MNI EUROPEAN MARKETS ANALYSIS: China July Exports/Imports Up

- US President Trump announced a 100% tariff on chip imports, although there will be exemptions for companies that already manufacturer chips in the US, or plan to do so. Market impact has seen equities rally where the authorities say key companies will be exempt (like Taiwan).

- China export and import growth was better than forecast for July. NZ inflation expectations were stable, which should aid a cut at the RBNZ meeting later in August.

- Later the Fed’s Bostic speaks on monetary policy. US preliminary Q2 productivity/ULC, July NY Fed 1-yr inflation expectations and jobless claims print as well as June German trade & IP. The BoE decision is announced and a 25bp rate cut is widely expected. Governor Bailey will follow.

MARKETS

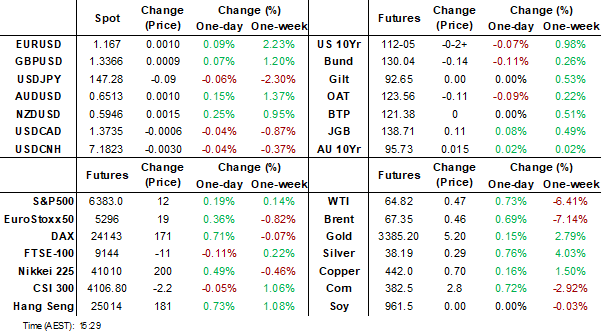

US TSYS: Asia Wrap - Yields Mixed, Long-End Edges Higher

The TYU5 range has been 112-03+ to 112-07 during the Asia-Pacific session. It last changed hands at 112-04, down 0-03+ from the previous close.

- The US 2-year yield is trading around 3.712%.

- The US 10-year yield has edged higher trading around 4.246%, up 0.02 from its close.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Mohamed El-Erian on LinkedIn: “The views of some FOMC members appear to be shifting to align with the position taken by the two dissenters, Governors Bowman and Waller, at last week's policy meeting. The massive revisions to the jobs data are, of course, the catalyst for this change. However, there's another noteworthy aspect: We're once again witnessing the limitations of this Federal Reserve's excessive data dependency, which has left it with virtually no strategic vision -- something that also contributed to the big 2021-22 ("transitory inflation") policy mistake.”

- Alexander Stahel on X: ”Think about this “Black Swan” again. The downward revisions to May and June payrolls in the July jobs report constitute a black swan event — a three-standard-deviation move with less than a 0.2% chance of occurrence in the last 30 years. 50bps cut is coming."

Data/Events: Initial Jobless Claims, Wholesale Inventories, NY Fed 1-Yr Inflation Expectations, Consumer Credit

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bull-Flattener After 30Y Supply, BoJ SoS Tomorrow

JGB futures are stronger, +13 compared to settlement levels.

- Today, the local calendar will also see Leading/Coincident Index data.

- Zerohedge on X: "What epic chaos, Japan had expected items currently tariffed at < 15% would face a 15% levy, while those above 15%, like beef, would stay at the current rate without any additional tariff. But according to the US government, imports from Japan will be subject to an additional 15% tariff regardless of the existing rate: Kyodo."

- Cash US tsys are 1bp cheaper to 1bp richer, with a slight steepening bias, in today's Asia-Pac session.

- Cash JGBs are flat to 4bps across benchmarks, with a flatter curve after today’s 30-year auction.

- The 30-year JGB auction delivered mixed results. The low price aligned with dealer expectations of 95.35, per the Bloomberg survey. However, the cover ratio dipped to 3.4297x from 3.5796x. On the other hand, the auction tail shortened significantly to 0.15 from 0.31, indicating an improvement in bidding strength.

- Swap rates have twist-steepened, with rates 1bp lower to 2bps higher. Swap spreads are mixed.

- Tomorrow, the local calendar will see Household Spending, Trade Balance and Bank Lending data alongside the BOJ Summary of Opinions (July MPM).

JAPAN DATA: Local Investors Sell Offshore Bonds & Stocks

Local investors sold offshore bonds for the second straight week, see the table below. This does fit with some slight easing in global bond returns in recent weeks. Cumulative net buying of offshore bonds has still been very strong in recent months (+¥9.3trln since the start of May). Local investors also sold offshore equities. We have now seen local investors sell offshore stocks in 3 out of the last 5 weeks (with cumulative outflows of nearly ¥1.5trln since late June).

- In terms of inbound inflows into Japan equities/bonds, offshore investors bought local stocks, albeit at a reduced pace. Since the start of April, or the past 18 weeks, we have only seen one week of net selling of local equities by offshore investors.

- On the bond side, we saw the third straight week of outflows, albeit at a fairly modest pace. Offshore investors have sold local bonds in four out of the last five weeks.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Aug 1 | Prior Week |

| Foreign Buying Japan Stocks | 193.0 | 743.3 |

| Foreign Buying Japan Bonds | -87.5 | -184.6 |

| Japan Buying Foreign Bonds | -526.3 | -326.3 |

| Japan Buying Foreign Stocks | -752.1 | 207.3 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Subdued Session Of Trading, Nov-33 Supply Tomorrow

ACGBs (YM +1.0 & XM +1.0) are mildly stronger after a subdued session of trading.

- The June merchandise trade surplus widened more than expected in June to $5365mn from a downwardly-revised $1604mn. There was a jump in exports while imports contracted. The surplus remained in the range it has been in since March 2024.

- After frontloading of shipments to the US in Q1 to beat the early April tariff deadline, exports moderated in Q2 but while they remained at robust levels, the UK exceeded them in June. Iron ore & coal volumes were robust in June.

- Cash US tsys are 1bp cheaper to 1bp richer, with a slight steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at flat.

- The bills strip is slightly mixed, with pricing -1 to +2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 97% probability, with a cumulative 63bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Foreign Reserves data.

- The AOFM plans to sell A$1000mn of the 3.00% 21 November 2033 bond on Friday.

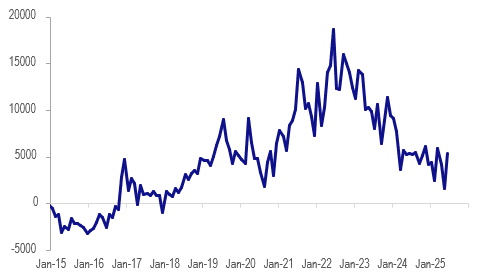

AUSTRALIA DATA: June Gold Exports Drive Increase In Trade Surplus

The June merchandise trade surplus widened more than expected in June to $5365mn from a downwardly-revised $1604mn. There was a jump in exports while imports contracted. The surplus remained in the range it has been in since March 2024.

Australia merchandise trade surplus A$mn

Source: MNI - Market News/ABS

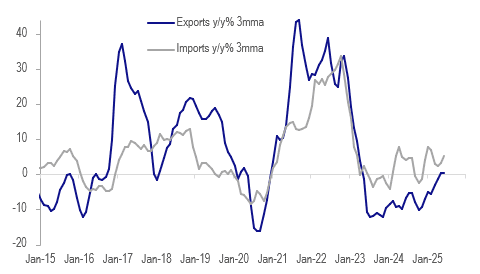

- The 6% m/m rise in goods exports was driven by a 36.7% increase in non-monetary gold but there was also growth in metal ores (+2.3%) and coal (+17.3%). Rural exports fell 0.1% m/m to be up 11.7% y/y while non-rural rose 3.1% but are down 6.3% y/y. Total exports are up 2.6% y/y after declining 2.8% y/y in May.

- Merchandise imports fell 3.1% m/m with the weakness across the major sectors but they are still up 3.1% y/y down from May’s 6.6% though.

- Capex fell 9.1% m/m driven by equipment & other goods to be flat on the year, while consumer items shrank 5.5% m/m due to vehicles but still grew 4.1% y/y. The data are volatile and the 3-month averages suggest some pickup on both components over Q2.

Australia goods exports vs imports y/y% 3-mth ma

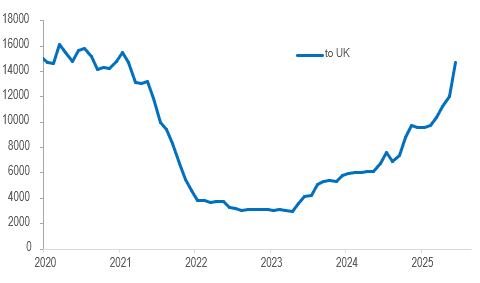

AUSTRALIA DATA: UK Becoming A More Important Export Destination

After frontloading of shipments to the US in Q1 to beat the early April tariff deadline, exports moderated in Q2 but while they remained at robust levels, the UK exceeded them in June. There was an improvement in growth to a number of Australia’s major destinations. Iron ore & coal volumes were robust in June.

- Export growth to the US rose 19.6% y/y in June but the level was surpassed by the UK which saw shipments rise to their highest on record. They have been rising strongly since the Aus-UK FTA came into effect in May 2023 and were over 1000% higher in Q2 than in Q1 2023.

Australia goods exports to the UK A$mn 12-mth sum

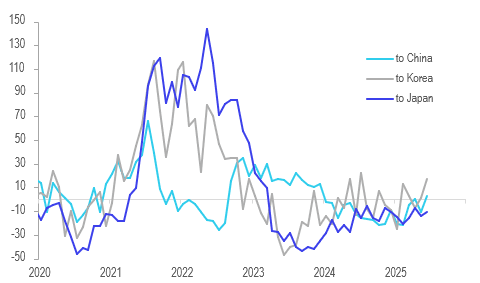

- Exports to China rose in June and annual growth picked up to 2.8% y/y, highest in 18 months. There was an increase in the volumes of iron ore shipments to China.

- There was also higher annual growth to NZ, Korea, India and Indonesia, while it was weak to Japan, Germany, Singapore and Taiwan.

Australia goods exports to Asia y/y%

Source: MNI - Market News/ABS

- Iron ore volumes rose in both May and June driven by China and Japan, while they fell to Korea, Vietnam and Indonesia. Prices fell for the fourth straight month.

- Coal export quantities were up in June driven by Japan, Korea, Taiwan and Europe after hard-coking and semi-soft both rose in May. Unit values also increased on the month.

- LNG saw volumes fall again in June, while prices have decreased in every month this year.

BONDS: NZGBS: Closed On A Strong Note After Q3 Infl Expns Stable

NZGBs closed near session bests, 2-3bps richer, after the release of RBNZ inflation expectations data.

- Q3 inflation expectations were stable in the RBNZ’s survey of forecasters, economists and industry leaders. 1-year ahead they remained at 2.4%, while 2-years ahead at 2.3% - both within the 1-3% target band but remaining above the mid-point. 1-year troughed at 2.1% in Q4 2024 while 2-year in Q3 2024 at 2.0%. With expectations stable, its measure of core moderating 0.1pp to 2.8% in Q2, wage inflation heading towards 2% and economic growth remaining lacklustre, the RBNZ seems likely to cut rates 25bp to 3% on August 20.

- Today’s weekly supply saw strong demand metrics, with cover ratios ranging from 3.13x (May-35) to 6.66x (May-41).

- Cash US tsys are 1bp cheaper to 1bp richer, with a slight steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Swap rates closed 1-2bps lower, with a slightly steeper 2s10s curve.

- RBNZ dated OIS pricing closed little changed across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- Tomorrow, the local calendar will be empty. The next release will be Card Spending data on Wednesday.

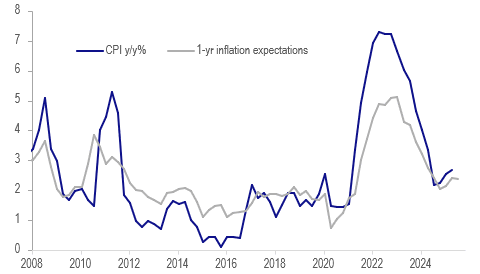

NEW ZEALAND: Steady Inflation Expectations, August Cut Likely

Q3 inflation expectations were stable in the RBNZ’s survey of forecasters, economists and industry leaders. 1-year ahead they remained at 2.4%, while 2-years ahead at 2.3% - both within the 1-3% target band but remaining above the mid-point. 1-year troughed at 2.1% in Q4 2024 while 2-year in Q3 2024 at 2.0%. With expectations stable, its measure of core moderating 0.1pp to 2.8% in Q2, wage inflation heading towards 2% and economic growth remaining lacklustre, the RBNZ seems likely to cut rates 25bp to 3% on August 20.

- Monetary conditions are expected to be less tight at the end of Q3, while they are believed to be easier in Q4 at -22.5 from -7.3. In terms of a year out, they are thought to still be accommodative but less than expected last quarter.

- Q3 household inflation expectations are released on August 14. They tend to be higher than the survey of forecasters results.

NZ inflation vs inflation expectations %

Source: MNI - Market News/LSEG

FOREX: Asia FX Wrap - BBDXY Testing First Support

The BBDXY has had a range of 1203.29 - 1205.45 in the Asia-Pac session, it is currently trading around 1203, -0.10%. The BBDXY is probing its first support just below 1205, with the market still very quick to jump onto any opportunity to sell the USD. A sustained move back above the 1230 area would be needed to put pressure on the bears. China Exports and Imports Beat Estimates for July: the numbers tell a more encouraging story for the longer-term outlook.

- EUR/USD - Asian range 1.1650 - 1.1676, Asia is currently trading 1.1670. The pair has bounced nicely off the important 1.1300/1.1400 area. The market is probing its first resistance towards the 1.1700 area, Sellers should be around this area first-up.

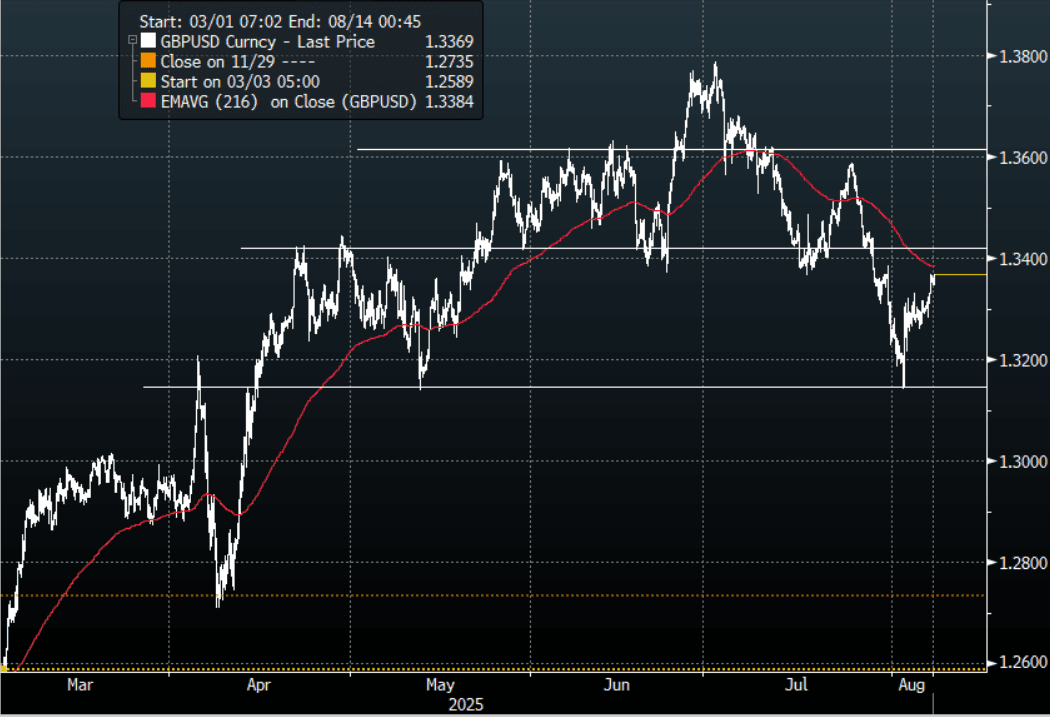

- GBP/USD - Asian range 1.3346 - 1.3369, Asia is currently dealing around 1.3365. The pair bounced nicely off the 1.3100/1.3200 support area. I would suspect sellers could be around this bounce back towards 1.3400/1.3450 initially.

- USD/CNH - Asian range 7.1796 - 7.1875, the USD/CNY fix printed 7.1345, Asia is currently dealing around 7.1830. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.20%, Gold $3380, US 10-Year 4.242%, BBDXY 1203, Crude Oil $64.98

- Data/Events : France Trade Balance/Wages, Germany Industrial Production/Trade Balance, EZ ECB Economic Bulletin

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

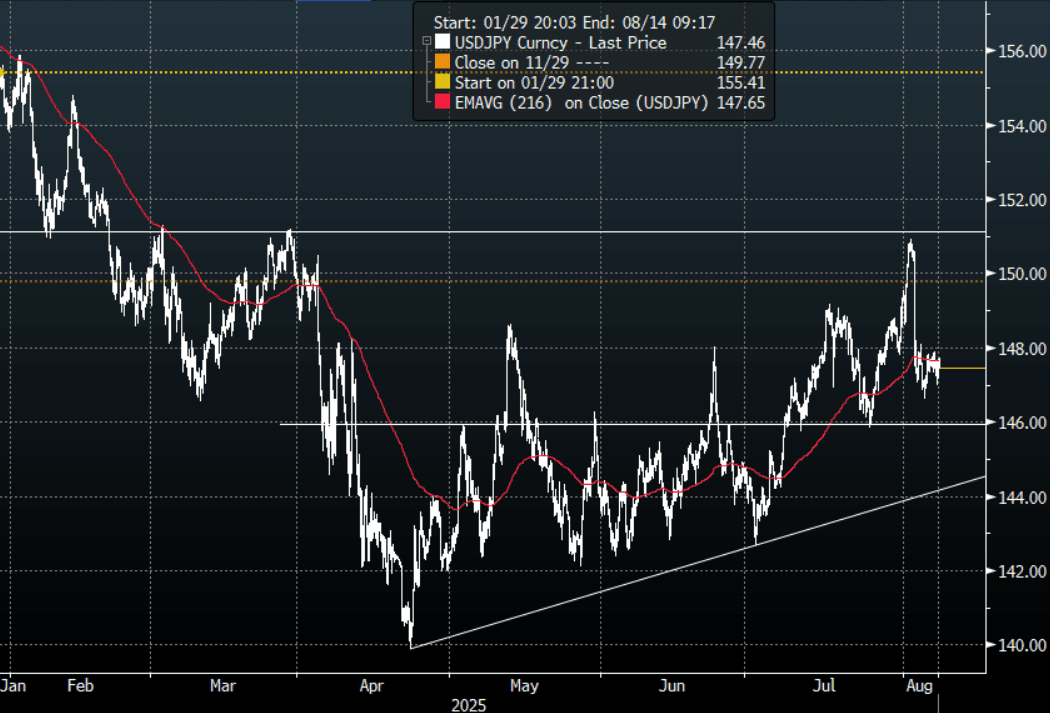

JPY: Asia Wrap - USD/JPY Consolidates On A 147 Handle

The Asia-Pac USD/JPY range has been 147.15 - 147.71, Asia is currently trading around 147.40, +0.03%. USD/JPY is consolidating within a 146.50-148.00 range. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional Yen longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. Price is holding above the support area around 146.50/147.00, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- "U.S. TO ADD 15% TARIFF ON ALL JAPANESE IMPORTS, U.S. WILL NOT APPLY EXCEPTIONS TO JAPAN FOR PRODUCTS THAT ALREADY HAVE TARIFFS EXCEEDING 15% - ASAHI NEWSPAPER CITING WHITE HOUSE OFFICIAL - [RTRS]"

- Zerohedge on X: “What epic chaos, Japan had expected items currently tariffed at < 15% would face a 15% levy, while those above 15%, like beef, would stay at the current rate without any additional tariff. But according to the US government, imports from Japan will be subject to an additional 15% tariff regardless of the existing rate: Kyodo.”

- "HAYASHI: AKAZAWA CALLED ON US TO IMPLEMENT LOWER AUTO TARIFFS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.65($1.43b), 148.50($1.24b).Upcoming Close Strikes : 147.30($797m Aug 12), 146.00($671m Aug 8 ) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

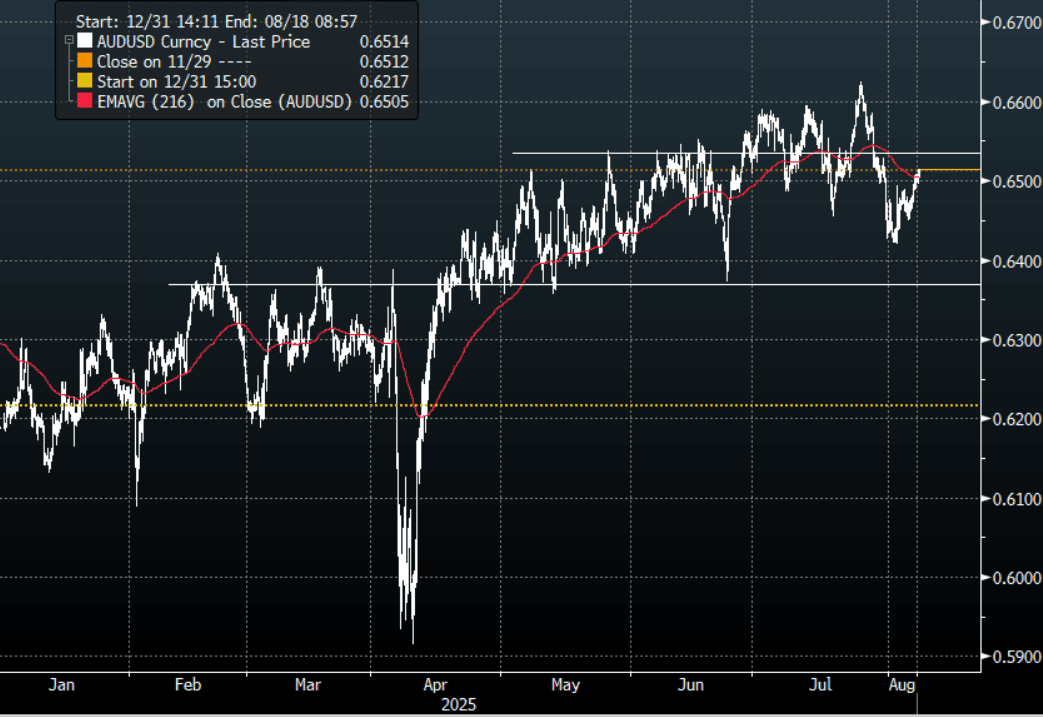

AUD: Asia Wrap - AUD/USD Benefits From Risk Extending Higher

The AUD/USD has had a range of 0.6496 - 0.6516 in the Asia- Pac session, it is currently trading around 0.6515, +0.18%. US equities shrugged off any growth concerns and surged higher, preferring to concentrate on potential rate cuts and further Tech investments. This morning the Apple announcement has seen US futures trade better bid, ESU5 +0.28%, NQU5 +0.30%. The AUD has benefitted from this renewed surge in risk but depending on what your view is 0.6500/50 offers good risk/reward to fade initially. I feel the performance of US equities over August/September will be crucial as seasonality points to some strong headwinds approaching.

- AUSTRALIA DATA: June Gold Exports Drive Increase In Trade Surplus. The June merchandise trade surplus widened more than expected in June to $5365mn from a downwardly-revised $1604mn. There was a jump in exports while imports contracted. The surplus remained in the range it has been in since March 2024.

- (Bloomberg) -- After outperforming peers since April, the best days for the Aussie and kiwi are now in the rearview mirror, Capital Economics says, and expects both currencies to weaken against the US dollar over the remainder of the year. “Although we suspect global risk sentiment will remain strong, we think optimism around China will reverse soon.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD1.2b), 0.6600(AUD1.97b). Upcoming Close Strikes : 0.6500(AUD4.37b Aug 8 ), 0.6400(AUD1.32b Aug 8 ), 0.6700(AUD1.41b Aug 8 ) - BBG

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 95.66 - 96.09, Asia is trading around 96.05. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support toward the 95.00 area. There should be sellers around the 96.00/96.50 area initially, a sustained break below 94.50/95.00 is needed to signal a deeper move lower.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Gets A Boost As Apple Investment Helps Risk Extend Higher

The NZD/USD had a range of 0.5923 - 0.5951 in the Asia-Pac session, going into the London open trading around 0.5950, +0.30%. US equities shrugged off any growth concerns and surged higher, preferring to concentrate on potential rate cuts and further Tech investments. This morning the Apple announcement has seen US futures trade better bid, ESU5 +0.25%, NQU5 +0.30%. NZD/USD bounced nicely off its 0.5850 support but depending on your view I would suspect sellers could return on any bounce back toward 0.6000. For the moment back in the 0.5850-0.6100 range looking for a catalyst to break and give clearer direction.

- Steady Inflation Expectations, August Cut Likely. Q3 inflation expectations were stable in the RBNZ’s survey of forecasters, economists and industry leaders. 1-year ahead they remained at 2.4%, while 2-years ahead at 2.3% - both within the 1-3% target band but remaining above the mid-point. 1-year troughed at 2.1% in Q4 2024 while 2-year in Q3 2024 at 2.0%. With expectations stable, its measure of core moderating 0.1pp to 2.8% in Q2, wage inflation heading towards 2% and economic growth remaining lacklustre, the RBNZ seems likely to cut rates 25bp to 3% on August 20.

- BNZ Notes That Weak Hours Worked Signal Soft Q2 GDP - While the Q2 headline labour market data were not as weak as BNZ expected, the details showed “a picture that is at least as soft as we had feared, and one which is certainly weaker than the Reserve Bank had expected” in May. Thus BNZ is sticking with its view that the RBNZ will cut rates 25bp on August 20 and October 8.

- Westpac Economics - “We expect the RBNZ will deliver another 25bp rate cut at this month’s policy review. But the picture beyond that time is less clear. It’s unlikely that the RBNZ will call time on the easing cycle just yet as the economy is yet to decisively and sustainably turn. However, with mixed economic conditions in recent months, there are questions about the pace and extent of any further policy easing (if any).”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5970(NZD496m). Upcoming Close Strikes : 0.5920(NZD483m Aug 11), 0.5930(NZD646m Aug 11). - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Taiwan Surges On TSMC Chip Tariff Exemption

Asian stocks markets are mostly higher in the first part of Thursday trade. Taiwan markets are the standout, up over 2%. US equity futures are in positive territory, around +0.25-30% for both Eminis and Nasdaq futures. The main news focus has been US President Trump's earlier announcement of a 100% tariff on chip imports from companies that don't have or aren't planning to have manufacturing operations in the US. Those that do have such facilities or are planning to are exempt. Apple shares rose firmly in afterhours US trade as this was seen as a risk to its outlook.

- South Korean and Taiwan officials noted that a number of key suppliers of semiconductors, Samsung and SK Hynix for South Korea and TSMC for Taiwan, would be exempt from the tariffs.

- The has likely aided sentiment in these markets. In Taiwan TSMC is up over 4%. The broader market is up over 2%, leaving the Taiex index around 24000, which is fresh highs back to mid last year. The authorities noted some companies will still be impacted.

- South Korea's Kospi is up around 0.75%, last above 3220. Still, offshore investors have been modest sellers of local stocks so far today.

- Japan markets are also higher, the Topix pressing towards 3000, up close to 0.70%. This is fresh record high for the index.

- In China, markets are little changed. Earlier data showed better than expected export and import growth for July. The trade surplus was sub $100bn, with exports to the US continuing to fall in y/y terms.

- In SEA, the Philippines is weaker down 0.66%. There may be some concern around the chip impact on electronic exports. Elsewhere, Thailand stocks are up over 1% and the SET has now recovered 20% from recent lows. Most other markets are tracking higher.

ASIA STOCKS: Positive Inflow Momentum Slowing Somewhat

Yesterday saw little net aggregate offshore equity inflows for the Asia Pac region. Inflows for South Korea and India were offset by net selling for Taiwan. South Korean net inflows are positive for the past 5 trading days, but still modestly negative for August to date. Headlines have crossed earlier that Samsung and Hynix won't be subject to the 100% chip tariff that US President Trump stated earlier (which will apply to companies which aren't producing or planning to produce chips in the US).

- For Taiwan, yesterday's outflow coincided with the Taiex falling by 0.90%.

- Indian markets saw some positive inflow momentum, but outflows persist August to date.

- In South East Asia, Thailand flows are generally on a positive trend, while Malaysia has mostly seen outflow pressures since the start of the month.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 200 | 193 | -4929 |

| Taiwan (USDmn) | -404 | 1203 | 3059 |

| India (USDmn)* | 178 | -934 | -11220 |

| Indonesia (USDmn) | 27 | -83 | -3755 |

| Thailand (USDmn) | 61 | 164 | -1690 |

| Malaysia (USDmn) | -41 | -188 | -3117 |

| Philippines (USDmn) | 4 | 0 | -628 |

| Total (USDmn) | 24 | 355 | -22279 |

| * Data Up To Aug 5 |

Source: Bloomberg Finance L.P./MNI

OIL: After Falling Through August Crude Is Higher Today As US Punishes India

Oil prices have declined since Friday but so far today they are higher following US President Trump imposing a 25% punitive tariff on imports from India because of its significant imports of fuel from Russia. Markets don’t expect US measures to materially impact Russian exports, but there is still the risk that global supply declines as a result.

- WTI is 1.0% higher at $64.96/bbl after reaching $65.08 but it has struggled to hold breaks above $65. Brent is up 0.8% to $67.45/bbl following an intraday high of $67.58.

- President Trump said that special envoy Witkoff made “great progress” in Russia and that he should meet with President Putin next week. He sounded very uncertain though on the chance of a truce despite his August 8 deadline. He also stated that other countries would face punitive tariffs and didn’t rule out that China would be included.

- Westpac believes that current supply trends will cap moves in Brent in the low $70s (Bloomberg).

- Despite higher output, Saudi Arabia increased its price for the second consecutive month.

- Later the Fed’s Bostic speaks on monetary policy. US preliminary Q2 productivity/ULC, July NY Fed 1-yr inflation expectations and jobless claims print as well as June German trade & IP. The BoE decision is announced and a 25bp rate cut is widely expected. Governor Bailey will follow.

Gold Higher On Increased Fed Cut Expectations & Elevated Uncertainty

After being slightly down on Wednesday, gold prices have started today up 0.3% to $3380.3/oz. They fell to $3365.36, below initial support at $3268.2, early in the APAC session and then rose to a high of $3384.02 supported by the weaker US dollar. Dovish Fed comments yesterday and increased risks to growth from higher tariffs (US added 25% to India for buying Russian fuel, 100% for US chip imports) are likely contributing. Uncertainty remains high over Ukraine-Russia talks.

- The Fed’s Daly and Cook sounded dovish saying that “we will likely need to adjust policy in the coming months” and that payrolls were a possible “turning point” respectively. Markets are also monitoring the replacement process for Governor Kugler.

- Silver is also higher up 0.6% to $38.039, close to the intraday high. It fell to $37.828 earlier. It continues to trade between support at $36.216 and resistance at $39.655.

- Equities are generally stronger with the S&P e-mini up 0.3%, Nikkei +0.7% and Hang Seng +0.5%. Oil prices are up with WTI +0.9% to $64.93/bbl. Copper is 0.3% higher.

- Later the Fed’s Bostic speaks on monetary policy. US preliminary Q2 productivity/ULC, July NY Fed 1-yr inflation expectations and jobless claims print as well as June German trade & IP. The BoE decision is announced and a 25bp rate cut is widely expected. Governor Bailey will follow.

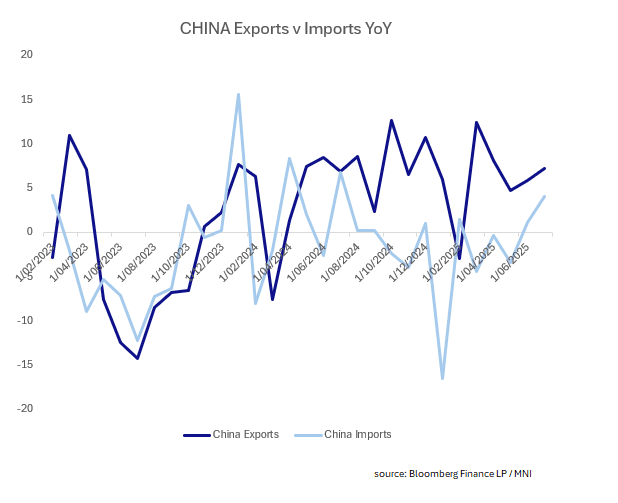

CHINA: Exports and Imports Beat Estimates for July

- The volatility in trade continued in China's July numbers which topped estimates considerably.

- Exports in USD terms were up +7.2% against estimates of +5.6% with June numbers revised up to +5.9%. In CNY terms exports expanded +8.0%, from +7.2% in June.

- After a contraction in February ahead of the imposition of tariffs, China's exports have maintained positive momentum.

- The rise in imports of +4.0% was unexpected as the market forecast for a contraction. The July import release is the strongest since mid-2024.

- The resulting trade balance of $98.24bn missed estimates and was materially down from the month prior.

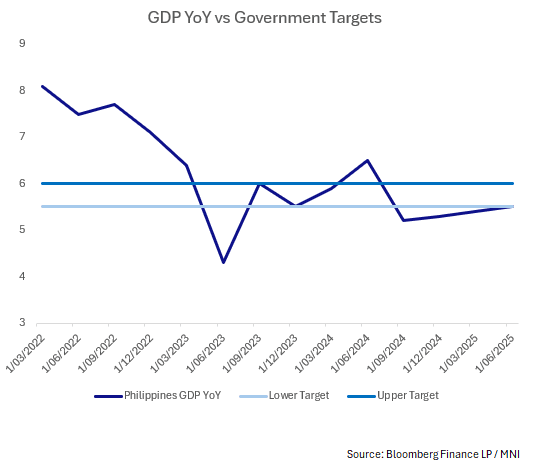

PHILIPPINES: Second Quarter GDP Beats Estimates

- The Philippines’ GDP growth for Q2 grew 5.5% year on year in 2Q25, from 5.4% in the first quarter and ahead of forecasts.

- Domestic consumption has seen mixed signals with imports contracting, overseas cash remittances moderating whilst unemployment has fallen.

- PMI manufacturing bottomed out just prior to the tariff announcements in April, with the accompanying bounce in April and since has seen positive trends emerging. Exports have had one of their strongest six months in several years, underpinning hopes for a pick up in growth.

- The quarter on quarter trend is up also with Q2 rising to +1.5%, from 1.2% in Q1 and topping forecasts of +1.3%.

- The second quarter result still sees growth below the revised government target of 5.5% - 6% (from 6 - 8%) but the improvements will be encouraging. The BSP starting cutting rates ahead of regional peers last year and have reduced the base rate from 6.50% to 5.25%. They next meet on August 28 and have cut at their last two meetings.

INDIA: Country Wrap: Trump Punishes India

- The Monetary Policy Committee on Wednesday decided to press the pause button on its benchmark interest rate and neutral stance as broadly expected, giving a clear signal that the central bank is keeping its powder dry for uncertainties arising out of any tariff threat from the US. The time limit for using the dry powder, however, will be short as the MPC decision came hours before US President Donald Trump’s late evening tariff bombshell of an additional 25% tariff on India for buying Russian oil, after 21 days. Earlier in the day, Reserve Bank of India Governor Sanjay Malhotra said in his monetary policy statement, “The current macroeconomic conditions, outlook and uncertainties call for continuation of the policy repo rate of 5.50% and wait for further transmission of the front-loaded rate cut to the credit markets and the broader economy. Accordingly, the MPC unanimously voted to keep the repo rate unchanged.” (source Financial Express)

- US President Donald Trump, who imposed an additional 25 per cent tariff on India for New Delhi's ties with Russia, has again hinted at imposition of “secondary sanctions”. However, it remains unclear whether Donald Trump has threatened secondary sanctions solely on India or on other countries as well. Donald Trump made the fresh ‘secondary sanction’ threat when he was asked why India was being “singled out” for its business ties with Russia, but not other countries that have been buying Russian energy. (source MINT)

- Unsurprisingly the NIFTY 50 fell at the open on the tariff news and is currently down -0.45% for a third day of losses.

- The Rupee is doing very little in early trade at 87.69 and remains the only of its regional peers posting losses over the last five trading days.

- Bonds are strong with the 10-year -1.5bp in yield at 6.40%

MALAYSIA: Country Wrap: Malaysia Seeks Clarity on CHIPS Tariffs

- Malaysia projects 104 billion ringgit ($24.6 billion) in approved investments for the manufacturing and services sectors in 2025, according to Investment, Trade and Industry Minister. The forecast takes into account the gross domestic product projection, projects under evaluation and potential projects, he said in a parliamentary written reply on Wednesday. The government expects trade performance to experience a slight decline in the second half of 2025 on account of lower demand from the US due to tariffs. A more significant impact is expected to be felt in the first quarter of 2026 (source BBG)

- Malaysia has reached out to the US to seek an explanation on the 100% tariffs President Donald Trump said he would impose on some semiconductor imports, according to Investment, Trade and Industry Minister. The ministry is in regular communication with the US Trade Representative and Department of Commerce, he said in Parliament on Thursday. The tariff would have a big impact on exporting countries such as Malaysia. For now, Malaysia’s semiconductors are exempted from tariffs, but this is subject to review and current policy developments in the US. (source BBG)

- The FTSE Malay KLCI is up +0.24% for a third successive day of modest gains.

- With regional peers delivering strong gains today, the ringgit has struggled and is down -0.01% at 4.2275, yet remains almost 1% better over the last five trading days. The ringgit has traded in a tight range of 4.2365 - 4.2210 in recent days as it looks for a catalyst for it's next move.

- There is a sizeable bond auction today of MYR2.5bn with a 2044 maturity and is the likely source of the move higher for the 10 year yield which is up +2bps at 3.42%

ASIA FX: TWD Outperforms With Local Equities, USD/CNH Down Modestly

In North East Asia FX, the USD has tracked lower, although KRW and TWD have outperformed CNH. TWD has been buoyed by onshore equity market strength, with chip bellwether TSMC exempt from a 100% chip import tariff announced by US President Trump (per the local authorities). USD/HKD remains close to the top end of the peg band, last around 7.8495.

- USD/CNH sits near 7.1820 in latest dealings, down slightly from end NY levels on Wednesday. The USD/CNY fix was set at a fresh low back to early Nov last year. Still, any CNH surge is unlikely to unfold dramatically. The July trade figures were better than forecast, showing firmer export and import trends, particularly on the latter. The trade surplus was slightly below forecasts.

- USD/KRW has drifted a little lower, the pair last near 1383, around 0.25% stronger in won terms versus end Wednesday levels. Local equities are firmer, up a little over 0.60%. The authorities noted that chipmakers Samsung and SK Hynix won't subject to 100% chip tariff threat from US President Trump.

- Spot USD/TWD is down sharply, the pair back to 29.80/85. up around 0.50% in TWD terms. This puts us close to the 50-day EMA support point (29.79). Recent highs in the pair were marked just above 30.03. The better equity tone is helping sentiment in the FX space. The Taiex has surged +2.2% to put the index around the 24000 level. This is fresh highs back to mid 2024. TSMC is up over 4%, after earlier reports stated the tech bellwether would be exempt from the 100% chip tariff announcement made by US President Trump. To the extent this aid fresh inflows into Taiwan stocks it should be a TWD positive.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/08/2025 | 0600/0800 | ** | Trade Balance | |

| 07/08/2025 | 0600/0800 | ** | Industrial Production | |

| 07/08/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/08/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/08/2025 | 0645/0845 | * | Foreign Trade | |

| 07/08/2025 | 0700/0900 | ** | Unemployment | |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 07/08/2025 | 1130/1230 | BOE Press Conference | ||

| 07/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 07/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 07/08/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 07/08/2025 | 1300/1400 | BOE Decision Maker Panel Data BOE Decision Maker Panel Data | ||

| 07/08/2025 | 1400/1000 | * | Ivey PMI | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | ** | Wholesale Trade | |

| 07/08/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 07/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 07/08/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 07/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 07/08/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 07/08/2025 | 1900/1500 | * | Consumer Credit | |

| 07/08/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 08/08/2025 | 2330/0830 | ** | Household spending | |

| 08/08/2025 | 2350/0850 | Balance of Payments | ||

| 08/08/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/08/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 08/08/2025 | 1115/1215 | BOE Pill At National MPC Agency Briefing | ||

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey |