ASIA: Inflation Green Shoots Could See Rates on Hold for Near Term

Nov-12 03:44

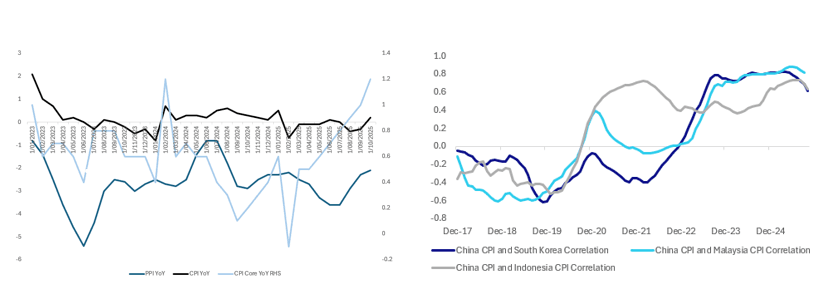

- Over the weekend, China's YoY CPI rose to +0.2%, after months of flipping between very modest to no inflation and deflation. Core inflation however jumped to +1.2%, it's highest reading in over a year.

- The Q3 Monetary Policy Report described inflation as 'weak' whilst the broader economy as stable and fundamentals solid. Following this report Goldman Sachs pushed their rate cut call out to Q1 2026, from Q4 2025.

- Over the last decade in various cycles China's deflation challenges have impacted the region. In 2014-16 a commodity slump pushed on a slowing economy after years of heavy investment particularly in manufacturing resulting in Asia facing cheap Chinese imports, which pushed PPIs in the region negative. From 2018-19 the early stages of the trade war under the Trump administration resulted in manufacturing excesses being dumped in the region, pushing down producer prices. Again in 2023-25 manufacturing overcapacity, particularly from EV related industries has seen extreme price competition, pushing down producer prices in the region.

- PPI's correlation to CPI is strong. Likewise CPI's correlation to Core. As core rises, it is likely to result in CPI rises, which in turn can feed into PPI. Whilst PPI and CPI remain negative and barely positive, it is their delta that raises the most interest. From their lows they have retraced 40% for PPI and 120% for CPI and with Core CPI now pushing to it's highest since 2022, are we about to see a bottoming and or a resurgence of inflation and what does that mean for the region and the rate cycle?

Fig 1: China PPI YoY, CPI YoY and Core CPI YoY & China CPI Correlations with Korea, Malaysia + Indonesia - Rolling 3yrs

source: Bloomberg Finance LP / MNI

- Regionally, whilst on an historical comparison CPI remains low, the delta of CP from lows is worth noting.

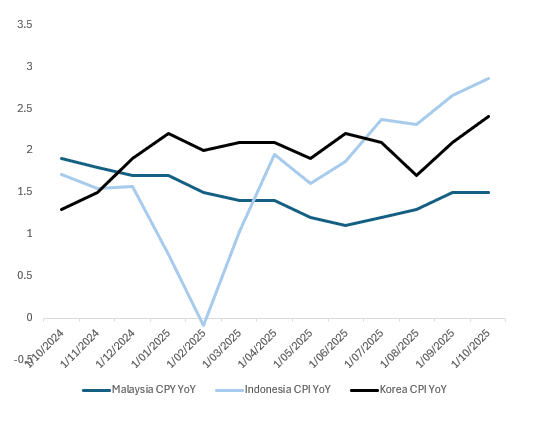

Fig 2: Malaysia, Indonesia & Korea CPI YoY

source: Bloomberg Finance LP / MNI

- When looking back, Malaysia' meeting last week could mark the turning point in the rates cycle for region. Bank Negara (BNM) held rates steady with a balanced assessment of inflation and growth, a view likely re-enforced by the US trade deal. The BNM sees inflation as contained through 2026 noting global costs moderating. The BNM cuts rates only once whereas the Bank Indonesia five times and Bank of Korea four times.

- The BOK faces a housing crisis with house price escalation at the forefront of policymakers minds. When added to the trend in CPI, it suggests the BOK could be on hold for some time.

- In Indonesia, the Rupiah has lost -2.5% over the last three months and is down -3.4% year to date. This at a time when 3Q GDP topped 5% and the JCI is up 40% from the trade war induced April lows.

- As US rate cuts now appear less certain, the outlook in Asia appears similar. What could follow for Asia's Central Bank's could be an extended hold, with those markets with rate cuts priced in still, progressively taking them out.

- The Goldman Sachs change may just be the start of more to come across the region, as rate cut expectations get pushed out. Central Bank's need to maintain flexibility to cut rates further and worry about taking rates too low especially if their currencies are pressurized.

- The BOK is on hold for now with the BNM joining them. Markets will watch with interest as the BI deals with the competing interests of a pro-growth government and a currency that won't rally.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: September Exports Surge (Ex US) as Trade War Intensifies

Oct-13 03:18

- The moderation of exports in August was short-lived as September's numbers jumped +8.3% YoY, beating expectations and much stronger than the month prior.

- According to BBG estimates, the decline in exports to the US was significant, down -27% YoY. This points to the growth of demand from non US markets, arguably weakening the US's position in a trade war. Exports to Africa, India and other Asian nations are soaring with the latter back to pre-COVID levels.

- US President Donald Trump had threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures.

- The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times.

- Imports climbed +7.4% in September for it's largest monthly expansion since April 2024. Despite being a crude indicator for domestic demand, the result nevertheless comes a an invaluable time as the US rhetoric ramps up.

- Along with the decline in exports to the US, imports from the US declined -16.1%, widening the trade surplus with the US to $22.bn.

- Whilst this data captures a period before the weekend's escalation it may slightly strengthen Beijing's position in negotiations, given the ever growing decline in the US's importance to China's trade outcome.

MNI: CHINA YTD EXPORTS +7.1% Y/Y IN YUAN TERM: CUSTOMS

Oct-13 03:07

- CHINA YTD EXPORTS +7.1% Y/Y IN YUAN TERM: CUSTOMS

- CHINA YTD IMPORTS -0.2% Y/Y IN YUAN TERM: CUSTOMS

- CHINA YTD TRADE SURPLUS +CNY6.28 TRLN: CUSTOMS

MNI: CHINA SEP EXPORTS +8.3% Y/Y VS MEDIAN +6.5% Y/Y: CUSTOMS

Oct-13 03:06

- CHINA SEP EXPORTS +8.3% Y/Y VS MEDIAN +6.5% Y/Y: CUSTOMS

- CHINA SEP IMPORTS +7.4% Y/Y VS MEDIAN +1.8% Y/Y: CUSTOMS

- CHINA SEP TRADE SURPLUS +$90.45 BLN VS MEDIAN +$98.2 BLN