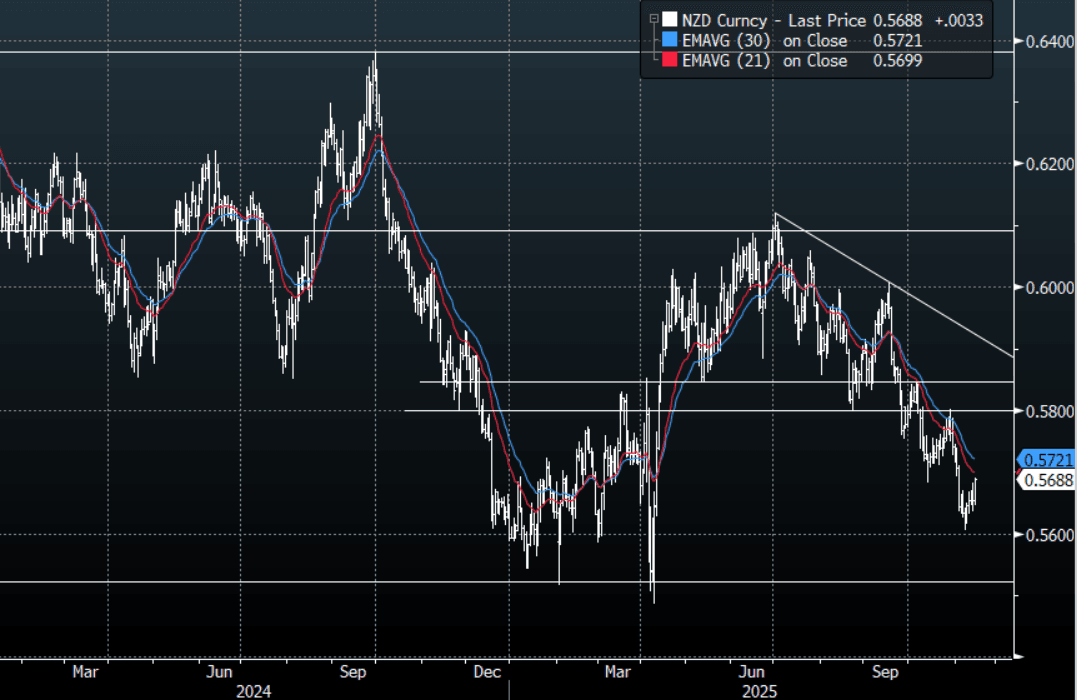

NZD: Asia-Pac: NZD/USD Retraces Overnight losses

The NZD/USD had a range today of 0.5645 - 0.5687 in the Asia-Pac session, going into the London open trading around 0.5685, +0.55%. The NZD has ignored the global woes and retraced all its losses and even breaking the overnight highs, reacting to local inputs. The NZD does stand out as a vehicle to express a short, and if this washout in risk expands it should again be a market favourite. This morning's move could be pointing to positioning with everyone bearish. On the day though should the move in risk build on this correction in the US session I would be skewed to play from the short-side, a move back below 0.5630-40 could see the downtrend reinstated. This would see the focus once again return back toward the 0.5500 lows. Next resistance now back toward the 0.5750 area.

- The Reserve Bank of New Zealand will ease mortgage loan-to-value restrictions, effective Dec. 1, according to a statement. RBNZ will continue to closely monitor housing-related risks and impact of changes.

- MNI AU - PMI Rise Points To Recovery, But Index Short Of 2025 Highs: New Zealand's BusinessNZ Manufacturing PMI rose to 51.4 in Oct, from a revised 50.1 outcome in Sep (originally reported as 49.9). The index has been above the 50.0 benchmark since July of this year, but we remain sub earlier 2025 cycle highs (53.6 recorded in Feb). We don't get Q3 GDP until Dec 18. Given the y/y decline in Q3 last year was -1.7%, base effects should help y/y momentum for Q3 this year, but broader evidence around the economic recovery remains patchy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5730(NZD308m Nov 19), 0.5835(NZD300m Nov19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: 10y Futures Near Key Resistance, AU 3/10s Curve Flattest Since Apr

Aussie bond futures are mixed, with the 10yr (XM) biased higher, aided by US Tsy futures moves (the US Tsy yield is threatening a downside test of 4.00%). We were last 96.77, +2bps, with earlier highs at 95.78, which is key short term resistance (multiple Sep highs). 3yr futures (YM) are down slightly, last 96.52.

- ACGB yields are mixed, slightly firmer at the front end, 3yr at 3.46%, while the 10yr is off close to 2bps last 4.21%. This leaves the 3/10s slightly flatter at +75bps. The AU-US 10yr spread has been relatively steady last +21bps.

- The RBA's Hunter said today that the RBA is looking to keep inflation close to the current rate which is around 2.6/2.7% for the trimmed mean. Her commentary on recent economic developments was consistent with the 30 September meeting minutes. There was nothing to suggest thinking for the 4 November decision. The Board remains flexible and highly data dependent.

- Market pricing for the Nov RBA meeting remains quite steady, last around 3.49%, against an effective policy rate of 3.60%.

- The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months.

- Note tomorrow we get Sep jobs data for Australia. The market expects a +20k rise, versus -5.4k prior. The unemployment rate is forecast to tick up to 4.3% from 4.2%.

ASIA STOCKS: New All Time Highs for KOSPI on Regional Rally

A strong day for regional equities with the KOSPI reaching new highs and the NIKKEI nearing recent new highs. As the FED Reserve hinted that the two rate cuts expected remained a possibility markets were buoyed as regional currencies rallied along with most bond markets. The FED's actions typically lead others in the region, opening up the possibility for further cuts. The next major Central Bank meeting is the Bank Indonesia next week where concerns are rising as to the new FinMin could try to influence policy. The deflationary problem facing the Chinese economy was in full view today with the release of the September CPI and PPI, with both remaining negative. The CPI at -0.3% missed estimates of -0.2% as one of the longest streak of price declines in decades continues.

- The NIKKEI's rally of +1.15% along with the KOSPI's rally of +2.05% sees both indexes maintain their position north of all major moving averages.

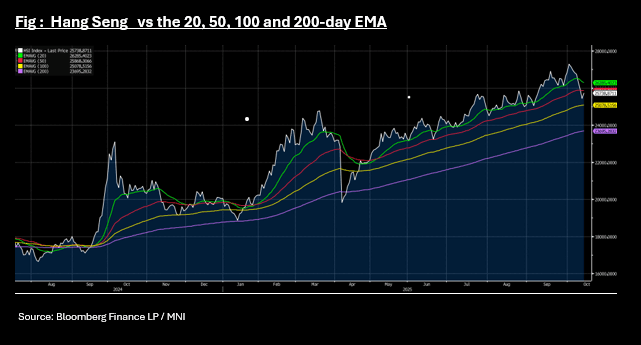

- The HSI in Hong Kong has bounced today to be up +1.15% and near to the 50-day EMA. The weakness in recent days following the US trade moves sees the Hang Seng back below the 20-day and 50-day EMA for the first time since April yet with most major moving averages remaining upward sloping, indications are that the bullish momentum could return.

- Taiwan's TAIEX is up over 300pts today as it nears the recent new high on October 9th. Taiwan’s biggest life insurance company Cathay Life plans to shift over NT$7 trillion ($228 billion) in investment mandates to its parent group’s asset management arm as part of a push to make the island’s money management industry regionally competitive and a move seen supportive of domestic equities.

BONDS: NZGBS: Fresh Low For 2yr Swap, RBNZ's Conway - Open To Further Easing

NZGB yield losses have extended as the Wednesday session had unfolded, supported by lower US Tsy yields (the 10yr Tsy eyeing a fresh test of 4.00% on the downside is a focus point). We are around 4.5-7bps lower across the NZGB benchmarks, with the back end leading slightly. The 2yr bond is at 2.55%, while 10yr is at 4.02%, close to a 4.00% test. The NZ 2/10s curve is little changed at +147bps. 2yr swap rates are at fresh cycle lows of 2.32%. Downside focus will rest on a move under 2.25% (levels last seen in early 2022)

- The NZ-US 10yr spread is trending lower, albeit little changed today near +2bps. The bias is likely to remain for NZGB yields to see greater downside relative to the US and Australia, but focus will be on whether US Tsy yield losses accelerate if we can sustain a break under 4.00% for the 10yr.

- The RBNZ's Chief Economist spoke earlier. He reiterated that the MPC is open to further easing dependent on the data. While inflation is expected to moderate to 2% in 2026, Conway said it was “nerve-racking” that it was close to the top of the band. Q3 CPI prints on 20 October.

- A 25bps cut is just about fully priced for the Nov meeting, which would take the policy rate to 2.25%. Into 2026 market pricing is at 2.09% for the July meeting.