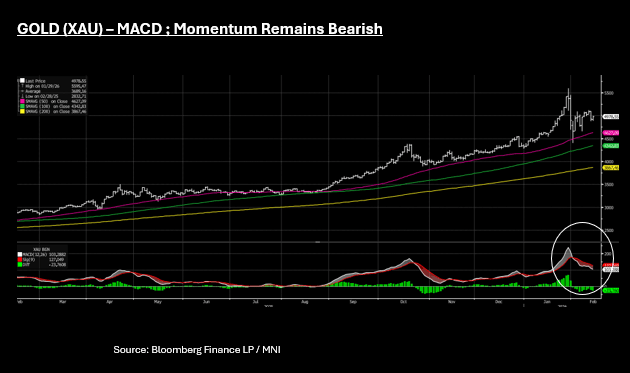

GOLD: Gold Up; Remains Below $5,000 Awaiting US CPI

- During the Asian trading day today gold prices have staged a moderate rebound, climbing +1.2% to US$4,985. This follows a dramatic sell-off on Thursday where the precious metal plunged more than 3%, crashing below the psychologically significant $5,000 per ounce mark to a near one-week low. Market commentators were left scratching their heads as to the driver of Thursday's sell off, with the reality likely that the ripples of the late January falls are still being felt.

- Gold is holding on to weekly gains of just +0.3% as investors wait for the January CPI report in the US later, looking for clues as to the future direction for interest rates. The bullish case for gold in the near term hinges on a weak US CPI bringing rate cuts into play whilst a stronger CPI takes them off the table.

- The current market sentiment remains cautious and likely supported by dip buyers today as bullion holds above the $4,900 support level. Some momentum indicators point a different picture with the MACD (white) line below the Signal (red) line - a bearish sign for prices.

- Geopolitical tensions have taken a backseat in recent days with fresh news from US Iran talks limited with any spike in tensions likely to remain supportive for gold prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Bear-Steepener, Hike Pricing Suggests Flatter Curve

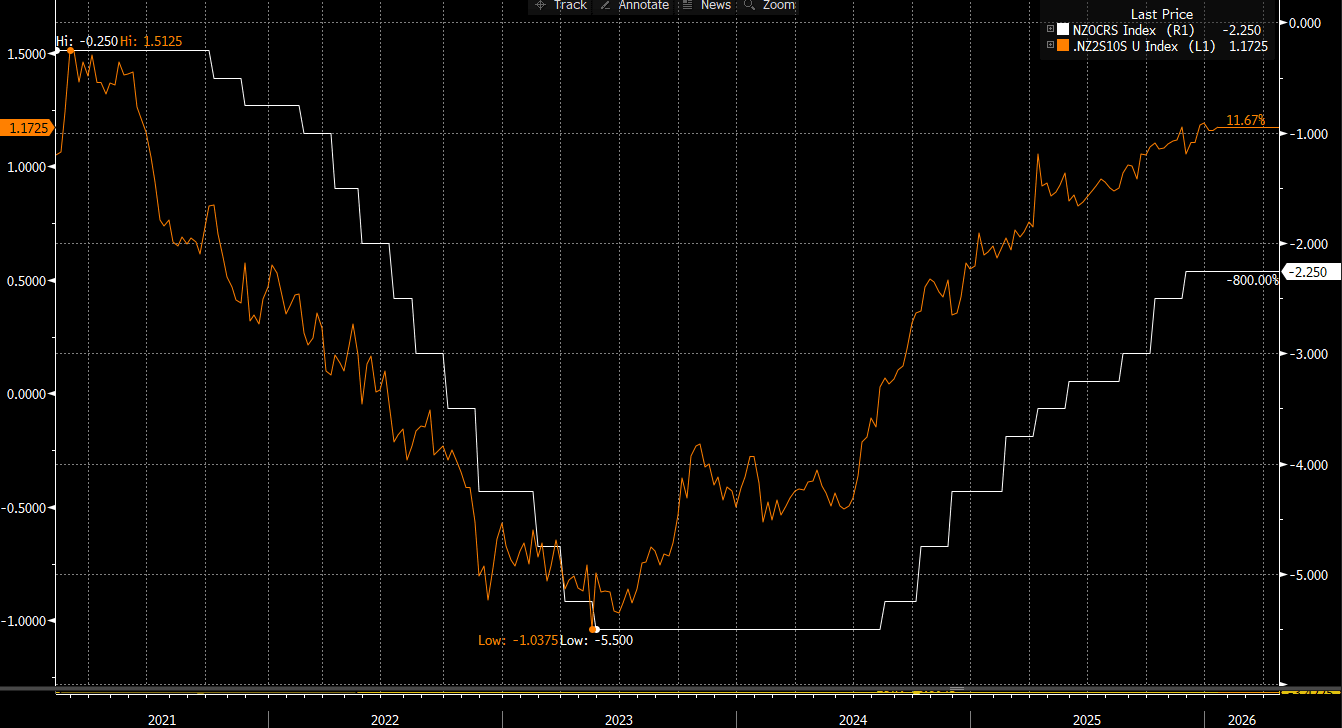

NZGBs closed showing a bear-steepener, with benchmark yields 2-5bps higher.

- NZ filled jobs rose 0.3%m/m in Nov last year after a revised -0.1% outcome for Oct (originally reported as flat). Nov's rise was the best m/m gain since Oct 2023. The data, along with a rise in building permits, should add to the sense of improved economic momentum for NZ in 2026, suggesting an early wait and see approach for the RBNZ. Note we get Q4 2025 inflation next week on Friday.

- Swap rates closed 1–3bps higher, with further steepening in the 2s10s curve. The curve is now near its cycle high and at its steepest since 2021.

- While our Economics team’s central view remains that the RBNZ will stay on hold through 2026, market pricing has recently shifted toward expectations of tightening. Given the current degree of curve steepness, this leaves scope for a material flattening in 2026 should markets continue to price a tightening path (see chart).

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while October 2026 assigns 24bps.

- Tomorrow, the local calendar will be empty.

- Tomorrow, the NZ Treasury plans to sell NZ$250 Million 4.5% 2035 bond, NZ$200 Million 4.5% 2030 bond and NZ$25 Million 3.25% 2050 Linkers.

Bloomberg Finance LP

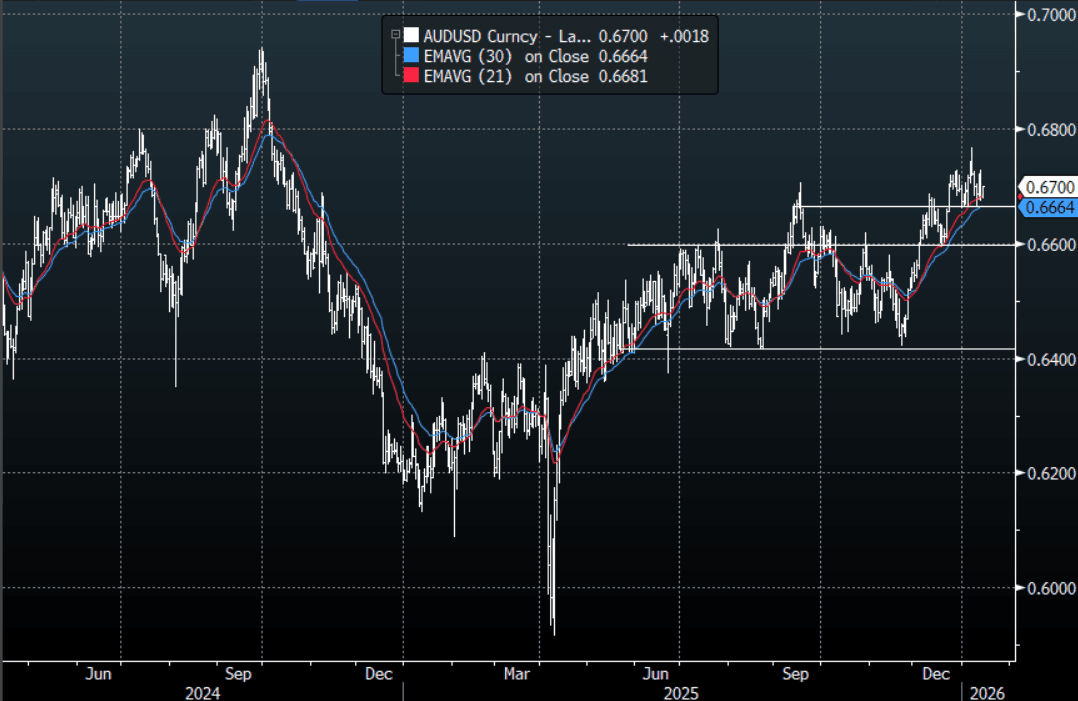

AUD: AUD/USD-Drifts Up To 0.6700, Needs To Hold Below 0.6720-30 To try Lower

The AUD/USD has had a range today of 0.6677 - 0.6700 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD has drifted back toward 0.6700 during our session as Asian stocks, Crypto and Metals outperform. The AUD price action has been constructive but its failure to extend higher would be a little concerning as the USD tries to mount a comeback. Technically while the AUD remains above 0.6600 dips should continue to find support. On the day, the risk is another test of the 0.6650 area which has been so supportive in recent weeks. In the short-term watch for sellers back toward the 0.6700-0.6720 area looking for a test of the 0.6650 support, a sustained move back above 0.6730 and we could see the upward momentum re-established.

- MNI AU: Job Vacancies Ease, Trend Mostly Sideways, Jobs Data Next Thursday: Today's data showed job vacancies down -0.2%q/q (ending in Nov). This follows a -2.7% decline in the prior quarter. Job vacancies remain around 30% off 2022 highs, but the trend though was only down modestly, to end Nov just under 327k. To Nov we were down 5.2%y/y. The q/q trend is relatively steady, not too far from flat for 2025. The data is unlikely to shift RBA thinking around labour market trends. Note we get Dec jobs data next Thursday (22nd of Jan).

- MNI: China To Assess Housing Stimulus On Q1 Performance. Authorities in China are expected to assess the need for substantial property market stimulus after Q1, following recent signals in high-level government reports, although local governments are likely to remain constrained by funding gaps and potential spillover effects on surrounding cities, advisors and analysts told MNI. {NSN T8U2JA33O5C0 <GO>}

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD630m), 0.6700(AUD776m), 0.6750(AUD961m). Upcoming Close Strikes : 0.6600(AUD1.98b Jan16), 0.6640(AUD1.14b Jan16), 0.6800(AUD2.51b Jan16) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 44 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS AUCTION: 5-Year Supply Shows Lacklustre Demand Metrics

Today’s 5-year JGB auction delivered weakish demand signals. The low price was below expectations at 99.81, the bid-to-cover ratio fell to 3.0811x from 3.1676x, and the tail widened to 0.05 from 0.04.

- The result aligns with the weakish results seen at this month’s 10-year and 30-year auctions, and last month’s poor 2-year auction.

- Back in December, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance rose by around Y100bn today. Reuters also noted that there was no changes to the planned issuance for 10-40-year tenors.

- Overall, with an outright yield and the 2s/5s curve near cycle highs, today’s outcome points to generally poor demand conditions.

- In the aftermath, the 5-year sector is slightly cheaper in afternoon trading.