ASIA STOCKS: Taiwan Surges On TSMC Chip Tariff Exemption

Asian stocks markets are mostly higher in the first part of Thursday trade. Taiwan markets are the standout, up over 2%. US equity futures are in positive territory, around +0.25-30% for both Eminis and Nasdaq futures. The main news focus has been US President Trump's earlier announcement of a 100% tariff on chip imports from companies that don't have or aren't planning to have manufacturing operations in the US. Those that do have such facilities or are planning to are exempt. Apple shares rose firmly in afterhours US trade as this was seen as a risk to its outlook.

- South Korean and Taiwan officials noted that a number of key suppliers of semiconductors, Samsung and SK Hynix for South Korea and TSMC for Taiwan, would be exempt from the tariffs.

- The has likely aided sentiment in these markets. In Taiwan TSMC is up over 4%. The broader market is up over 2%, leaving the Taiex index around 24000, which is fresh highs back to mid last year. The authorities noted some companies will still be impacted.

- South Korea's Kospi is up around 0.75%, last above 3220. Still, offshore investors have been modest sellers of local stocks so far today.

- Japan markets are also higher, the Topix pressing towards 3000, up close to 0.70%. This is fresh record high for the index.

- In China, markets are little changed. Earlier data showed better than expected export and import growth for July. The trade surplus was sub $100bn, with exports to the US continuing to fall in y/y terms.

- In SEA, the Philippines is weaker down 0.66%. There may be some concern around the chip impact on electronic exports. Elsewhere, Thailand stocks are up over 1% and the SET has now recovered 20% from recent lows. Most other markets are tracking higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

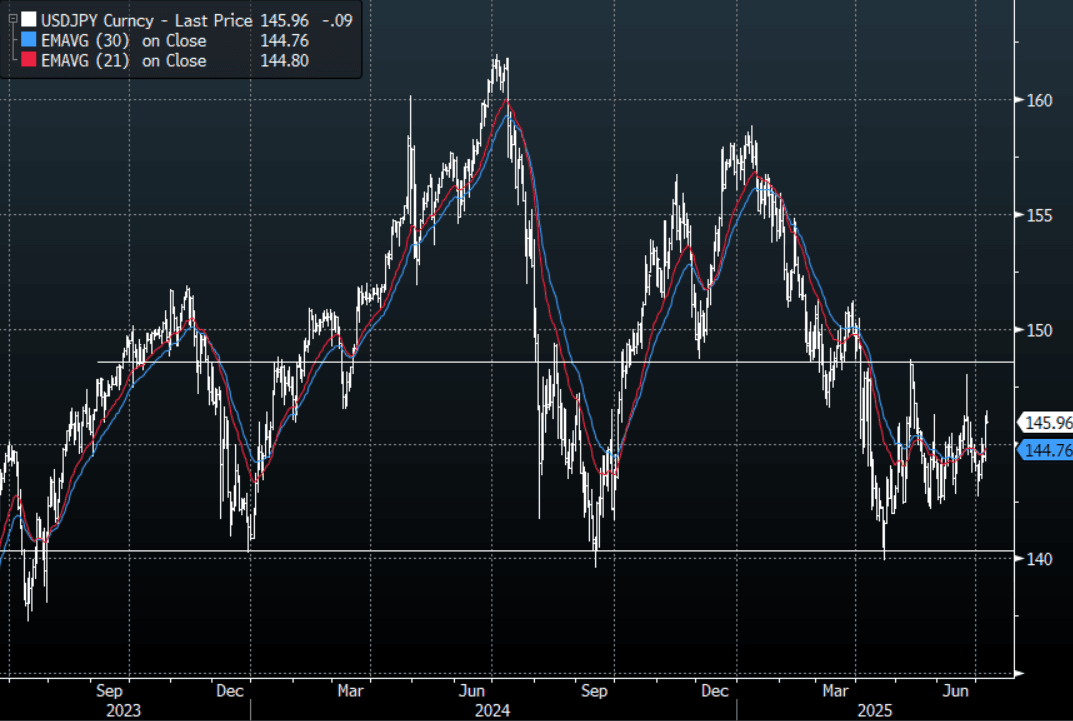

JPY: Asia Wrap - USD/JPY Finds Supply Towards 146.50

The Asia-Pac USD/JPY range has been 145.83 - 146.45, Asia is currently trading around 146.00, +0.05% having found decent supply towards the 146.50 area in our session. USD/JPY price action was telling overnight as it marched relentlessly higher challenging a market positioned the wrong way. Price is still well within the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market.

- (Bloomberg) -- “Japan’s super-long bonds extended their recent declines, pushing the yield on 30-year debt back above 3% and within sight of a record high. The moves come as investors weigh the impact of a new Aug. 1 deadline for US tariffs and as concern mounts that an upper house election in Japan on July 20 will usher in higher government spending.”

- Zerohedge on X: - “Impact of new tariff on Japan (if remains unchanged): JPM strategist Rie Nishihara expects a reciprocal tariff of 24% will lead to 0.4%-0.9% drag in Japan GDP and 7% decline in TOPIX 2025 EPS. The downside scenario estimated by Rie for NKY is 34,000.”

- (Bloomberg) -- Japanese Finance Minister Katsunobu Kato says that he’s not planning to hold talks specifically on currencies with US Treasury Secretary Scott Bessent in the near future.

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to follow through with yesterday's price action the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.60($948m).Upcoming Close Strikes : 144.50($860m July9).

- CFTC data shows Asset managers increased their JPY longs slightly +94753, while leveraged funds maintained their longs they have tried to rebuild +15798.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Stocks Advance on Hope of Further Negotiations

The headlines overnight focused on the imposition of tariffs on Japan and Korea and the sending of letters to other countries. However markets today focused on President Trump's suggestions that he remains open to further negotiations, further delaying tariffs until August. These comments eased earlier concerns .

- China's major bourses were strong with the Hang Seng leading the way with gains of +0.79%, CSI 300 up +0.74%, Shanghai Comp up +0.58% and Shenzhen rising +1.07%

- In Taiwan, the TAIEX was one of the few fallers, down -0.61% today.

- The KOSPI had a slow start to the day but things improved on Trumps comments and it has gained +1.40% to be one of the best performers of the major bourses.

- The FTSE Malay KLCI is down -0.54% and the Jakarta Comp down just -0.05%.

- The FTSE Straits Times in Singapore is up +0.45% and the PSEi in the Philippines down -0.17%

- The NIFTY 50 is doing very little following yesterday finishing flat.

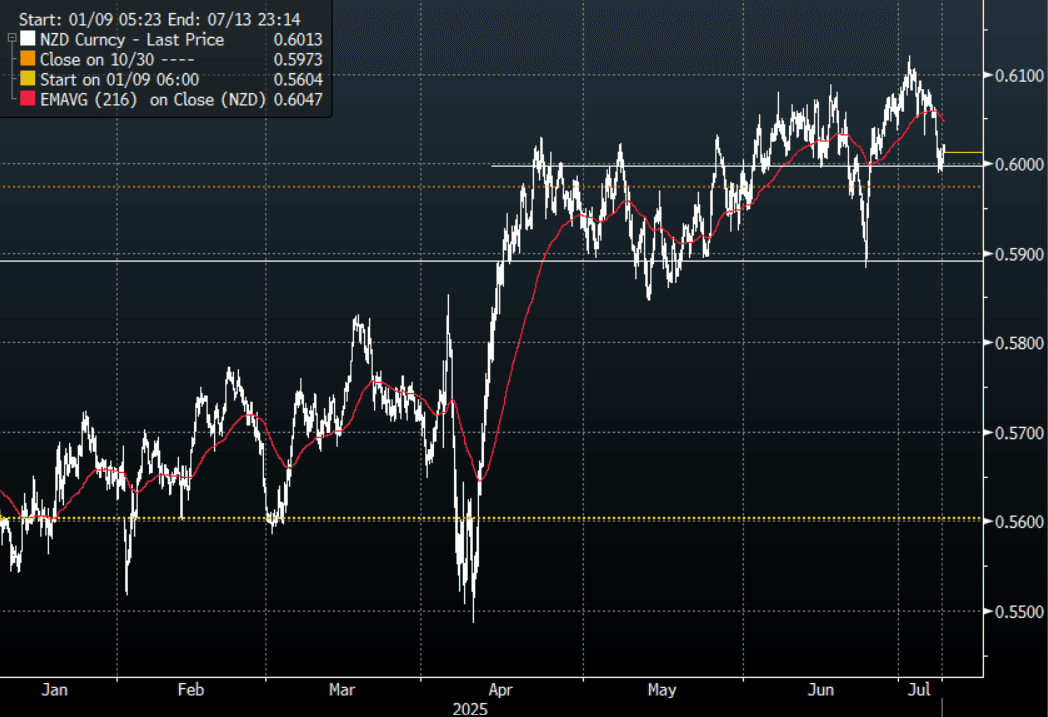

NZD: Asia Wrap - NZD/USD Demand Seen Just Below 0.6000

The NZD/USD had a range of 0.5995 - 0.6021 in the Asia-Pac session, going into the London open trading around 0.6015, +0.32%. The pair has drifted higher for most of our session as the market tries to view the Europe trade deal as a potential playbook and hopes that the Aug.1 deadline has not been set in stone. US Equity futures turned positive after opening lower in Asia, ESU5 +0.04%, NQU5 +0.20%. We have seen this ‘movie’ before and it normally ends with the USD faltering and moving lower again, is this time different ? The NZD found support again around the 0.6000 area as it tries to build a base from which to move higher, a sustained break below here though would risk a deeper correction back to 0.5850/0.5900.

- MNI RBNZ Preview-July 2025: Likely On Hold. The sell-side consensus is for the RBNZ to remain on hold tomorrow, which is also consistent with market pricing. There are some sell-side forecasters looking for a rate cut tomorrow, whilst most of those who see the RBNZ on hold, see risks of further cuts as we progress through 2025. For this meeting, our own bias is for the central bank to hold policy rates steady.

- RBNZ dated OIS pricing is little changed across meetings today, ahead of tomorrow's RBNZ Policy Decision. 3bps of easing is priced for this week's meeting, with a cumulative 32bps by November 2025.

- The NZD/USD has lost all its upward momentum and is back testing its support around the 0.6000 area. If risk has a deeper correction and the USD can find some upward momentum the risk is a move back towards the 0.5850/0.5900 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9), 0.6000(NZD407m July 10), 0.6025(NZD373m July10).

- CFTC Data shows Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0820 - 1.0839, currently trading 1.0830. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some direction. Can the RBA today and RBNZ tomorrow give this pair the energy it needs to move higher again ?

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P