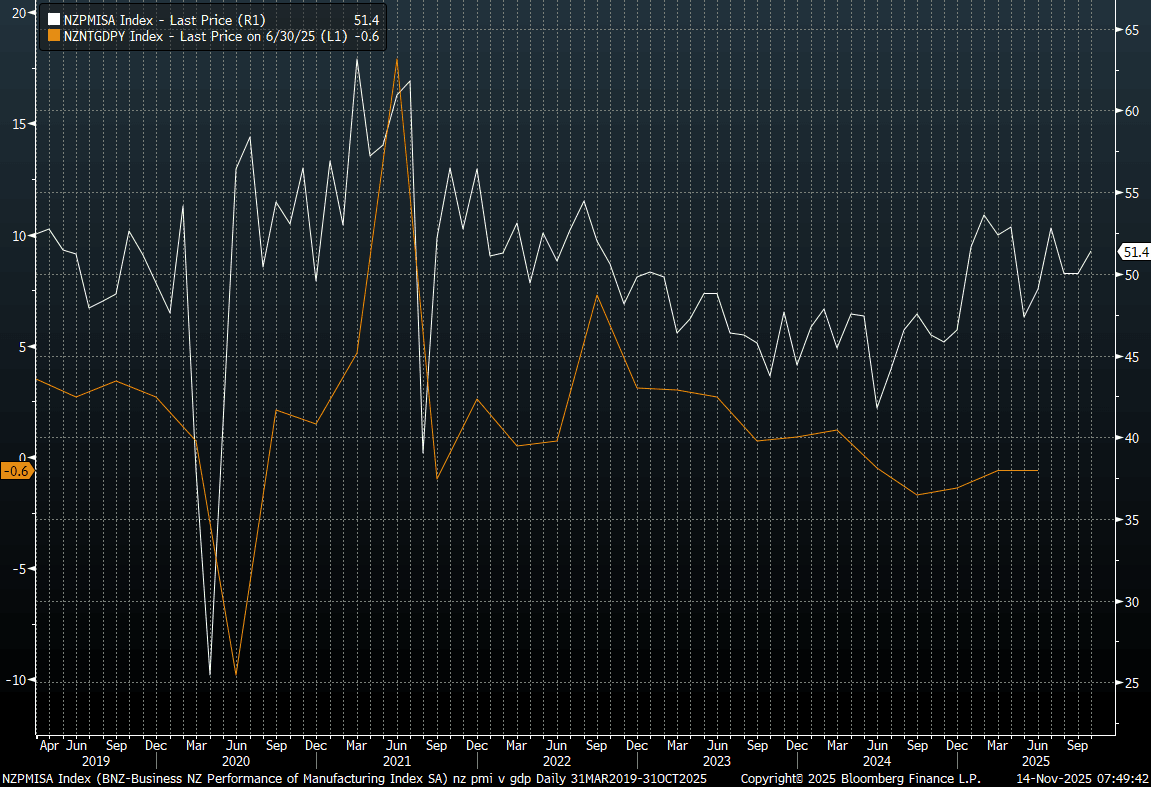

NEW ZEALAND: PMI Rise Points To Recovery, But Index Short Of 2025 Highs

New Zealand's BusinessNZ Manufacturing PMI rose to 51.4 in Oct, from a revised 50.1 outcome in Sep (originally reported as 49.9). The index has been above the 50.0 benchmark since July of this year, but we remain sub earlier 2025 cycle highs (53.6 recorded in Feb), see the chart below. The other line on the chart is NZ y/y GDP growth. We don't get Q3 GDP until Dec 18. Given the y/y decline in Q3 last year was -1.7%, base effects should help y/y momentum for Q3 this year, but broader evidence around the economic recovery remains patchy.

- In terms of the PMI detail, production rose to 52.0, from 50.5, while employment edged up to 48.1 from 47.7. We haven't been in expansion for this sub index since April.

- New orders bounced to 54.9, from 50.5, an encouraging sign, but this just takes us back to where we were in August for this index.

Fig 1: New Manufacturing PMI & GDP Y/Y

Source: BusinessNZ/BNZ/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (Z5) Strong Start to Week

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.685 - 1.000 proj of the Sep 3 - 12 - 15 price swing

- RES 1: 96.615 - High Sep 12

- PRICE: 96.505 @ 16:24 BST Oct 14

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Aussie 3-yr futures surged on the resumption of trade after the weekend, returning focus higher after the break of support last week. While prices appear more stable, the recent break of Sep 3 low of 96.435 negates the recent short-term bullish theme. This breach signals scope for an extension towards 96.280, the May 15 low on the continuation chart. The short-term resistance to watch is 96.615, the Sep 12 high. Clearance of this level is required to reinstate a bullish theme.

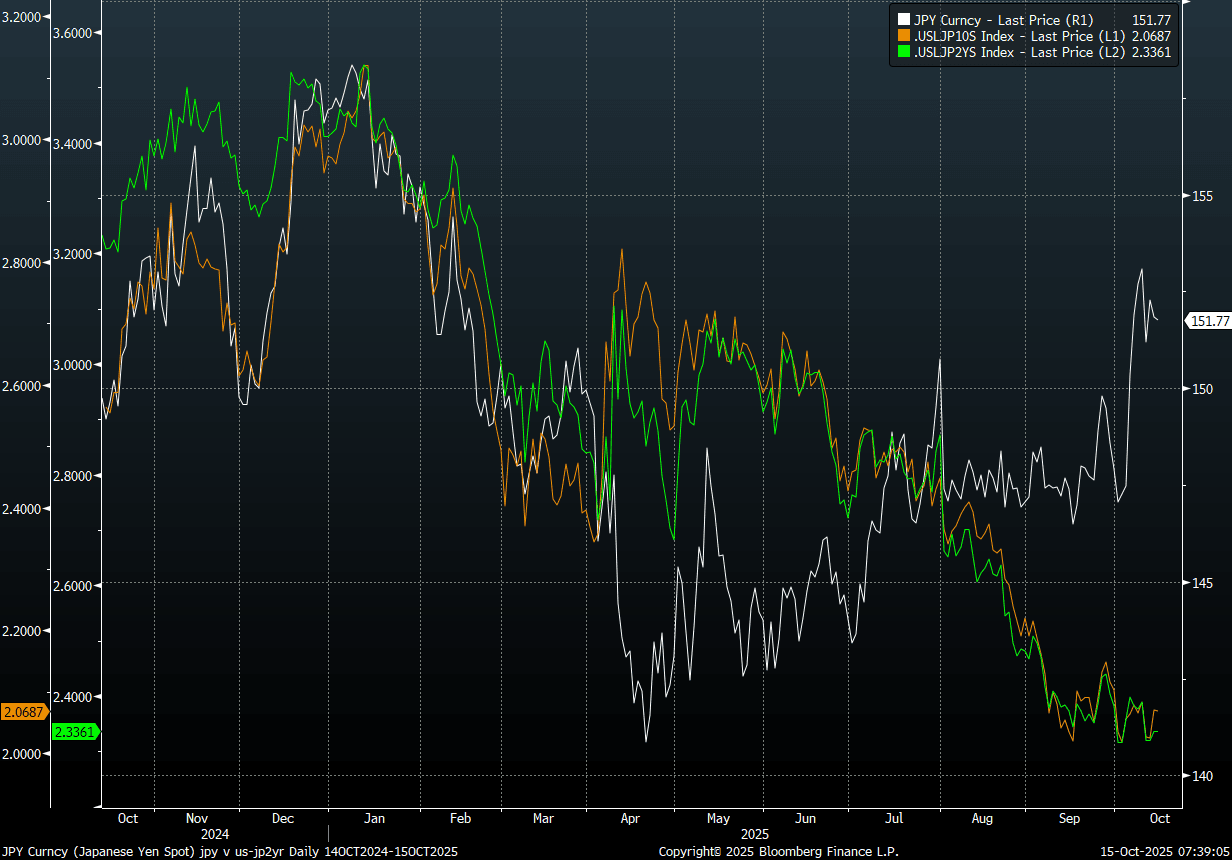

JPY: USD/JPY Bullish Set Up Remains, Takaichi Seeking Meeting With Oppo Parties

USD/JPY tracks under 152.00 in early Wednesday dealings, after posting a modest gain for Tuesday's session. Bullish technical conditions persist, with the recent correction lower considered corrective for now. The next important support lies at 149.72, the 20-day EMA. On the upside, clearance of last Friday’s 153.27 high, would resume the uptrend and open 154.39, a Fibonacci retracement point.

- This backdrop didn't shift as Tuesday's session unfolded, with focus elsewhere, as EUR recovered some ground, while AUD/USD moved up from lows as the USTR said US-China talks were still continuing. AUD/JPY is near 98.40 in latest dealings, remaining supported on dips sub 98.00 for now.

- Despite the bullish technical set up, more broadly, USD/JPY looks too high relative to US-JP yield differentials, see the chart below. Fed Chair Powell largely maintained status quo in terms of signaling another 25bp rate cut at the end of October, without a significant market reaction. Intervention risks also lurk in the background for USD/JPY.

- Some offset is coming from continued domestic political uncertainty. The chairpersons of the House of Councillors' Diet Affairs Committees from the governing Liberal Democratic Party (LDP) and main opposition Constitutional Democratic Party (CDP) met yesterday and agreed on the convening of an extraordinary session of the National Diet on 21 October (likely to elect a new PM). LDP leader Takaichi is seeking meetings with the three main opposition parties today (see this link).

- On the data front today we have Aug final IP, while a 20yr debt auction is in focus on the JGB side.

- In the option expiry space, note the following for NY cut later: Y143.00($1.8bln), Y150.00($1.1bln), Y151.55($956mln), Y151.95-00($500mln).

Fig 1: USD/JPY Versus US-JP Yield Differentials

Source: Bloomberg Finance L.P./MNI

ASIA: Government Bond Issuance Today

- Bank of Korea to Sell KRW700bn 1-Year Bonds

- Vietnam To Sell VND 0.5Tln 2055 Bonds; (TD2555052)

- Vietnam To Sell VND 1.5Tln 2040 Bonds; (TD2540037)

- Vietnam To Sell VND 8.0Tln 2035 Bonds; (TD2535024)

- Vietnam To Sell VND 3.0Tln 2030 Bonds; (TD2530010)

- Thailand to Sell THB30bn of New 2029 Bonds

- Bank Indonesia to Sell 95D SUVBI Bills

- Bank Indonesia to Sell 367D SUVBI Bills

- Bank Indonesia to Sell 182D SUVBI Bills

- Bank Indonesia to Sell 31D SUVBI Bills

- Bank Indonesia to Sell 273D SUVBI Bills

- Thailand to Sell THB15bn of 2040 Bonds

- Singapore to Sell S$5.8 Billion 364-Day Bills

- India to Sell INR60bn 364-Day Bills

- India to Sell INR70bn 91-Day Bills

- India to Sell INR60bn 182-Day Bills