ASIA STOCKS: Positive Inflow Momentum Slowing Somewhat

Yesterday saw little net aggregate offshore equity inflows for the Asia Pac region. Inflows for South Korea and India were offset by net selling for Taiwan. South Korean net inflows are positive for the past 5 trading days, but still modestly negative for August to date. Headlines have crossed earlier that Samsung and Hynix won't be subject to the 100% chip tariff that US President Trump stated earlier (which will apply to companies which aren't producing or planning to produce chips in the US).

- For Taiwan, yesterday's outflow coincided with the Taiex falling by 0.90%.

- Indian markets saw some positive inflow momentum, but outflows persist August to date.

- In South East Asia, Thailand flows are generally on a positive trend, while Malaysia has mostly seen outflow pressures since the start of the month.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 200 | 193 | -4929 |

| Taiwan (USDmn) | -404 | 1203 | 3059 |

| India (USDmn)* | 178 | -934 | -11220 |

| Indonesia (USDmn) | 27 | -83 | -3755 |

| Thailand (USDmn) | 61 | 164 | -1690 |

| Malaysia (USDmn) | -41 | -188 | -3117 |

| Philippines (USDmn) | 4 | 0 | -628 |

| Total (USDmn) | 24 | 355 | -22279 |

| * Data Up To Aug 5 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Is This The Catalyst For Some Reversion

The ESU5 overnight range was 6246.25 - 6315.00, Asia is currently trading around 6274. US Stocks pulled back from their highs overnight in reaction to the potential new tariffs being implemented. This morning has seen US futures open a little lower but has since bounced, ESU5 -0.02%, NQU5 +0.10%. Stocks have had an unbelievable run forcing an underweight market to get back in, the short term looks a little stretched now and the shorts have been carried out, could these tariffs and the threat it poses to global growth be the catalyst now for some reversion back to the mean ? Support seen back towards the 6000 area.

- Gavekal on LinkedIn - “The US corporate credit spread has largely ignored two significant macro concerns this year: the "reciprocal" tariffs and the Israel-Iran conflict. The calmness in the corporate credit market may be attributed to an improvement in corporate balance sheets which has lowered the risk of defaults.”

- Lance Roberts on X: “ Why the Sell America theme was always a bad idea...

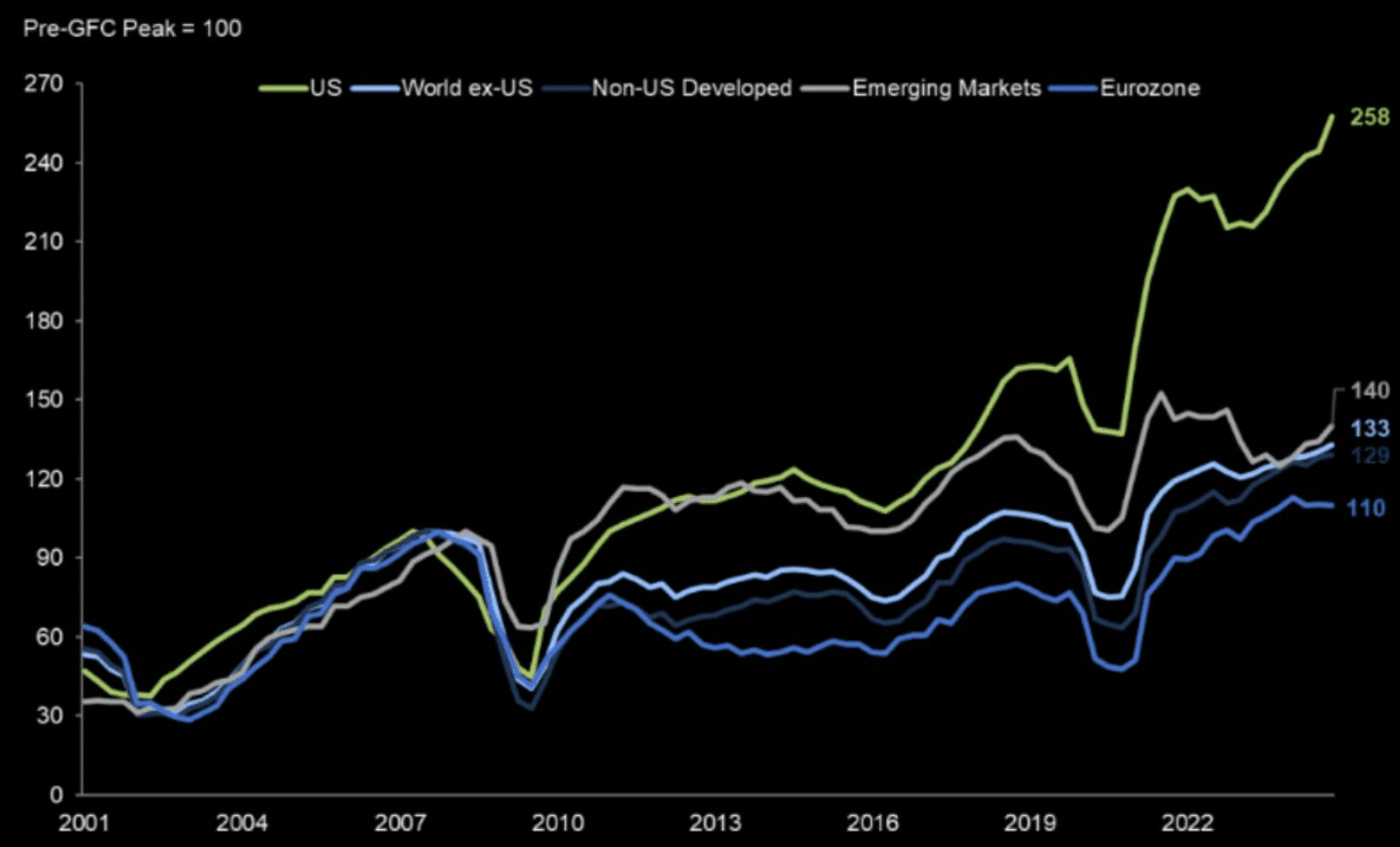

- "This plots earnings growth of the US vs various cuts of ROW (12-month trailing EPS, expressed in local FX). To my eye, it clearly demonstrates why US equities have outperformed so much in the post-GFC era (particularly post-COVID). Now the debate turns on whether that immense gap is set to converge, or not" - GS” See Graph Below

- “As noted in this weekend's BullBearReport, professional investor allocations jumped sharply last week to 99.30. Such a reading often occurs around short-term market peaks.”

- Short-term this is starting to look a little overdone. Could the risks to global growth from the new tariffs give the market some pause ? First support is back towards the 6000 area.

Fig 1: US Earnings Growth Vs ROW

Source: MNI/@LanceRoberts/GS

US TSYS: Cash Open

TYU5 is trading 111-00, up 0-02+ from its close.

- The US 2-year yield opens around 3.89%, down 0.01 from its close.

- The US 10-year yield opens around 4.38%.

- (Bloomberg) -- In the week ended July 1, asset managers' net long positioning in both 5- and 10-year note futures surged to record amounts, according to latest CFTC data released Monday. Over the reporting week, net positioning among asset managers in 5-year note futures extended by $20m/DV01 and by $12.1m/DV01 in 10-year note futures, pushing net positioning in both to record longs.

- (Bloomberg) -- US interest-rate strategists at JPMorgan recommended exiting their week-earlier call to short two-year Treasury notes following the surge in yields sparked by June employment data released Thursday.

- “While we could see front-end yields continue to move somewhat higher from current levels if the June inflation data released later this month shows a material acceleration from recent months, we expect yields to remain within a fairly tight range through the summer”

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- Data/Events: NFIB Small Business Optimism

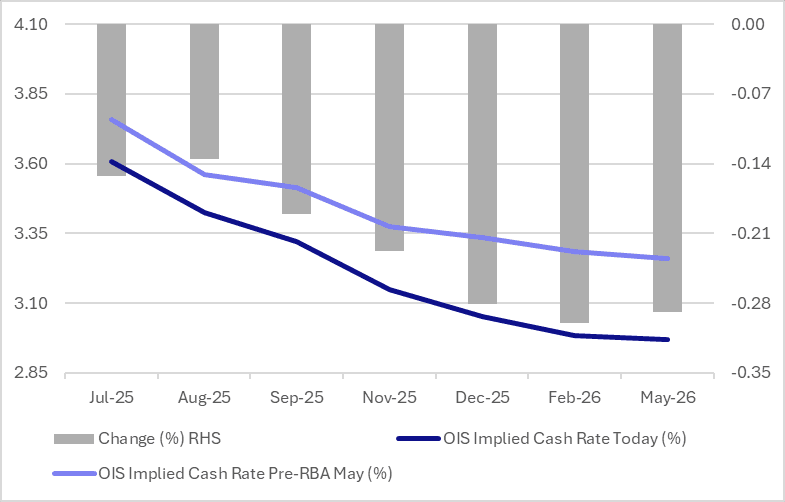

STIR: RBA Dated OIS Almost Fully Priced For A 25bp Cut Today

RBA-dated OIS pricing is slightly firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 94% probability, with a cumulative 79bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, pricing across meetings is 14-30bps softer than levels before the May 20 RBA Meeting.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA (May)

Source: Bloomberg Finance LP / MNI