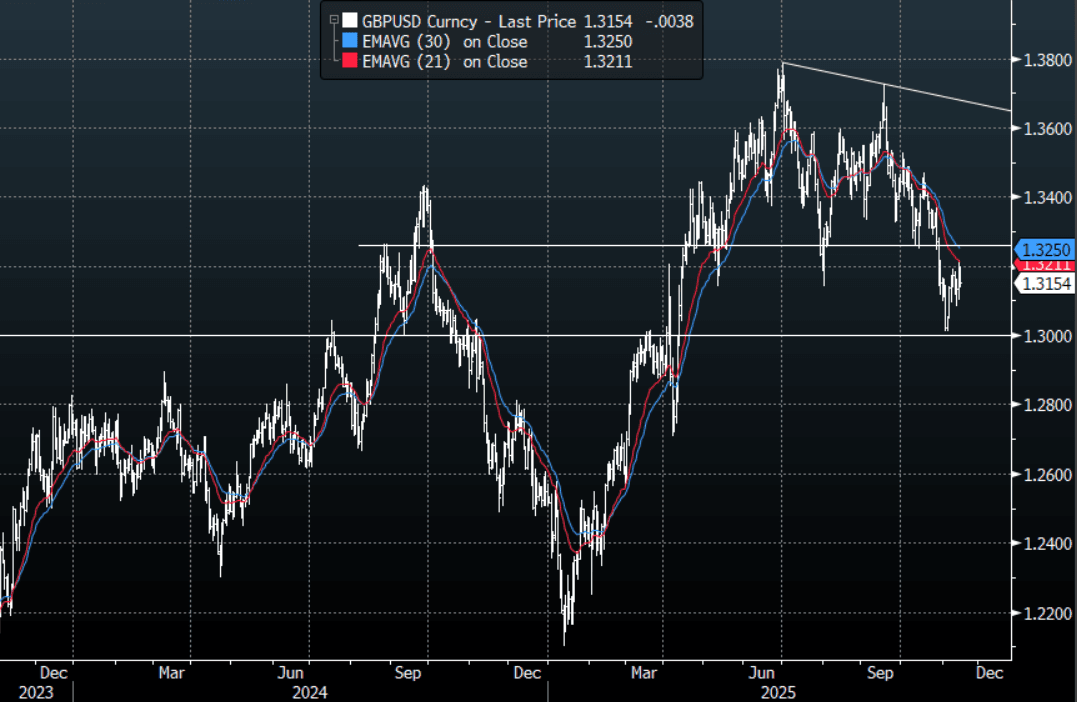

GBPUSD: GBP/USD - Slides Lower After Stalling Above 1.3200 On FT Report

The overnight range was 1.3101 - 1.3213, Asia is currently trading around 131.55, -0.30%. GBP/USD stalled back above the 1.3200 area overnight and for the most part seemed to be ignoring the reversal in global risk sentiment. This morning's FT report that "Starmer and Reeves ditch Budget plan to increase income tax rates", has seen Cable play catch up to the move. Should this squeeze lower in risk expand and force those positioned for the “year-end” rally to pare back then Sterling could come back under some pressure. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I was hoping for a deeper pullback toward the 1.3250-1.3300 area but we never quite got there. If this move lower in risk builds then I suspect rallies on the day back toward 1.3175-1.3200 could be faded, a sustained move back below 1.3080-1.3100 would see the momentum lower reinstated and focus turn back toward the 1.3000 area.

- The GBP/USD Average True Range for the last 10 Trading days: 80 Points

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.3100(GBP330m), 1.2970(GBP638m). Upcoming Close Strikes : 1.3200(GBP407m Nov 19), 1.3250(GBP355m Nov 19) - BBG

Fig 1 : GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Kiwi Softer As RBNZ’s Conway Says OCR At Lower End Of “Neutral”

NZDUSD has dipped today to around 0.5709 following comments from RBNZ chief economist Conway and that he’s “confident” the output gap will close and that rates are towards the bottom end of neutral suggesting that further easing will bring policy into stimulatory territory. At this stage another cut on 26 November looks likely.

- Conway reiterated that rates are “getting toward the lower end” of the neutral range. The RBNZ estimates it to be around 2.5-3.5% and the OCR is currently at 2.5% after October’s 50bp cut. He also repeated that excess capacity should help inflation return to the 2% mid-point of the band.

- His speech was on the policy lessons learned from the pandemic period which included recent research on the effect of Large-Scale Asset Purchases (LSAPs). He stated that “while certainly not perfect, LSAPs need to remain a key part of our additional policy toolkit for targeted interventions during financial and economic crisis when the Official Cash Rate has reached its lower limit.” But additional tools are unlikely to be used anytime soon.

- Kiwi was impacted by generally weaker risk appetite on Tuesday related to US-China trade concerns as China retaliated against the US’ investigation into shipping. NZDUSD fell 0.2% to 0.5716 on Tuesday off the intraday low of 0.5683 helped by comments from US trade representative Greer that staff-level talks with China were taking place increasing hopes of a solution.

- AUDNZD is up 0.2% to 0.1365 so far today driven by the contrast between the RBNZ’s clear easing bias and the RBA’s caution and focus on upside risks in its 30 September meeting minutes. AUDNZD fell to 1.1323 on Tuesday and finished down 0.3% to 1.1349.

CNH: Wedged Between Key EMAs, US-China In Focus, Inflation Data Today

USD/CNH is wedged between key EMAs, last near 7.1415/20 (the 20-day support point is at 7.1370, while on the topside the 50-day resistance is close to 7.1450). Recent highs in the pair have not stretched much beyond 7.1500. Spot USD/CNY ended yesterday at 7.1372.

- Firm market focus remains on US-China relations. Sentiment calmed somewhat as Tuesday's session unfolded (after risk off came post China shipping curbs/investigation). With USTR's Greer confirming that staff-level communications between US and Chinese representatives was underway, helping stabilize sentiment. Greer also stated the meeting between US President Trump and China President XI is still scheduled to take place.

- Still, US President Trump stated, "... he might stop trade in cooking oil with China as retaliation against Beijing for its refusal to buy American soybeans." (via BBG). Chair of the US National Economic Council also stated on FoxNews that the US has lots of leverage over China and that China needs to come to the table to work with the US.

- 1 month implied USD/CNH vol remains near recent highs, last at 3.20%, is still very low by historical standards. The anchored USD/CNY fixing is helping offset concerns from US-China trade tensions.

- Today we get the Sep inflation prints, with CPI expected to remain negative at -0.2%y/y, while PPI is forecast at -2.3y/y (versus -2.9% prior).

- Equity sentiment will also be in focus, with China and Hong Kong markets losing momentum over the past week. The China to global equity ratio has fallen sharply, although this isn't impacting CNH negatively at this stage.

JGBS: Futures Holding Recent Gains But Sub Resistance Levels, 20yr Sale Today

JGB futures finished up post Tokyo trade on Tuesday at 136.41, +.08 versus settlement levels. Like elsewhere the Dec JGB futures is holding the bulk of its gains seen so far this week. This impulsive rally comes in the context of the firm downtrend that’s dominated prices since mid-September, and will need to challenge resistance before signaling a broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. On the downside, note the Oct 8 low at 135.61.

- The bias remains for futures to remain in a downtrend, given fiscal pressures and potential delays to the BoJ tightening cycle (which should bias the JGB curve steeper, all else equal). Still, markets will be mindful that the US 10yr Tsy yield is close to recent lows near 4.00%, so spill over could unfold if this benchmark yield tests lower.

- Domestic politics remains in focus, with uncertainty as to who will be the next PM. An extraordinary session of the National Diet is expected to be held on 21 October (likely to elect a new PM). Per Kyodo news: "There is no indication of when LDP President Sanae Takaichi will receive the nomination, and a series of meetings between the ruling and opposition parties and within the opposition parties are expected to be held in the afternoon of the 15th." LDP leader Takaichi is seeking meetings with the three main opposition parties today. Takaichi's PM odds sit at 80 per Polymarket, slightly up from this week's lows.

- Note we have the 20yr debt sale today. Concerns around a sharp rise in bond issuance may have fallen, given the on-going political uncertainties could leave it difficult to pass aggressive fiscal policy in the near term.

- The 10yr JGB finished up yesterday at 1.65%.