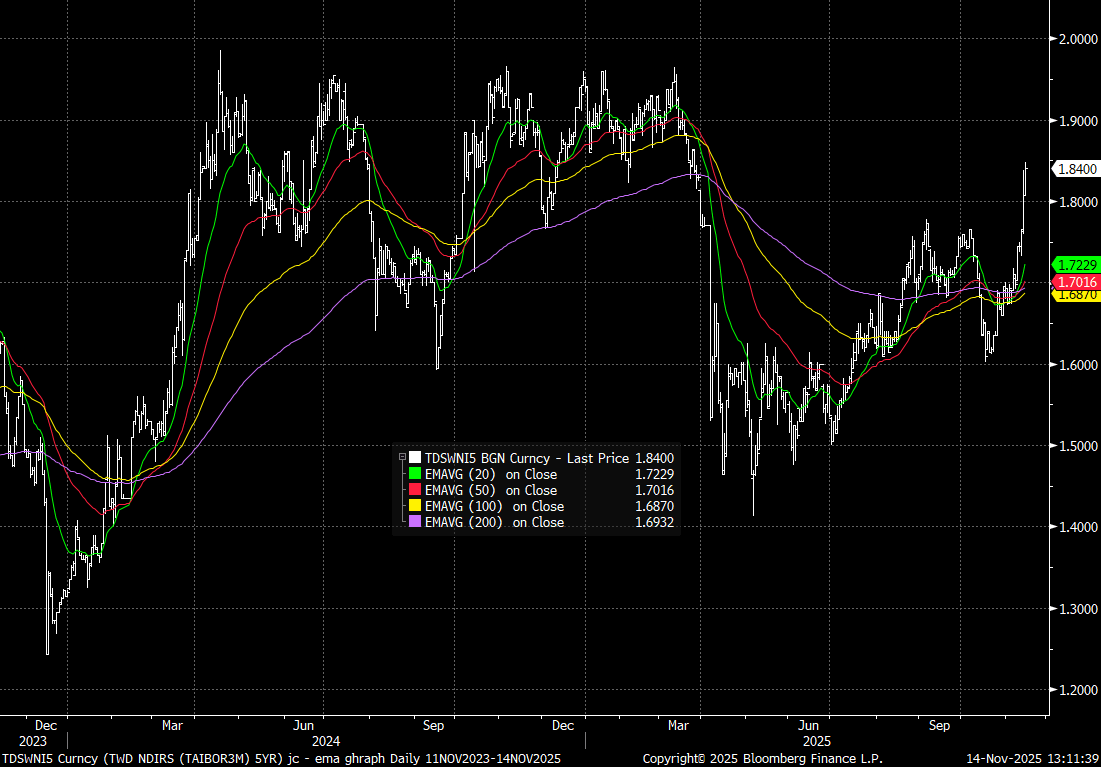

TAIWAN: 5yr NDIRS Surges, As Rate Cut Expectations Erode, TWD Still Weaker

Taiwan's 5yr NDIRS rate has surged higher in recent sessions, last near 1.84%, after starting the week closer to 1.70%. Upside focus is likely to rest around the 1.90-1.95% area, which marked highs in the first part of the year (see the chart below). As we noted earlier in the week, risks were skewed towards steadier policy rate settings in the near term, reflecting a host of factors (including spill over from higher China inflation pressures) (see this link). We saw risks of higher short term rates, with Taiwan likely seeing spilling in recent sessions, via BBG: "“Hedge funds unwound positions after paring back expectations for rate cuts in Asian markets, driving IRS rates higher,” said Henry Lin, an IRS trader at SinoPac Securities".

- The upside projections for Taiwan 2025 GDP growth (with the government noting GDP growth should exceed 5.5% earlier this week), is another factor, although growth projections from the sell-side have been steadily rising in recent months. US and Taiwan officials have also been noting progress in terms of trade talks.

- These rate moves aren't doing much for TWD FX though, which remains weaker, last near 31.125 for USD/TWD, fresh highs back to the start of May this year.

- Equity markets are under pressure amid global tech headwinds, while offshore investors have sold over $1bn of local stocks so far this week. The flagship equity for chipmaking in Taiwan TSMC touched all time highs earlier this month. It is now down almost 5% from those highs on profit taking falling six out of the nine days post the highs.

Fig 1: Taiwan 5yr NDIRS To Fresh Multi Month Highs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Steady As 20yr Auction Results Due, Oct JGB Demand Firm

JGB futures are little changed at 136.31, -.02 versus settlement levels as markets await the 20yr JGB auction result, due in around 30mins. The last 20yr auction, back on Sep 17 went reasonably well with a bid to cover ratio of 3.997 (versus the prior 3.085 outcome). Since the start of Oct, the 10yr and 30yr auction results haven't disappointed the market from a demand standpoint.

- The 20yr bond yield, like other parts of the back end of the curve, spiked after Takaichi was voted as the new LDP leader. However, from highs of 2.75% we have since stabilized, last around 2.70%.

- Political uncertainty continues around who will be the new PM, with headlines crossing a short while ago that the parliamentary committee has failed to agree to hold the new PM election on Oct 21 (which was speculated on yesterday).

- Still the upshot of there is unlikely to be strong fresh fiscal stimulus (and thereby JGB issuance in the near term). Via BBG: "The 20-year auction is expected to go smoothly, supported by the high yield level and the bond’s relative cheapness, he says (Katsutoshi Inadome, senior strategist at Sumitomo Mitsui Trust Asset Management Co.)".

- BBG noted: "*JAPAN 20Y GOVT BOND AUCTION MAY HAVE 100.20 LOWEST PRICE:POLL" - BBG".

RATINGS: New Zealand AA+ Rating Affirmed By S&P

Headlines have crossed from S&P that it has affirmed NZ's credit rating at AA+, with the outlook remaining stable. The rating agency noted, via BBG: "S&P sees New Zealand to gradually consolidate its fiscal deficit over the next three years."

- S&P noted the economic challenges from a growth standpoint NZ has face in recent years, but also commented on the structural improvement in the current account position.

- NZ Finance Minister Willis stated recently a return to surplus was still the government's goal (by 2028) and that fresh fiscal spending/stimulus is not needed for the economy (despite current headwinds).

JPY: USD/JPY Under Fri Lows As US 10yr Eyes 4.00% Test, Key EMAs Under 150.00

USD/JPY is continuing to track lower, now under 151.15, up 0.50% in yen terms. This puts us under Friday lows in the pair, but we are still comfortably above key EMAs.

- Focus in the near term may rest on the softer US Tsy yield backdrop. The 10yr at 4.01% is close to recent lows, with eyes on whether we can break under the 4.00% handle. As we noted earlier USD/JPY looks too high relative to yield momentum between US-JP. The USD/CNY fix under 7.1000 has been another positive, while other cross asset trends have been mixed. Gold continues to rally, signifying some safe haven flows are still on-going, but the regional equity mood looks better.

- JPY is outperforming so far in the G10 space, although AUD isn't too far behind, up 0.30% (with similar benefits from the CNY fixing outcome).

- For USD/JPY we are now under late Friday highs, while other support points to note are outlined below. We are still some distance from the 50-day EMA.

- SUP 1: 150.92 High Sep 26

- SUP 2: 149.72 20-day EMA

- SUP 3: 148.50 50-day EMA.