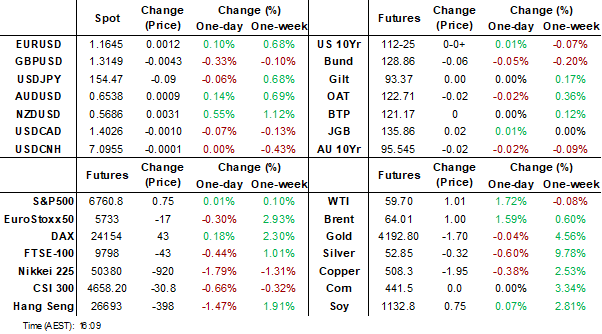

MNI EUROPEAN MARKETS ANALYSIS: Asia Pac Equities Falter

- GBP/USD was under pressure early as headlines crossed that plans to raise income tax rates had been shelved ahead of the upcoming budget. The USD has mostly fallen elsewhere, with NZD and KRW rebounding.

- Japan equities were weighed down by PM Takaichi comments, while tech sensitive bourses have faltered elsewhere.

- China data for October was mostly weaker than forecast, particularly for investment and property related indicators, although retail sales was stable.

MARKETS

US TSYS: UST Yields Modestly Higher on the Week

US bond futures were flat to modestly down in the Asia trading day, failing to take the overnight lead. Stuck below a key technical, the 10-Yr TYZ5 if flat on the day at 112-24+ having traded below the 50-day EMA of 112-26+ overnight.

Cash was better bid, having tried to move higher throughout the morning. All maturities out to 10-Yr are down -0.4 - 0.8bps whilst longer bonds are still suffering from the overnight weak 30-Yr auction.

- The 2-Yr is at 3.58% (+2bps for the week)

- The 5-Yr is at 3.70% (+2bps for the week)

- The 10-Yr is at 4.10% (+1bps for the week)

- The 30-Yr is at 4.71% (+1bps for the week)

A story in the New York Time suggests that President Trump is preparing tax exemptions in a bid to lower food prices, which have been a cause of anxiety for consumers. If successful, this could lower inflation, and bring rate cuts in 2026 back on the agenda.

We saw a sizeable block curve steepener going through in Asia trading: BUY 8600 of TUZ5 traded at 104-04 1/4, post-time 13:10:10 AEST (DV01 $320,084). The contract is currently trading at 104-04 3/8, unchanged from closing levels. SELL 3600 of UXYZ5 traded at 115-13+, post-time 13:10:10 AEST (DV01 $322,756). The contract is currently trading at 115-14+, -0-02 from closing levels.

There are no major auctions in the calendar tonight and data releases remain uncertain. Key will be whether investors follow on from last night's lead.

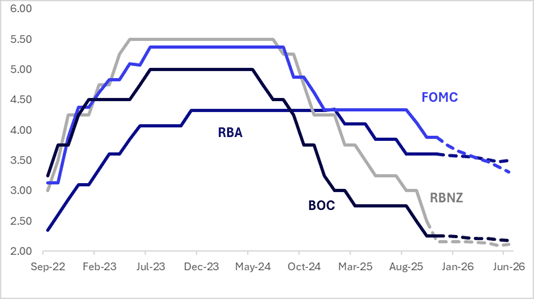

STIR: $-Bloc Pricing Out To Jun-26 Firmer Over The Past Week

Interest rate expectations across the $-bloc out to mid-2026 have firmed over the past week, with Australia (+9bps), Canada (+9bps), the US (+5bps) and New Zealand (+2bps).

- In Australia, the labour market normalised, with unemployment returning to 4.3% after September’s 4.5% spike. Employment rose 42.2k (all full-time) following 12.8k in September.

- OIS pricing now implies just a 1% probability of a 25bp December cut (9% pre-data), with cumulative easing of 10bps priced by mid-2026 (down from 17bps).

- Even still, as previously noted, markets may still be overestimating the likelihood of further cuts, given that rising annual inflation has historically ended RBA easing cycles.

- In the US, renewed scepticism over prospects of a Fed cut in December received a boost from recent commentary from Fed officials. Indeed, the likely lack of new CPI and up-to-date labour market reports before the December 10 FOMC decision implies that it will be even more difficult to shift hawks' inertia.

- The next key regional event is the RBNZ policy decision on November 26. 26bps of easing is priced for November, with a cumulative 35bps by February 2026.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.31%, -56bps; Canada (BOC): 2.18%, -7bp; Australia (RBA): 3.52%, -8bps; and New Zealand (RBNZ): 2.12%, -38bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

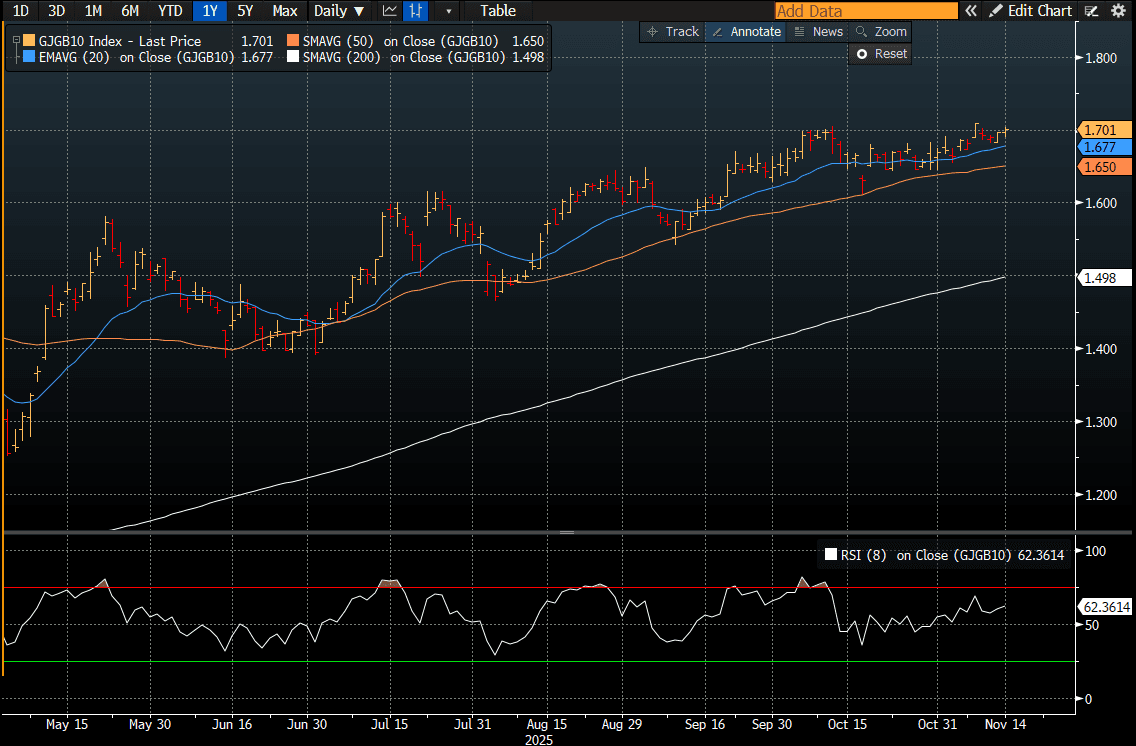

JGBS: 10YY Back At Cycle Highs

JGB futures are slightly weaker, -4 compared to settlement levels, after trading in a narrow range.

- The local calendar was light today. The Tertiary Industry Index is due shortly.

- Cash US tsys are 2-5bps cheaper in today's Asia-Pac session after yesterday's bear-steepener. Renewed scepticism over prospects of a Fed cut in December received a boost from recent commentary from Fed officials.

- Cash JGBs are little changed across benchmarks out to the 7-year and 1-2bps cheaper beyond. The benchmark 10-year yield is 0.5bp higher at 1.701% versus the cycle high of 1.709%. (see chart)

- Swap rates are flat to 1bp higher.

- On Monday, the local calendar will see Q3 GDP (P), Capu (Sep) and IP (sep) alongside 10-year Inflation-Linked supply.

- (Bloomberg) "Japan's real gross domestic product is forecast to contract by 2.4% in the three months through September on an annualised basis, the first decline in six quarters. The Takaichi government is looking to approve its first economic package in the coming week, with analysts predicting fresh spending to reach around 15 trillion, according to a median estimate in the Bloomberg poll."

Source: Bloomberg Finance LP

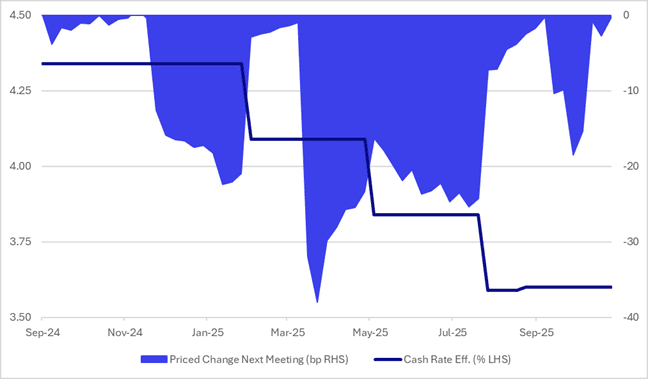

AUSSIE BONDS: Twist-Steepener, Dec Cut Gone But Hopes Remain For 2026

ACGBs (YM +1.5 & XM -3.0) are mixed as the short-end consolidates yesterday's post-jobs sell-off while the long-end follows global yields higher.

- Cash US tsys are 2-5bps cheaper in today's Asia-Pac session.

- Cash ACGBs have twist-steepened, with yields 2bps lower to 3bps higher. Yields remain 8-9bps higher than yesterday’s pre-jobs levels.

- The AU-US 10-year yield differential is at +33bps. At this level, the differential is through the top of its well-defined +/- 30bps trading range. However, with the market still pricing in a 40% chance of a 25bps cut by mid-2026, AU-US 10-year differential narrowing trades may still be premature.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 1% probability (see chart), with a cumulative 10bps of easing priced by mid-2026.

- The bills strip is flat to +4 across contracts, with a flattening bias.

- On Monday, the local calendar will be empty.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

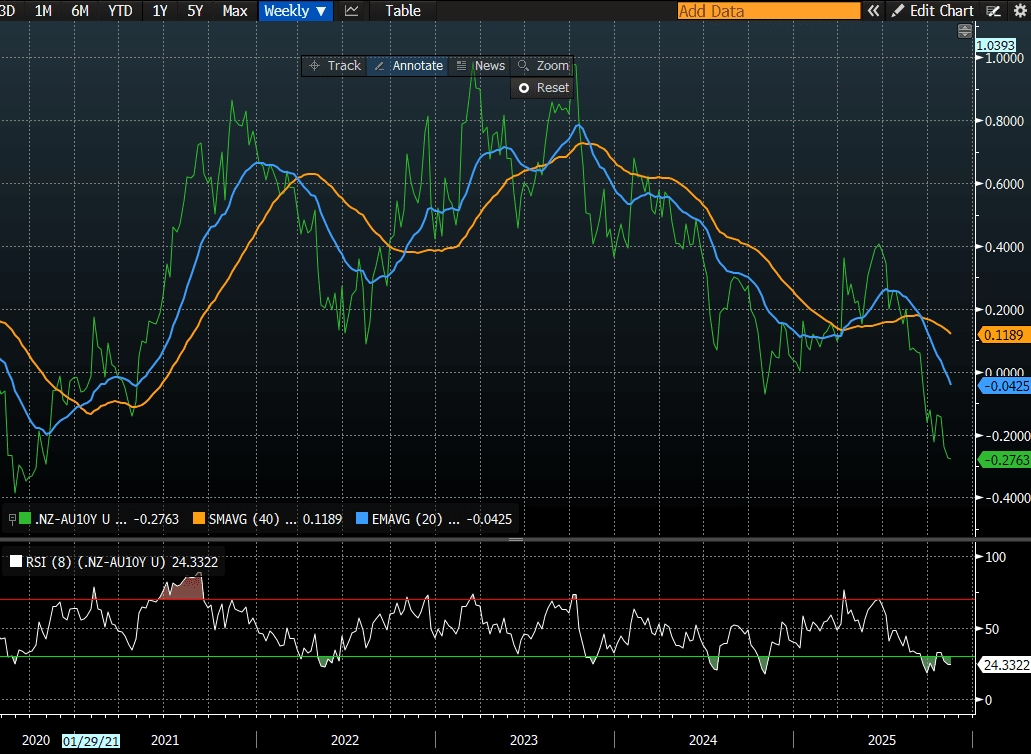

BONDS: NZGBS: Bear-Flattens But Outperforms $-Bloc

NZGBs closed showing a modest bear-flattener, with benchmark yields flat to 2bps higher.

- Cash US tsys are 2-5bps cheaper in today's Asia-Pac session after yesterday's bear-steepener. Renewed scepticism over prospects of a Fed cut in December received a boost from recent commentary from Fed officials.

- NZGBs did, however, outperform their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 4bps and 2bps tighter, respectively. At -28bps, the NZ-AU differential hovers just shy of its cyclical low of -30bps, the most negative since 2020. (see chart)

- Swap rates closed with rates flat to 3bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 25bps of easing is priced for November, with a cumulative 35bps by February 2026.

- Interest rate expectations across the $-bloc out to mid-2026 have firmed over the past week, with Australia (+9bps), Canada (+9bps), the US (+5bps) and NZ (+2bps).

- (Bloomberg) “The RBNZ will ease mortgage loan-to-value restrictions, effective Dec. 1.”

- On Monday, the local calendar will see the Performance Services Index.

Bloomberg Finance LP

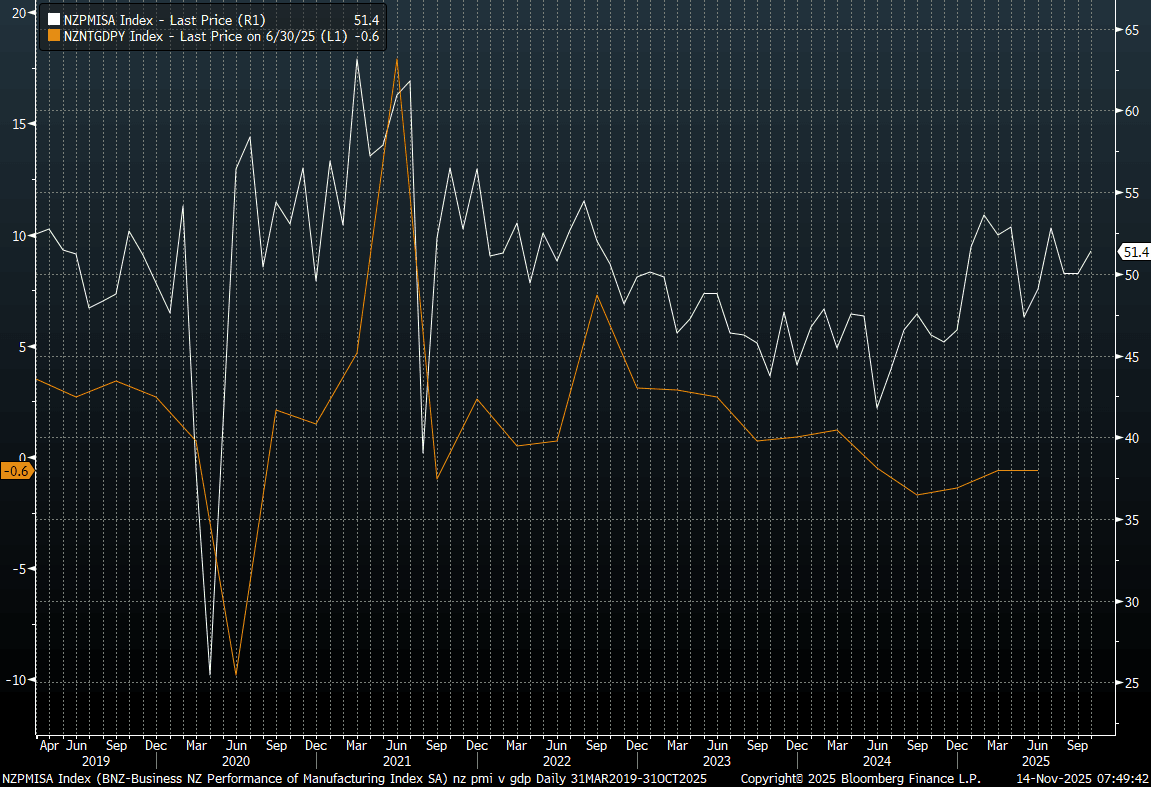

NEW ZEALAND: PMI Rise Points To Recovery, But Index Short Of 2025 Highs

New Zealand's BusinessNZ Manufacturing PMI rose to 51.4 in Oct, from a revised 50.1 outcome in Sep (originally reported as 49.9). The index has been above the 50.0 benchmark since July of this year, but we remain sub earlier 2025 cycle highs (53.6 recorded in Feb), see the chart below. The other line on the chart is NZ y/y GDP growth. We don't get Q3 GDP until Dec 18. Given the y/y decline in Q3 last year was -1.7%, base effects should help y/y momentum for Q3 this year, but broader evidence around the economic recovery remains patchy.

- In terms of the PMI detail, production rose to 52.0, from 50.5, while employment edged up to 48.1 from 47.7. We haven't been in expansion for this sub index since April.

- New orders bounced to 54.9, from 50.5, an encouraging sign, but this just takes us back to where we were in August for this index.

Fig 1: New Manufacturing PMI & GDP Y/Y

Source: BusinessNZ/BNZ/Bloomberg Finance L.P./MNI

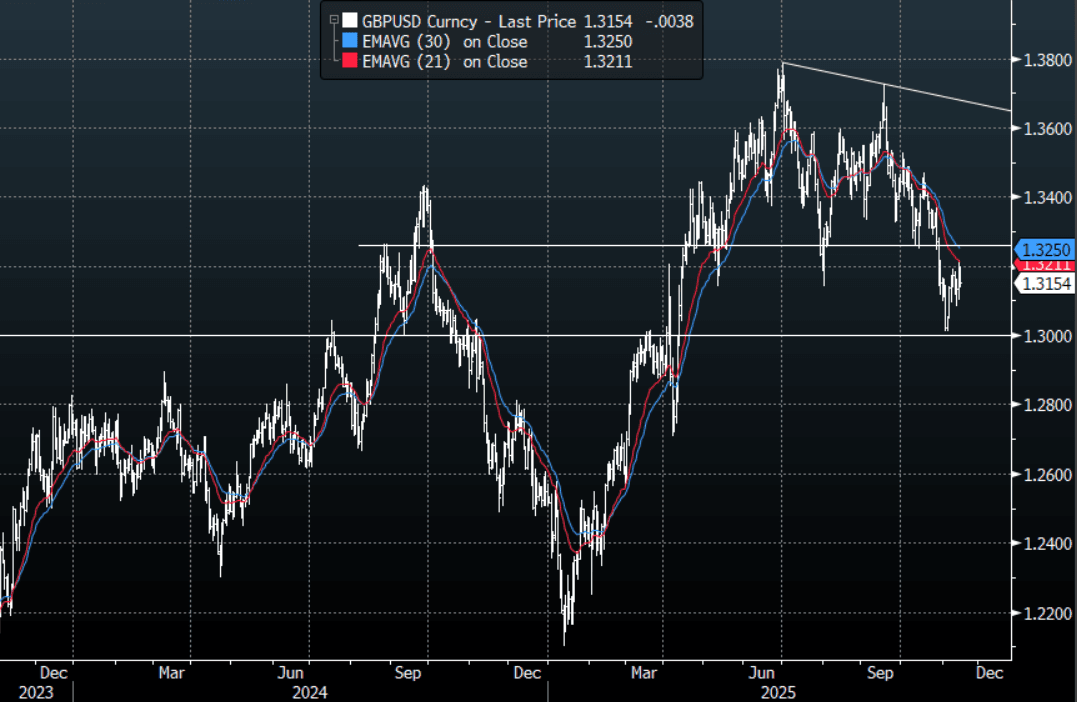

GBPUSD: GBP/USD - Slides Lower After Stalling Above 1.3200 On FT Report

The overnight range was 1.3101 - 1.3213, Asia is currently trading around 131.55, -0.30%. GBP/USD stalled back above the 1.3200 area overnight and for the most part seemed to be ignoring the reversal in global risk sentiment. This morning's FT report that "Starmer and Reeves ditch Budget plan to increase income tax rates", has seen Cable play catch up to the move. Should this squeeze lower in risk expand and force those positioned for the “year-end” rally to pare back then Sterling could come back under some pressure. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I was hoping for a deeper pullback toward the 1.3250-1.3300 area but we never quite got there. If this move lower in risk builds then I suspect rallies on the day back toward 1.3175-1.3200 could be faded, a sustained move back below 1.3080-1.3100 would see the momentum lower reinstated and focus turn back toward the 1.3000 area.

- The GBP/USD Average True Range for the last 10 Trading days: 80 Points

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.3100(GBP330m), 1.2970(GBP638m). Upcoming Close Strikes : 1.3200(GBP407m Nov 19), 1.3250(GBP355m Nov 19) - BBG

Fig 1 : GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

OPTIONS: GBP/USD Downside At 1.3100 Expressed Via Options - DTCC

Early FX option volume trends have been dominated by GBP/USD and EUR/GBP flows. Per DTCC on BBG this is close to 54% of total volumes so far today. For GBP/USD we have seen just over $450mn, for EUR/GBP, close to $190mn. For GBP/USD, puts with a 1.3100 strike, expiry on Nov 17 this year have gone through, while for EUR/GBP a call at 0.8875 (same strike date).

- Latest spot levels for GBP/USD are just under 1.3150. As we noted earlier, a sustained move back below 1.3080-1.3100 would see the momentum lower reinstated and focus turn back toward the 1.3000 area. On the topside moves back to 1.3175/1.3200 today could draw selling interest.

- Spot EUR/GBP was last near 0.8850, near fresh highs back to April 2023.

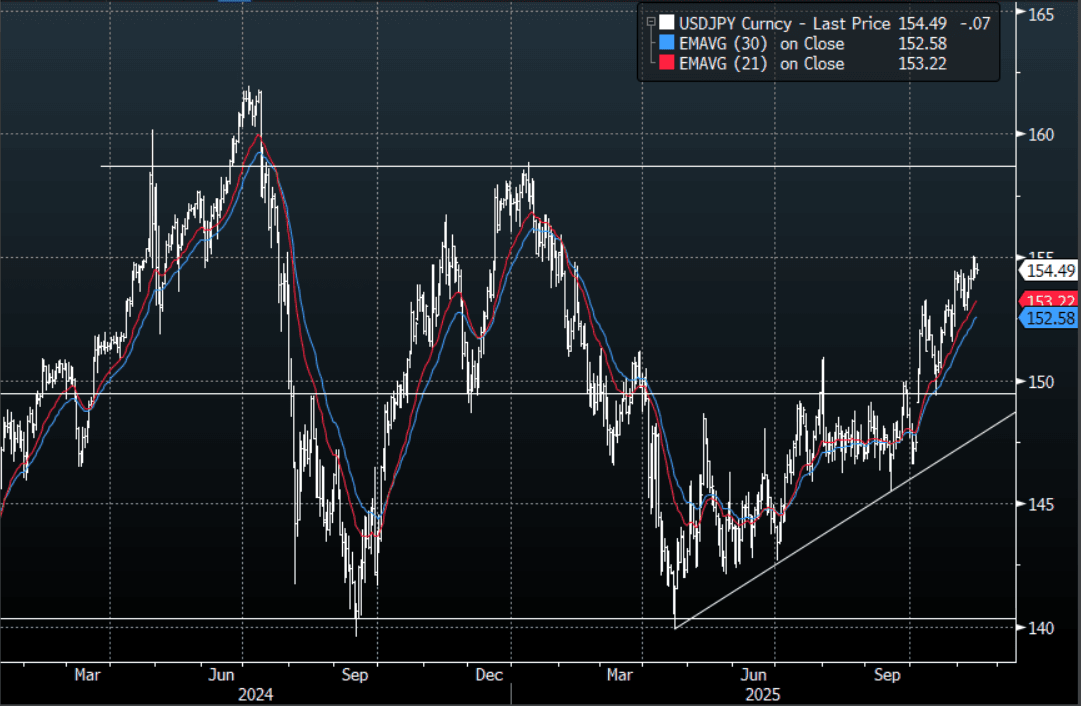

JPY: Asia-Pac: USD/JPY - Drifts Off 154.75 As Yen Bought As A Safe Haven

The USD/JPY range today has been 154.31 - 154.74 in the Asia-Pac session, it is currently trading around 154.45, -0.10%. The pair stalled around the 154.75 area in the Asian session and has drifted lower. Considering the move lower in risk USD/JPY has actually held up ok, probably because the market is starting to question another US cut in December. The overweight positioning in risk looking for a year-end rally is being squeezed across the board, if this has more to play out then Cross-Yen will experience headwinds and the demand for Yen in the crosses should keep the 155.00 area heavy for now. On the day I would be skewed towards looking for some sort of a retracement lower. A sustained break above 155.00 though and the market will start getting excited for another push toward 160.

- "JAPAN PRIME MINISTER TAKAICHI: HARD TO SET NUMERICAL TARGET FOR MINIMUM WAGE NOW, GOVT'S JOB IS TO CREATE ENVIRONMENT THAT ALLOWS FOR FIRMS TO OFFER PAY THAT EXCEEDS PACE OF INFLATION - [RTRS]"

- "JAPAN FINANCE MINISTER KATAYAMA: PLANNED ECONOMIC STIMULUS WILL BE IN LINE WITH TAKAICHI ADMINISTRATION'S PROACTIVE FISCAL POLICY, WHEN ASKED ABOUT SIZE OF STIMULUS - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 155.00($978m Nov17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

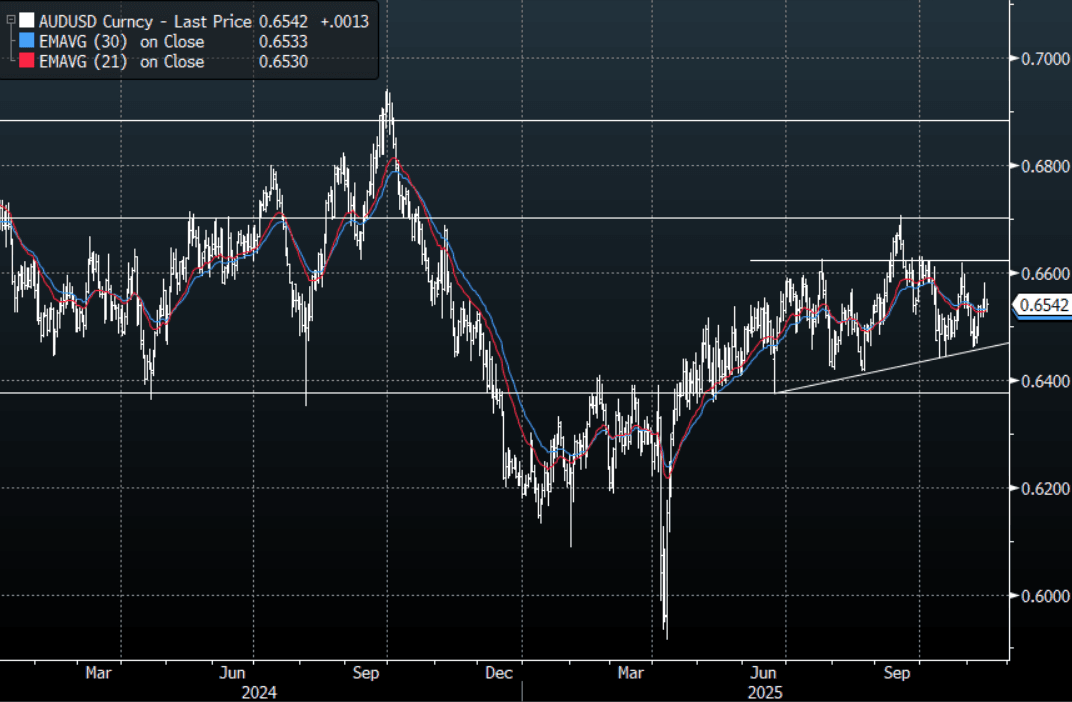

AUD: Asia-Pac: AUD/USD Drifts Toward 0.6550, Look To Fade A Bounce Initially

The AUD/USD has had a range today of 0.6524 - 0.6550 in the Asia- Pac session, it is currently trading around 0.6540, +0.20%. The AUD/USD has drifted higher in our session as Bitcoin finds bids below 100k and US Equity futures managed to lift off their lows. Tough market at the moment but this pull back in US stocks overnight looks to be about positioning with a lot of people set for the supposed “year-end rally.” The AUD/USD put in an ugly shadow on the Daily chart albeit within its recent ranges, on the day though this would suggest to me that this bounce toward 0.6550-0.6560 would be a fade initially looking for a retest below the 0.6500 area.

- MNI INTERVIEW: Spare Capacity Risks 2026 H2 RBA Hike - Fabo. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD670m), 0.6750(AUD2.17b). Upcoming Close Strikes : 0.6400(AUD913m Nov 18), 0.6500(AUD629m Nov 19), 0.6600 (AUD679m Nov 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 45 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

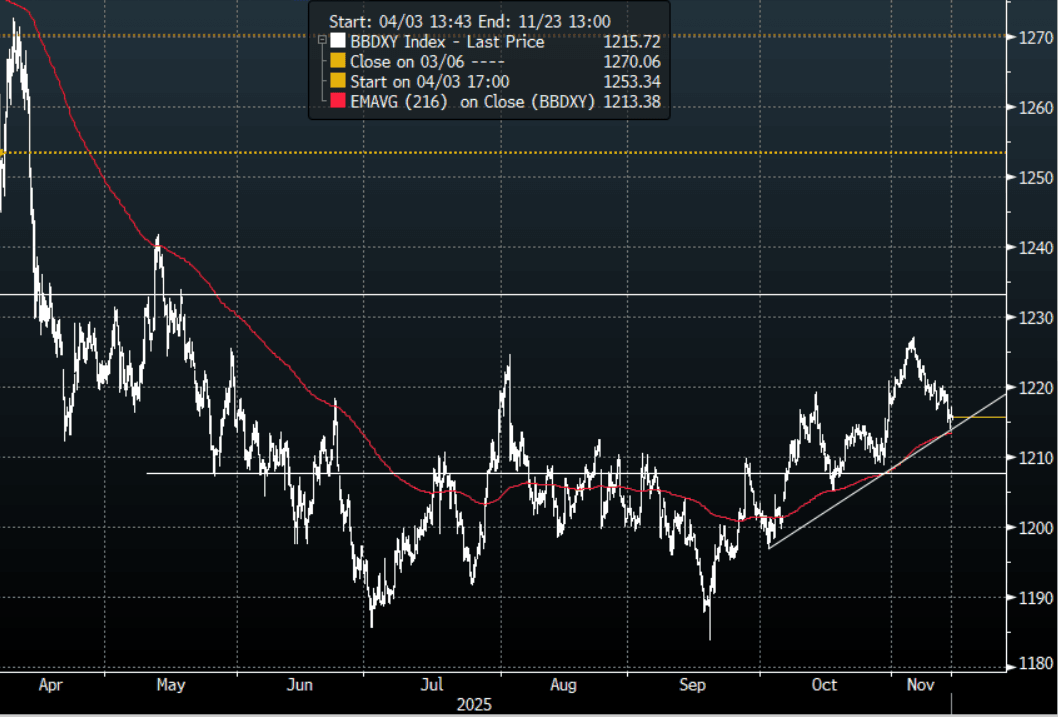

FOREX: Asia-Pac USD: BBDXY Drifts Lower With USD/JPY

The BBDXY has had a range today of 1215.09 - 1217.11 in the Asia-Pac session; it is currently trading around 1215, -0.05%. The USD has drifted off its overnight highs as Asia sells the USD in sympathy with the move lower in USD/JPY, I feel the market will differentiate and buy it against risk currencies into the London open. The USD fell back toward the 1210-1215 support overnight where it found some demand first up. Risk took an ugly turn last night and the USD was late to react, we have seen periods this year where the USD has not traded like a safe haven. Yet the Risk-Reward around this support area for me says this is the side I would be skewed towards. I expect we do some more work around these levels but I would be looking for signs of a base forming from which to move higher again if risk stays under pressure. Short-term the 1221-1222 area remains the pivot on the topside and we would need a move back above there to build for a retest of the 1230-35 area.

- EUR/USD - Asian range 1.1623 - 1.1645, Asia is currently trading 1.1640. The pair has moved into some decent resistance toward the 1.1650-1.1700 area. This has been the pivot within the larger 1.1400-1.1900 range over the past few months. On the day watch for any signs of topping out to express a short looking for a pullback.

- GBP/USD - Asian range 1.3136 - 1.3199, Asia is currently dealing around 1.3150, -0.35%. This morning's FT report that "Starmer and Reeves ditch Budget plan to increase income tax rates, has seen Cable play catch up to the risk-off move. I continue to favor fading rallies though as GBP looks to have put in a medium term top. If this move lower in risk builds then I suspect rallies on the day back toward 1.3175-1.3200 could be faded, a sustained move back below 1.3080-1.3100 support would see the momentum lower reinstated and focus turn back toward the 1.3000 area.

- Cross asset : SPX -0.05%, Gold $4200, US 10-Year 4.118%, BBDXY 1215, Crude Oil $59.57

- Data/Events : France CPI, EZ GDP/Trade Balance/Unemployment Rate, Spain CPI, Italy Trade Balance/General Government Debt

Fig 1: BBDXY Spot 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

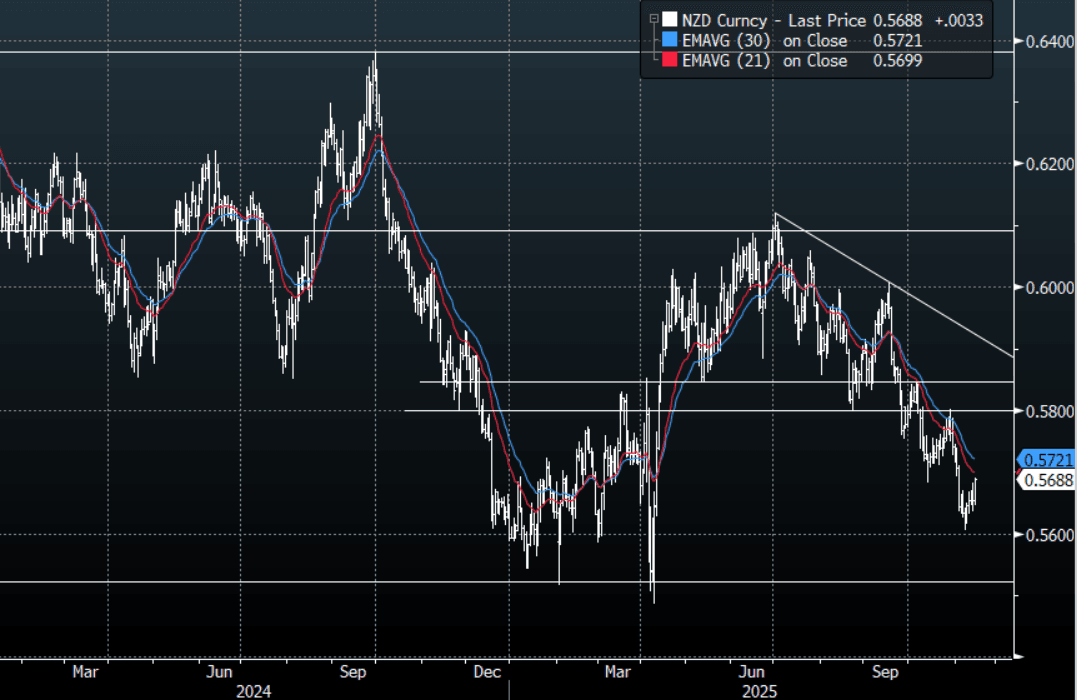

NZD: Asia-Pac: NZD/USD Retraces Overnight losses

The NZD/USD had a range today of 0.5645 - 0.5687 in the Asia-Pac session, going into the London open trading around 0.5685, +0.55%. The NZD has ignored the global woes and retraced all its losses and even breaking the overnight highs, reacting to local inputs. The NZD does stand out as a vehicle to express a short, and if this washout in risk expands it should again be a market favourite. This morning's move could be pointing to positioning with everyone bearish. On the day though should the move in risk build on this correction in the US session I would be skewed to play from the short-side, a move back below 0.5630-40 could see the downtrend reinstated. This would see the focus once again return back toward the 0.5500 lows. Next resistance now back toward the 0.5750 area.

- The Reserve Bank of New Zealand will ease mortgage loan-to-value restrictions, effective Dec. 1, according to a statement. RBNZ will continue to closely monitor housing-related risks and impact of changes.

- MNI AU - PMI Rise Points To Recovery, But Index Short Of 2025 Highs: New Zealand's BusinessNZ Manufacturing PMI rose to 51.4 in Oct, from a revised 50.1 outcome in Sep (originally reported as 49.9). The index has been above the 50.0 benchmark since July of this year, but we remain sub earlier 2025 cycle highs (53.6 recorded in Feb). We don't get Q3 GDP until Dec 18. Given the y/y decline in Q3 last year was -1.7%, base effects should help y/y momentum for Q3 this year, but broader evidence around the economic recovery remains patchy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5730(NZD308m Nov 19), 0.5835(NZD300m Nov19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: JP PM Spooks Markets, Rotation out of Tech Growing

In what could be a sign of things to come, Japanese PM Takaichi essentially warned Japanese businesses focus too little on wealth distribution to employees and too much on shareholders. The overnight lead in was weak as investors feel less confident as to a FED rate cut in December as key officials shared their doubts. Equities will have one eye on bond yields to see if they are to stay elevated as a potential lead into next week's opening. This naturally fed into the part of the market that had run the most, the tech sector, with key companies in this sector now down over 5% over the last week and sector rotation a driving theme.

- The NIKKEI finished the week with heavy falls of -1.6% and is barely holding onto weekly gains, following the PMs comments. The NIKKEI and the KOSPI have both benefited from the huge tech upswing and the downward pressure on the NIKKEI translated to the biggest daily fall for the KOSPI since mid-week last week. The KOSPI is down -2.6% today but holds onto weekly gains of +2.6%.

- China's major bourses are all down today with the CSI 300 now negative for the week. Losses were led by the Hang Seng, down -1.2% yet it retains a +1.8% weekly gain, outperforming the onshore bourses.

- Taiwan's TAIEX is down -1.1% today to give back all gains of the week, for modest losses.

- Despite confirming stronger than expected 3Q GDP, and a currency outperforming regional peers, the FTSE Malay KLCI is down today by -0.3% and holding onto weekly gains of +0.50% whilst the Jakarta Composite's fall of -0.10%, tipped it just into red figures for the week.

- In India, markets are watching for the outcome from the election in Bihar as a key test for PM Modi with the NIFTY 50 down -0.14% at the open Friday, whilst holding onto a weekly gain of +1.3%

OIL: Firmer On Russian Supply Concerns, WTI Still Sub Late Oct Highs

Oil benchmarks have built on Thursday gains in the first part of Friday trade. Brent was last around $64/bbl, up close to 1.3% from end Thursday levels, and modestly higher for the week. Session highs rest at $64.87/bbl. WTI is back around $59.70/bbl, up 1.7% but tracking close to flat for the week (earlier session highs were at $60.65/bbl).

- The potential impact of US sanctions on Russian oil flows is being cited as a reason for bounce (with these sanctions kicking in over the next few days). Via BBG: "On Thursday, the International Energy Agency warned of “considerable downside risk” to its outlook for Russian output from the moves." Risks of US military action against Venezuela, has also been cited as risk factor (per BBG) and may be helping drive short covering ahead of the weekend.

- The broader backdrop still look like oversupply concerns will dominate from a medium term standpoint.

- From a technical perspective, Wednesday's sell-off in WTI futures strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Resistance to watch is $62.59, the Oct 24 high.

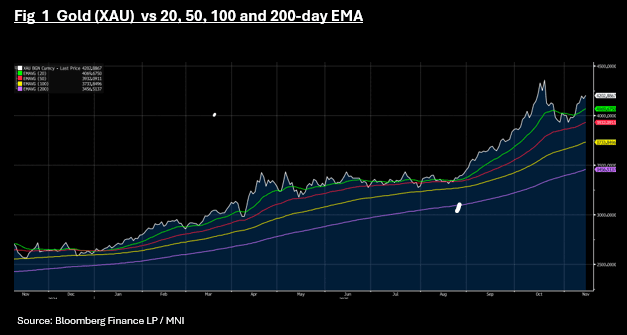

Gold on Track For Best Weekly Return in a Month

- Gold's fall overnight was short lived with buyers stepping in today during the Asia trading day, to rally above last night's closing.

- Up +0.82%, gold stands to finish the week over 5% higher assuming the trajectory remains throughout the EU / US trading days.

- The China Securities Journal reports that " Chinese investors should be aware of risks in gold price volatility and avoid making singular bets on the bullion market, " with comments from an analyst suggesting that "Gold price is still supported by its safe-haven status and central bank buying, but trading has already become very crowded due to rapid gains in short term, increasing the risk of market volatility,." (per BBG).

- Central Banks globally have increased their holdings of gold this year as it rises over 60% year to date in what some see as a diversification away from the USD.

- Gold retains its position above all major moving averages, with the trend for the EMAs upward sloping. This suggests that the positive momentum in gold prices could have more to run.

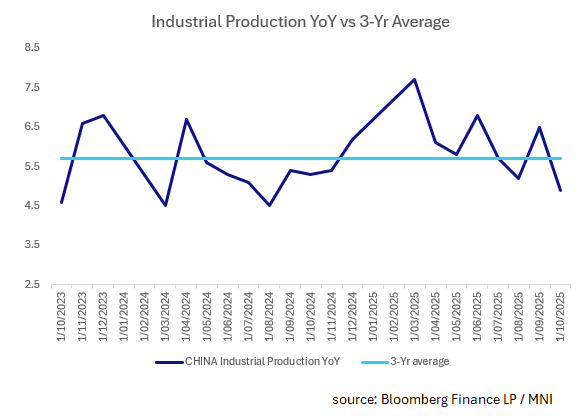

CHINA: Industrial Production Misses Forecasts, Retail Sales Steadies

- Amongst all of the data released today, industrial production were the areas where focus is likely to be.

- The focus on the consumer and domestic demand is the cornerstone to the next 5-Year plan and whilst it seems that retail sales is becoming less likely to return to the days of +10%, October's result was slightly ahead of market expectations.

- Expanding +2.9% against forecasts of +2.8%, and below prior month of 3.00%. With the coming data to capture the Single's Days sales, which by all accounts was a success, there may be upside potentials for retail sales and we look back on October's result as being resilient.

- For industrial production September result was impacted by what appeared to be attempts to get goods out ahead of the Trump Xi meeting and any outcome from trade negotiations. At +4.9%, it missed expectations of +5.5% and below September +6.5%. However since the onset of the trade war in April, there have only been two months with an industrial production expansion below the 3-Yr average. This therefore suggests that the October result may not be a downward trend, rather an reaction to the increase in output in September.

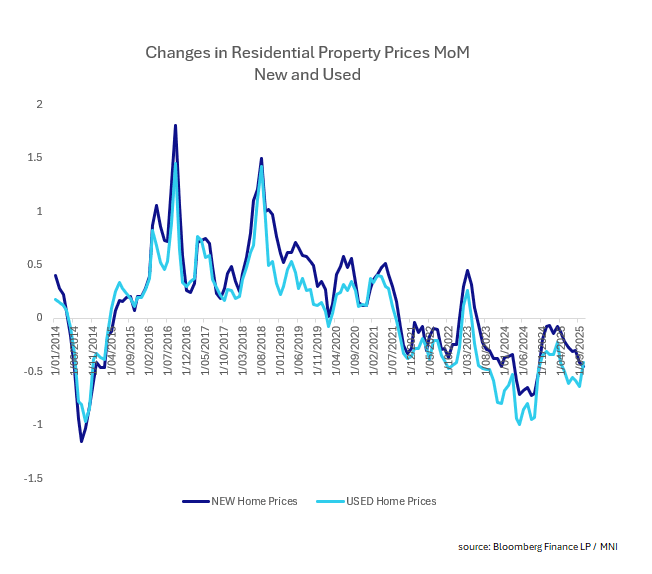

CHINA: Housing Sector Woes Continue

- In a raft of October data, there was no good news for the property sector as the deflationary spiral continues.

- New home prices were down -0.45% in October, from -0.41% in September with Beijing slipping back into decline after one month of appreciation and Shanghai maintaining its modest expansion.

- Used home prices were down -0.66% in October, from -0.64% in September. Home Prices Fell in 64 out of 70 Cities in the survey from the prior month

- You have to go back to early 2023 for the last monthly price increases, as the sector moves into its third year of deflation.

- Aligned with this was an increase in the decline in property investment YTD YoY to -14.7% in October, from -13.9% prior. New home sales value declined 9.4%, whilst new home sales value declined -9.6%.

- Residential property sales declined -9.4% to CNY6tn YoY, from -7.6% the month prior and the worst monthly result this year.

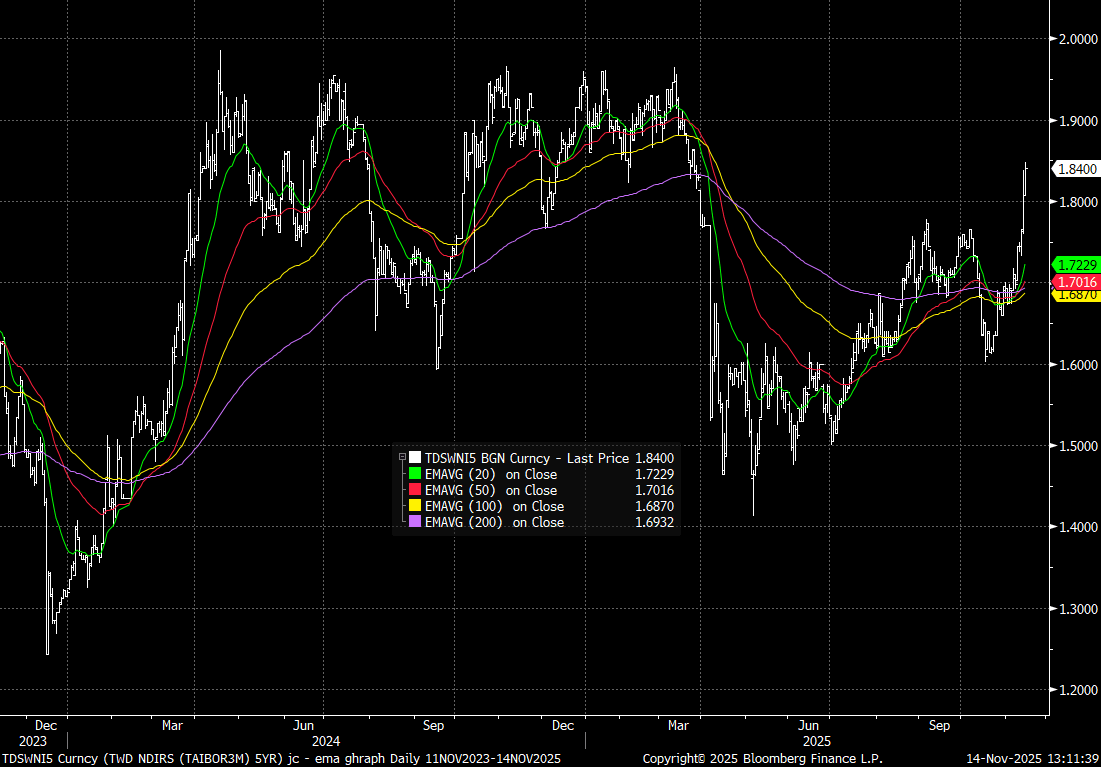

TAIWAN: 5yr NDIRS Surges, As Rate Cut Expectations Erode, TWD Still Weaker

Taiwan's 5yr NDIRS rate has surged higher in recent sessions, last near 1.84%, after starting the week closer to 1.70%. Upside focus is likely to rest around the 1.90-1.95% area, which marked highs in the first part of the year (see the chart below). As we noted earlier in the week, risks were skewed towards steadier policy rate settings in the near term, reflecting a host of factors (including spill over from higher China inflation pressures) (see this link). We saw risks of higher short term rates, with Taiwan likely seeing spilling in recent sessions, via BBG: "“Hedge funds unwound positions after paring back expectations for rate cuts in Asian markets, driving IRS rates higher,” said Henry Lin, an IRS trader at SinoPac Securities".

- The upside projections for Taiwan 2025 GDP growth (with the government noting GDP growth should exceed 5.5% earlier this week), is another factor, although growth projections from the sell-side have been steadily rising in recent months. US and Taiwan officials have also been noting progress in terms of trade talks.

- These rate moves aren't doing much for TWD FX though, which remains weaker, last near 31.125 for USD/TWD, fresh highs back to the start of May this year.

- Equity markets are under pressure amid global tech headwinds, while offshore investors have sold over $1bn of local stocks so far this week. The flagship equity for chipmaking in Taiwan TSMC touched all time highs earlier this month. It is now down almost 5% from those highs on profit taking falling six out of the nine days post the highs.

Fig 1: Taiwan 5yr NDIRS To Fresh Multi Month Highs

Source: Bloomberg Finance L.P./MNI

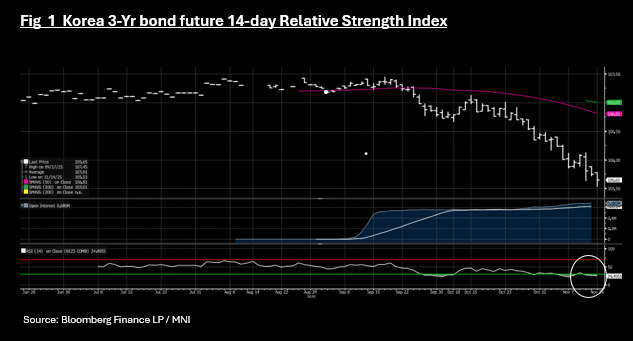

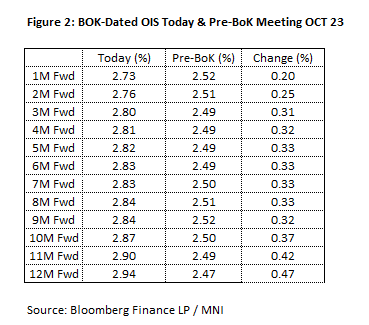

SOUTH KOREA: Bond Market Down Heavily Again, Rate Rises in Play

- The move in Korean bonds this week has been fierce, with bond futures gapping lower again today and KTB yields hitting new highs for the year whilst the move in IRS sees rate rises coming into reckoning.

- The move lower in the 10-Yr bond future takes the contract to 113.76, and oversold on the 14-day relative strength index and down almost 100pts this week alone.

- The 3-Yr future is down -0.10 to 105.65, a new contract low as it moves further into being oversold on the 14-day RSI

- Cash have been hit hard with yield 3-5.5bps higher across the curve. The 10-Yr is at 3.32%, the first time it has been above 3.30% since June 2024.

- Swap markets have re-priced the rate trajectory, with not only all cuts now removed partial rate hikes are priced further out the curve with the 12mth FWD pricing in almost a full rate hike.

- BBG's MIPR function now has +9bps of rate rises priced in over a 1-Yr time horizon.

The governor's comments this week hasn't calmed markets instead markets have focused on key words which was interpreted as rates on hold for a long time, whilst keeping the easing bias. For now the bias is being ignored and the market is pushing hard on the BOK who meet again on November 27. Until then, the pressure on bond yields could provide an interesting input into monetary policy thinking for the committee members.

ASIA FX: USD/KRW Slumps As FinMin Moves To Address FX Imbalances

The best performer in EM Asia FX so far today has been KRW, up 0.80%, as the FinMin stated it would launch efforts to stabilize the FX demand/supply imbalance (including discussions with the National Pension Service (NPS)). We have seen steadier trends elsewhere, with CNH holding the bulk of its recent gains. MYR has lost a little ground, while IDR is off recent highs.

- Earlier highs in spot USD/KRW were close to 1475, before headlines hit that the authorities will step up efforts to improve the FX demand/supply imbalance. The pair was last around 1454, close to session lows. The 20-day EMA is back near 1444, but NPS hedging resumes it should help put a cap in the pair around the 1470/80 region. Implied vols are higher but within recent ranges. The 1 month risk reversal is trending back towards flat and dips sub this level can coincide with further USD/KRW losses if history is a guide.

- USD/CNH sits unhanged around 7.0960, with generally weaker than expected data (particularly on the investment and property side) offset by fresh USD/CNY fixing lows and on-going policy efforts to boost yuan use. Downside risks in USD/CNH may still prevail, with 7.0851, the mid Sep low not too far away Our policy team noted - The PBoC will promote the cross-border use of the yuan in trade, investment and financing, and provide more products to facilitate foreign investor participation in the stock and bond markets, while improving the payment system and incorporating the currency's use into multilateral and bilateral agreement frameworks, Deputy Governor Tao Ling said Friday at the Caixin Summit 2025.

- USD/TWD continues to track higher, despite a sharp rise in local yields, as the market pares back rate cut expectations. We were last near 31.12, close to multi month highs. Local equities have been under pressure amid broader tech headwinds, which is also driving offshore investor outflows.

- USD/MYR has steadied just above the 4.1300 level. This is helping to correct overbought conditions. Q3 GDP revisions painted a firm picture for Malaysian growth though, suggesting upticks will be sold.

- The Rupiah is set to finish with a weekly loss, despite a decent rally Friday. With modest gains today, the Rupiah staved off three days of losses to move back towards 16,700.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/11/2025 | 0700/0800 | ** | Unemployment | |

| 14/11/2025 | 0745/0845 | *** | HICP (f) | |

| 14/11/2025 | 0800/0900 | *** | HICP (f) | |

| 14/11/2025 | 0900/1000 | Foreign Trade | ||

| 14/11/2025 | 1000/1100 | * | Trade Balance | |

| 14/11/2025 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 14/11/2025 | 1030/1130 | ECB Elderson Keynote at ECB Banking Supervision Forum | ||

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/0830 | *** | Retail Sales | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic | ||

| 15/11/2025 | 1330/1430 | ECB Schnabel Chairs Panel at Econ/FinStab Conference |