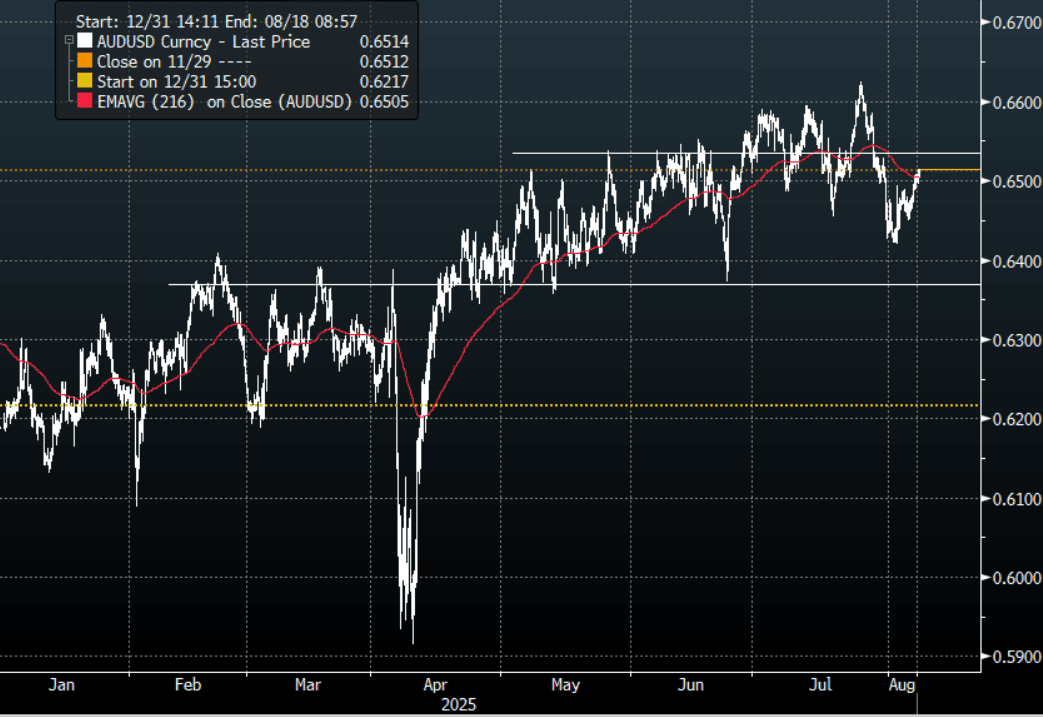

AUD: Asia Wrap - AUD/USD Benefits From Risk Extending Higher

The AUD/USD has had a range of 0.6496 - 0.6516 in the Asia- Pac session, it is currently trading around 0.6515, +0.18%. US equities shrugged off any growth concerns and surged higher, preferring to concentrate on potential rate cuts and further Tech investments. This morning the Apple announcement has seen US futures trade better bid, ESU5 +0.28%, NQU5 +0.30%. The AUD has benefitted from this renewed surge in risk but depending on what your view is 0.6500/50 offers good risk/reward to fade initially. I feel the performance of US equities over August/September will be crucial as seasonality points to some strong headwinds approaching.

- AUSTRALIA DATA: June Gold Exports Drive Increase In Trade Surplus. The June merchandise trade surplus widened more than expected in June to $5365mn from a downwardly-revised $1604mn. There was a jump in exports while imports contracted. The surplus remained in the range it has been in since March 2024.

- (Bloomberg) -- After outperforming peers since April, the best days for the Aussie and kiwi are now in the rearview mirror, Capital Economics says, and expects both currencies to weaken against the US dollar over the remainder of the year. “Although we suspect global risk sentiment will remain strong, we think optimism around China will reverse soon.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD1.2b), 0.6600(AUD1.97b). Upcoming Close Strikes : 0.6500(AUD4.37b Aug 8 ), 0.6400(AUD1.32b Aug 8 ), 0.6700(AUD1.41b Aug 8 ) - BBG

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 95.66 - 96.09, Asia is trading around 96.05. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support toward the 95.00 area. There should be sellers around the 96.00/96.50 area initially, a sustained break below 94.50/95.00 is needed to signal a deeper move lower.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Quiet Session

The TYU5 range has been 110-29+ to 111-01+ during the Asia-Pacific session. It last changed hands at 111-00, up 0-02 from the previous close.

- The US 2-year yield has moved lower trading around 3.884%, down 0.01 from its close.

- The US 10-year yield is relatively unchanged trading around 4.38%.

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- Per Politico: "The United States has offered an agreement to the European Union that would keep a 10 percent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits, an EU diplomat and a national official told POLITICO."

- (Bloomberg) -- “Scott Bessent told CNBC that he’ll meet with his Chinese counterpart within the next couple of weeks.”

- Data/Events: Bond investors will be focusing on the Fed Minutes and the demand for 10 & 30-year maturities this week. NFIB Small Business Optimism tonight

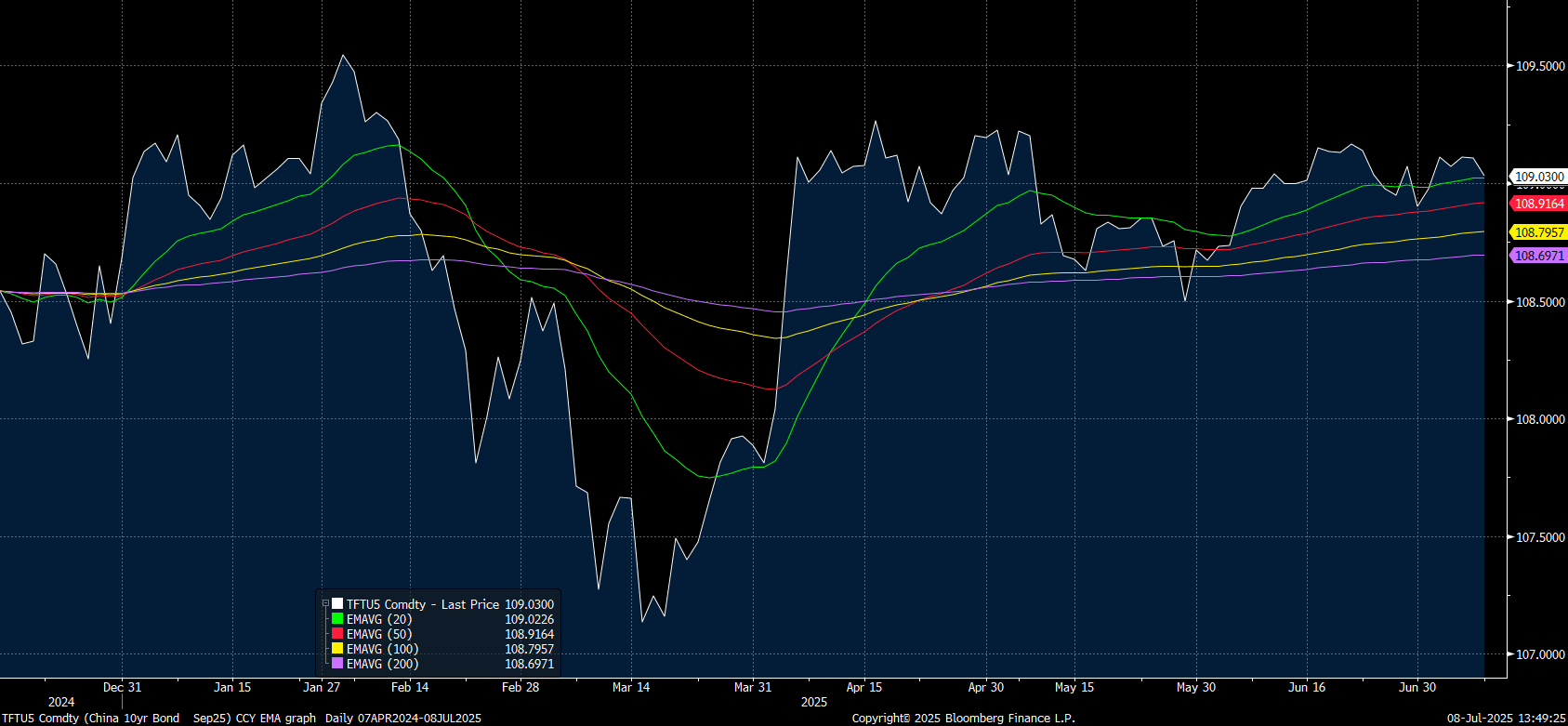

CHINA: Bond Futures Lower as Equities Rally

- China's major bond futures were all lower today in the morning session as equities rallied strongly across major bourses.

- The 10yr is down -0.07 at 109.03 and is approaching the 20-day EMA of 109.02.

source: Bloomberg Finance LP / MNI

- The 2yr bond future is down -0.02 at 102.47 and has moved below the 20-day EMA of 102.49.

- Government bonds are remain stable with the 10yr at 1.64%

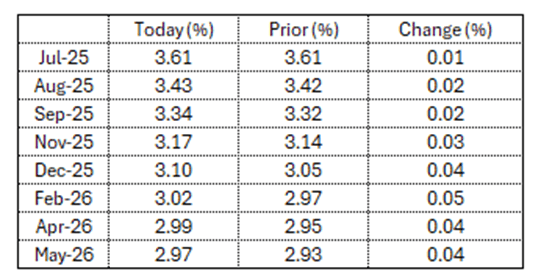

STIR: RBA Dated OIS Firmer Ahead Of RBA Decision

RBA-dated OIS pricing is firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 91% probability, with a cumulative 75bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Figure 1: RBA-Dated OIS – Current Vs. Prior

Source: Bloomberg Finance LP / MNI