MNI US Macro Weekly: The Fog Of Warsh

Jan-30 21:43By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- The largest rate moves of the week surrounded President Trump’s selection of former Fed Governor Kevin Warsh as the next Fed chair when Powell’s term in the position ends in May.

- A next Fed cut is close to being fully priced for the June meeting again (22bp, the first meeting under the new Fed chair) whilst there are two 25bp cuts fully priced by year-end.

- While historically more hawkish than most of the other contenders but also favoring economic productivity arguments for expecting inflation to remain in check amid solid growth, there remains high uncertainty on what the Fed might look like under Warsh’s leadership. (More from our Policy Team on page 18.)

- That includes policy on the balance sheet (preferring a smaller one) and communications, the Fed’s reach outside of core monetary policy channels, and even personnel, having previously said "I think what we need is regime change at the Fed, and that's not just about the Chairman, it's about a range of people...it's about breaking some heads, because the way they've been doing business is not working."

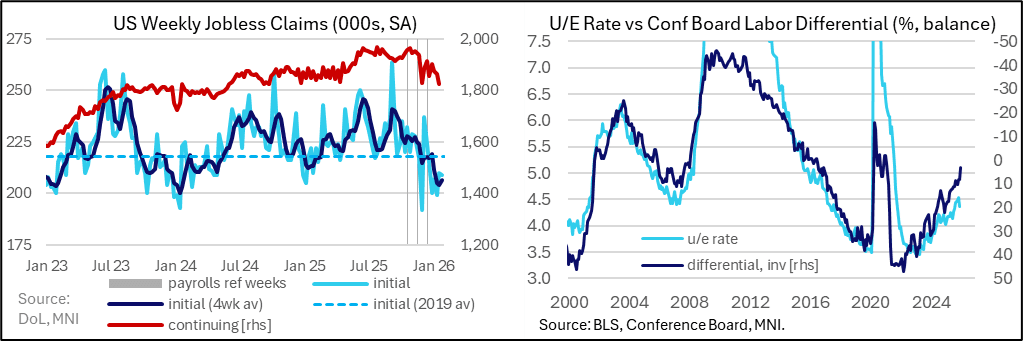

- Warsh or not, one impetus for consensus on a resumption of Fed easing would be a clear deterioration in the labor market, but here the data evidence remained mixed. Jobless claims remain at a healthy level despite initial claims surprising higher for the first time since Dec 11 after a particularly impressive run but with residual seasonality concerns. Continuing claims pushed lower still however but also with some questions over the role of unemployment insurance eligibility roll-off.

- A further acceleration of strong core PPI inflation trends had little impact on Friday against a backdrop of precious metal prices tumbling, whilst details confirmed strong core PCE estimates at ~0.4% M/M for Dec.

- Real GDP growth tracking for Q4 has been trimmed from 5.4% to a still very strong 4.2% after latest volatility in monthly trade reports. Capital goods imports are up strongly in tech-led strength but consumer and industrial imports are down heavily in a hangover from tariff front-running in Q1.

- Manufacturing firms’ sentiment firmed in January but consumer confidence slumped, with the lowest Conference Board metric since 2014 as consumer labor market perceptions softened further.

- The FOMC treaded a largely neutral path with its January decision, maintaining its easing bias but sounding slightly more patient in making its next move than it did last month. Markets took a very mildly hawkish interpretation with implied rates rising under 1bp for meetings to July but even less of a move further out, and the dollar remaining largely unmoved.

- Looking ahead, another government shutdown looms, starting Saturday, but with questions over its potential duration and breadth. In the event the BLS isn’t impacted, the nonfarm payrolls report for January will highlight the week’s economic data on Friday. The report will include benchmark revisions and will continue to see attention on the unemployment rate after its recent stalling around the 4.4% mark.

- We also get Treasury’s quarterly financing and borrowing updates, with attention on any revisions to its guidance on future increases in auction sizes.