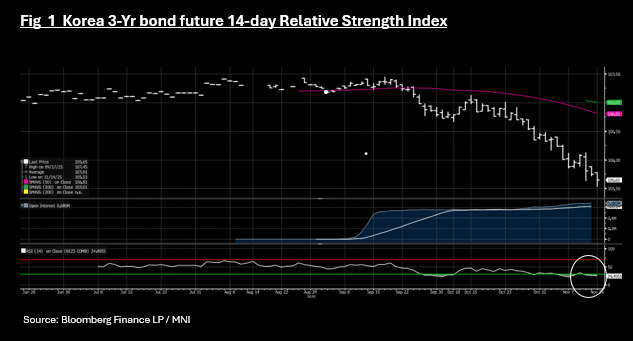

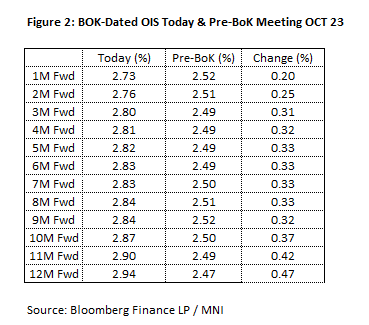

SOUTH KOREA: Bond Market Down Heavily Again, Rate Rises in Play

- The move in Korean bonds this week has been fierce, with bond futures gapping lower again today and KTB yields hitting new highs for the year whilst the move in IRS sees rate rises coming into reckoning.

- The move lower in the 10-Yr bond future takes the contract to 113.76, and oversold on the 14-day relative strength index and down almost 100pts this week alone.

- The 3-Yr future is down -0.10 to 105.65, a new contract low as it moves further into being oversold on the 14-day RSI

- Cash have been hit hard with yield 3-5.5bps higher across the curve. The 10-Yr is at 3.32%, the first time it has been above 3.30% since June 2024.

- Swap markets have re-priced the rate trajectory, with not only all cuts now removed partial rate hikes are priced further out the curve with the 12mth FWD pricing in almost a full rate hike.

- BBG's MIPR function now has +9bps of rate rises priced in over a 1-Yr time horizon.

The governor's comments this week hasn't calmed markets instead markets have focused on key words which was interpreted as rates on hold for a long time, whilst keeping the easing bias. For now the bias is being ignored and the market is pushing hard on the BOK who meet again on November 27. Until then, the pressure on bond yields could provide an interesting input into monetary policy thinking for the committee members.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: New Zealand AA+ Rating Affirmed By S&P

Headlines have crossed from S&P that it has affirmed NZ's credit rating at AA+, with the outlook remaining stable. The rating agency noted, via BBG: "S&P sees New Zealand to gradually consolidate its fiscal deficit over the next three years."

- S&P noted the economic challenges from a growth standpoint NZ has face in recent years, but also commented on the structural improvement in the current account position.

- NZ Finance Minister Willis stated recently a return to surplus was still the government's goal (by 2028) and that fresh fiscal spending/stimulus is not needed for the economy (despite current headwinds).

JPY: USD/JPY Under Fri Lows As US 10yr Eyes 4.00% Test, Key EMAs Under 150.00

USD/JPY is continuing to track lower, now under 151.15, up 0.50% in yen terms. This puts us under Friday lows in the pair, but we are still comfortably above key EMAs.

- Focus in the near term may rest on the softer US Tsy yield backdrop. The 10yr at 4.01% is close to recent lows, with eyes on whether we can break under the 4.00% handle. As we noted earlier USD/JPY looks too high relative to yield momentum between US-JP. The USD/CNY fix under 7.1000 has been another positive, while other cross asset trends have been mixed. Gold continues to rally, signifying some safe haven flows are still on-going, but the regional equity mood looks better.

- JPY is outperforming so far in the G10 space, although AUD isn't too far behind, up 0.30% (with similar benefits from the CNY fixing outcome).

- For USD/JPY we are now under late Friday highs, while other support points to note are outlined below. We are still some distance from the 50-day EMA.

- SUP 1: 150.92 High Sep 26

- SUP 2: 149.72 20-day EMA

- SUP 3: 148.50 50-day EMA.

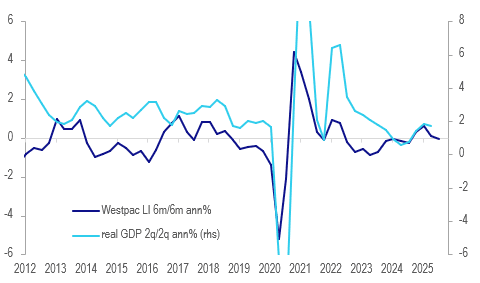

AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months. This measure leads detrended growth by 3 to 9 months and signals that growth may slow in H2 but be around trend early in 2026. Westpac is forecasting 2% growth in 2025 with it improving in 2026.

- Westpac forecast a 25bp rate cut at the November meeting but now believes that while the next move in rates is down, the upcoming decision will rely on Q3 CPI on 29 October. It notes though that its lead indicator signals GDP growth remains lacklustre.

- The indicator was stronger in H1 this year with the H2 moderation driven by dwelling approvals and AUD commodity prices. Westpac expects both of these components to turn with the latter already higher driven by gold and lower rates and policy likely to boost housing supply.

- Equity prices have been positive for the lead indicator over the last 6 months.

Australia Westpac lead indicator vs GDP %