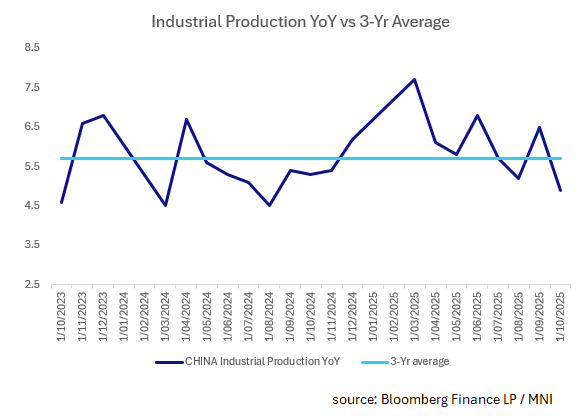

CHINA: Industrial Production Misses Forecasts, Retail Sales Steadies

- Amongst all of the data released today, industrial production were the areas where focus is likely to be.

- The focus on the consumer and domestic demand is the cornerstone to the next 5-Year plan and whilst it seems that retail sales is becoming less likely to return to the days of +10%, October's result was slightly ahead of market expectations.

- Expanding +2.9% against forecasts of +2.8%, and below prior month of 3.00%. With the coming data to capture the Single's Days sales, which by all accounts was a success, there may be upside potentials for retail sales and we look back on October's result as being resilient.

- For industrial production September result was impacted by what appeared to be attempts to get goods out ahead of the Trump Xi meeting and any outcome from trade negotiations. At +4.9%, it missed expectations of +5.5% and below September +6.5%. However since the onset of the trade war in April, there have only been two months with an industrial production expansion below the 3-Yr average. This therefore suggests that the October result may not be a downward trend, rather an reaction to the increase in output in September.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: USD/JPY Under Fri Lows As US 10yr Eyes 4.00% Test, Key EMAs Under 150.00

USD/JPY is continuing to track lower, now under 151.15, up 0.50% in yen terms. This puts us under Friday lows in the pair, but we are still comfortably above key EMAs.

- Focus in the near term may rest on the softer US Tsy yield backdrop. The 10yr at 4.01% is close to recent lows, with eyes on whether we can break under the 4.00% handle. As we noted earlier USD/JPY looks too high relative to yield momentum between US-JP. The USD/CNY fix under 7.1000 has been another positive, while other cross asset trends have been mixed. Gold continues to rally, signifying some safe haven flows are still on-going, but the regional equity mood looks better.

- JPY is outperforming so far in the G10 space, although AUD isn't too far behind, up 0.30% (with similar benefits from the CNY fixing outcome).

- For USD/JPY we are now under late Friday highs, while other support points to note are outlined below. We are still some distance from the 50-day EMA.

- SUP 1: 150.92 High Sep 26

- SUP 2: 149.72 20-day EMA

- SUP 3: 148.50 50-day EMA.

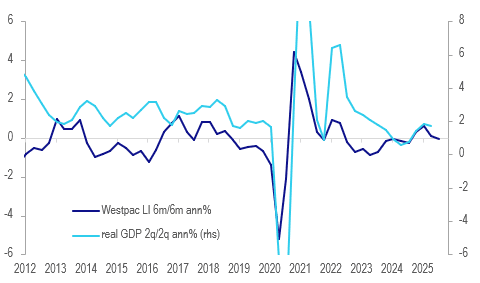

AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months. This measure leads detrended growth by 3 to 9 months and signals that growth may slow in H2 but be around trend early in 2026. Westpac is forecasting 2% growth in 2025 with it improving in 2026.

- Westpac forecast a 25bp rate cut at the November meeting but now believes that while the next move in rates is down, the upcoming decision will rely on Q3 CPI on 29 October. It notes though that its lead indicator signals GDP growth remains lacklustre.

- The indicator was stronger in H1 this year with the H2 moderation driven by dwelling approvals and AUD commodity prices. Westpac expects both of these components to turn with the latter already higher driven by gold and lower rates and policy likely to boost housing supply.

- Equity prices have been positive for the lead indicator over the last 6 months.

Australia Westpac lead indicator vs GDP %

JGBS: Futures Dips Supported As Tsys Push Higher, 20yr Auction Later

JGBs were a touch softer in the first part of trade, but sit back at 136.32, only -.01 versus settlement levels in latest dealings. The turn higher in US Tsy futures is likely providing some positive spill over for JGBs. Focus in the cash Tsy yield space will be on whether the 10yr yield can test under 4.00% (latest around 4.015%).

- For JGBs broader ranges continue to hold, with upside resistance still intact, while Tuesday highs were just above 136.50.

- In the cash JGB space, back end yields are softer for the 10yr through to 40yr. The 10yr last around 1.65%, 20-40yr tenors off 2-4bps. The 30yr leading.

- The front end of the curve is more stable, leaving the 2/30s curve flatter by 5bps to +228bps.

- We have the 20yr auction later.

- The opposition parties will meet at 4pm local time, ""*JAPAN'S TAMAKI: TO HOLD 3-WAY OPPOSITION PARTY TALKS AT 4 P.M.", via BBG. This comes ahead of next week's Diet session on Oct 21, where a new PM is expected to be elected. Uncertainty continues on who this will be, but Polymarket still has odds with LDP leader Takaichi.