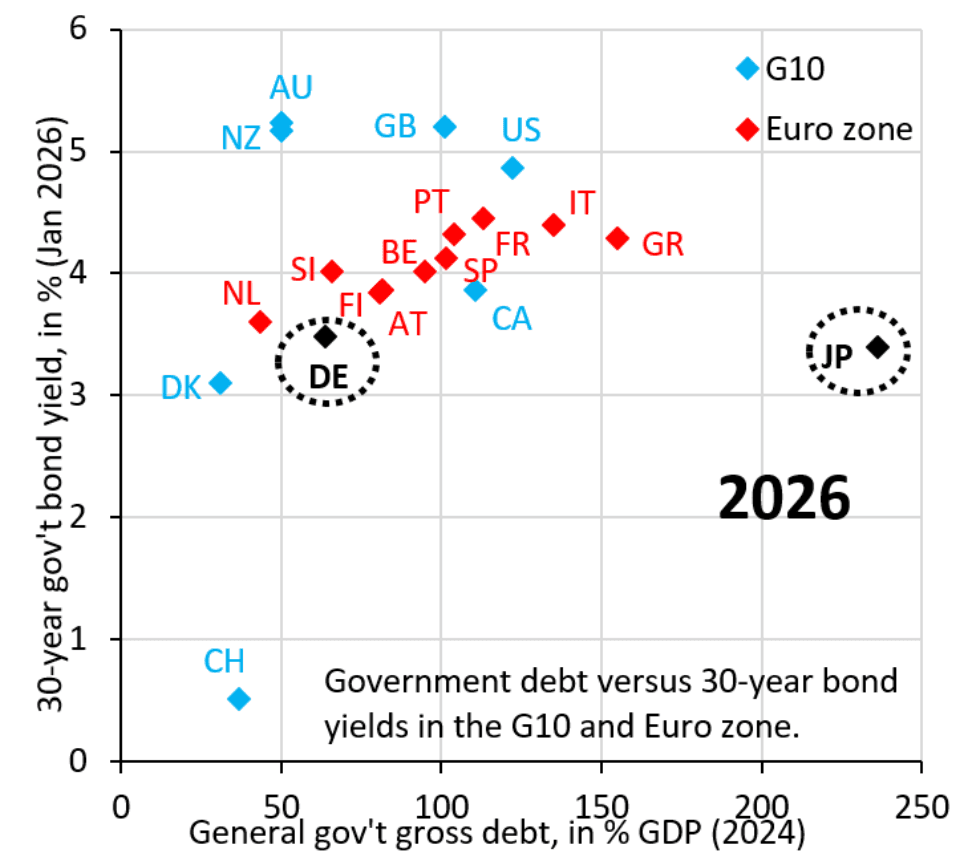

- Robin Brooks on X: “The Yen is falling because Japan's yields are artificially low. Whenever markets think fiscal risk rises, like now with a possible election, the Yen falls. Intervention won't fix this. Instead, the gov't needs to sell assets and retire some of its debt... robinjbrooks.substack.com/p/japan-in-cri “ See Graph Below.

- "Japan is trapped in a very bad place and is the G10 country that's closest to a full-blown debt crisis. Japan's only choice is to accept higher interest rates and a debt crisis or - if it caps yields - a depreciating Yen, which is nearing its 2024 lows."

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 158.00($1.9b Jan 16), 160.00($4.25b Jan 16) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 89 Points

Fig 1 : Gov Debt vs 30-Year Bond Yields

Source: MNI - Market News/@robin_j_brooks