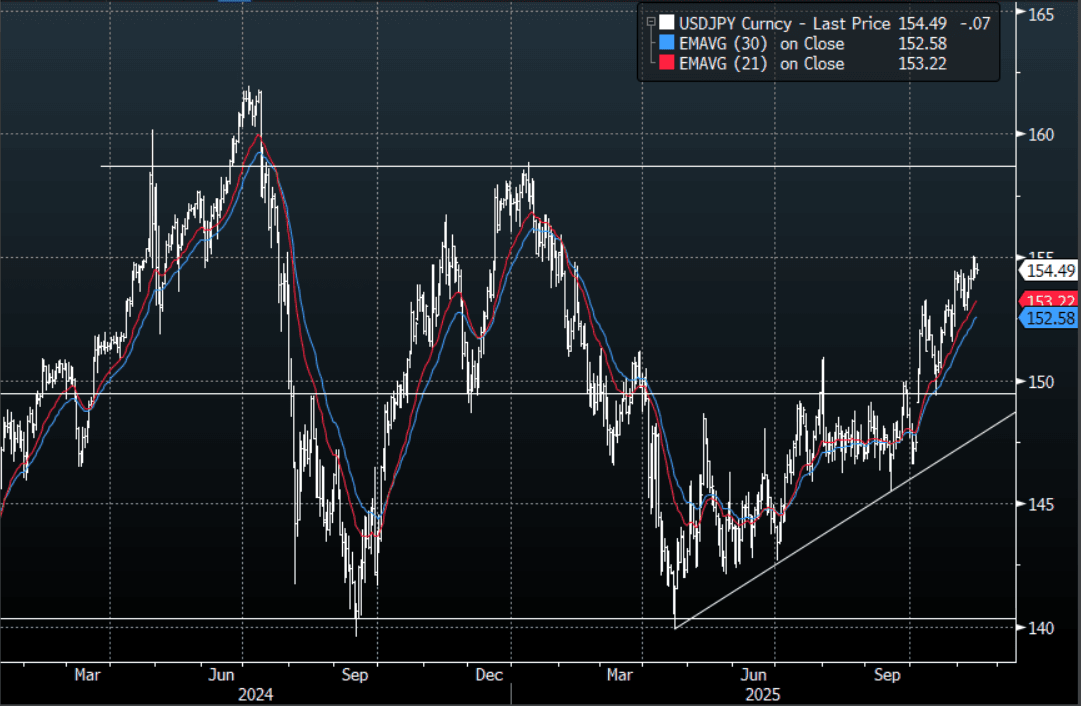

JPY: Asia-Pac: USD/JPY - Drifts Off 154.75 As Yen Bought As A Safe Haven

The USD/JPY range today has been 154.31 - 154.74 in the Asia-Pac session, it is currently trading around 154.45, -0.10%. The pair stalled around the 154.75 area in the Asian session and has drifted lower. Considering the move lower in risk USD/JPY has actually held up ok, probably because the market is starting to question another US cut in December. The overweight positioning in risk looking for a year-end rally is being squeezed across the board, if this has more to play out then Cross-Yen will experience headwinds and the demand for Yen in the crosses should keep the 155.00 area heavy for now. On the day I would be skewed towards looking for some sort of a retracement lower. A sustained break above 155.00 though and the market will start getting excited for another push toward 160.

- "JAPAN PRIME MINISTER TAKAICHI: HARD TO SET NUMERICAL TARGET FOR MINIMUM WAGE NOW, GOVT'S JOB IS TO CREATE ENVIRONMENT THAT ALLOWS FOR FIRMS TO OFFER PAY THAT EXCEEDS PACE OF INFLATION - [RTRS]"

- "JAPAN FINANCE MINISTER KATAYAMA: PLANNED ECONOMIC STIMULUS WILL BE IN LINE WITH TAKAICHI ADMINISTRATION'S PROACTIVE FISCAL POLICY, WHEN ASKED ABOUT SIZE OF STIMULUS - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 155.00($978m Nov17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Fresh Low For 2yr Swap, RBNZ's Conway - Open To Further Easing

NZGB yield losses have extended as the Wednesday session had unfolded, supported by lower US Tsy yields (the 10yr Tsy eyeing a fresh test of 4.00% on the downside is a focus point). We are around 4.5-7bps lower across the NZGB benchmarks, with the back end leading slightly. The 2yr bond is at 2.55%, while 10yr is at 4.02%, close to a 4.00% test. The NZ 2/10s curve is little changed at +147bps. 2yr swap rates are at fresh cycle lows of 2.32%. Downside focus will rest on a move under 2.25% (levels last seen in early 2022)

- The NZ-US 10yr spread is trending lower, albeit little changed today near +2bps. The bias is likely to remain for NZGB yields to see greater downside relative to the US and Australia, but focus will be on whether US Tsy yield losses accelerate if we can sustain a break under 4.00% for the 10yr.

- The RBNZ's Chief Economist spoke earlier. He reiterated that the MPC is open to further easing dependent on the data. While inflation is expected to moderate to 2% in 2026, Conway said it was “nerve-racking” that it was close to the top of the band. Q3 CPI prints on 20 October.

- A 25bps cut is just about fully priced for the Nov meeting, which would take the policy rate to 2.25%. Into 2026 market pricing is at 2.09% for the July meeting.

GOLD: Fed Easing Signals & Trade Tensions Push Bullion Even Higher

Gold has rallied again today with it reaching another new high at $4190.97/oz. It is up 1.1% at $4188.3 so far driven by Fed Chair Powell signalling that rates are likely to be cut again on 29 October, which had been almost fully priced in, due to the softer labour market and less concern regarding rising inflation. His comments have also pressured the US dollar (BBDXY -0.2%) and US yields lower. Another 25bp is priced in for the December decision.

- US-China trade tensions continue to provide support even though talks are taking place. Tuesday China imposed curbs on 5 US units of Korea’s Hanwha shipbuilder and today President Trump threatened to halt cooking oil trade with China.

- Bullion has momentum despite it now flashing overbought. It is above initial support at $4179.7, Tuesday’s intraday high, opening round number resistance at $4200.0.

- Silver has unwound a large share of Tuesday’s losses with the metal up 1.4% to $52.17 today after a high of $52.221, holding below resistance at $52.386. It began to correct yesterday on expectations of the London market normalising in coming weeks after liquidity issues.

- Silver is also nervous about US import duties if a review finds that it is a critical mineral.

- Risk appetite has improved with stronger equities and AUD. The S&P e-mini is up 0.2%, Hang Seng +1.3% but CSI 300 flat. Oil prices are slightly lower with WTI -0.2% to $58.60/bbl. Copper is down 0.2%.

- Later the Fed’s Miran, Waller and Schmid speak and the Beige book is released. The ECB’s de Guindos, Buch and Donnery, and BoE’s Breeden and Ramsden also appear. US October Empire manufacturing and August euro area IP print.

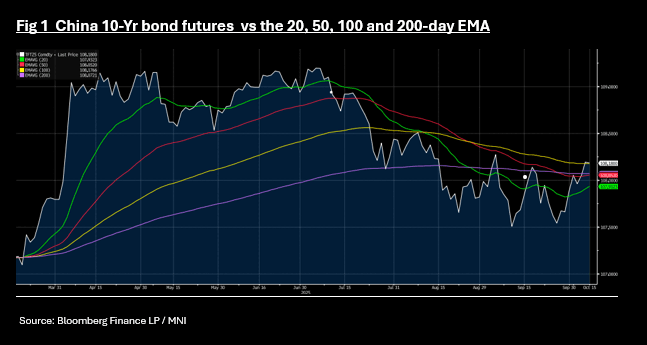

CHINA: Bond Futures Muted on Small Liquidity Injections

- China bond futures have done very little today following a second consecutive day of modest liquidity provision during the morning's open market operations.

- The 10-Yr future is down -0.01 at 108.18 as it remains near to the 100-day EMA

- The 2-YR future is down -0.02 at 102.36 to move back below the 20-day EMA of 102.37

- The bond market continues to grind lower in yield with the CGB 10-Yr back at near term lows of 1.83%. It has traded in a tight range of 1.80% - 1.90% for some months, looking for a catalyst to break out. Equity strength and significant regional and central government bond issuance has not put upward pressure on yields despite the PBOC purchase program remaining on hold.

- Next week's GDP may shed light on the next steps for policy, particularly should forecasts prove correct with a moderation in 3Q from 2Q