MNI ASIA OPEN: Not so Jolly on Messy Inflation Measures

EXECUTIVE SUMMARY

- MNI US INFLATION: MNI US Inflation Insight: Messy And Misleadingly Soft

- MNI FED: NY's Williams Signals Little "Urgency" For January Cut After Messy Data

- MNI US DATA: Downward NFP Revisions Look On Track For Powell's 60k/Month Estimate

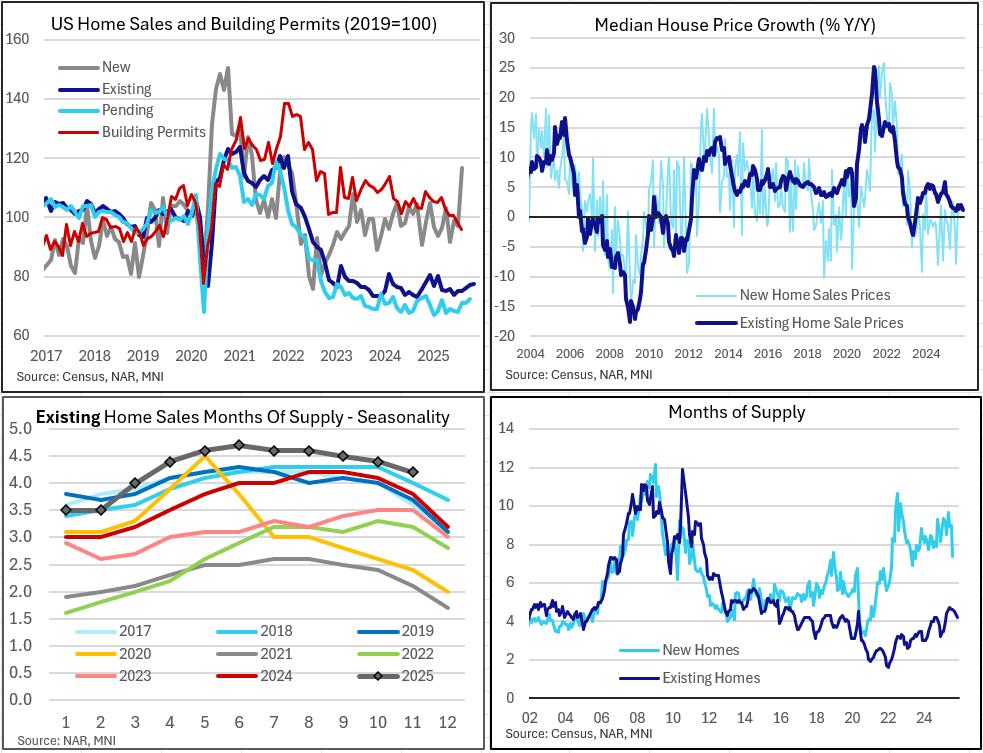

- MNI US DATA: Existing Home Sales Still Soft Despite Modest Upside Momentum

- MNI US DATA: UMich Sentiment Ends Year On Sour Note On Job And Inflation Concerns

US

MNI FED: NY's Williams Signals Little "Urgency" For January Cut After Messy Data

NY Fed President Williams tells CNBC in an interview Friday that the this week's soft CPI print as well as the tickup in the unemployment rate were distorted by technical factors. As such he says that the latest data don't change his view of the outlook: “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

- We would interpret the lack of "sense of urgency" to "act further...right now" as Williams pushing back against prospects of an end-January FOMC rate cut, at least unless there is some significantly dovish development in the data between now and then.

MNI US INFLATION: MNI US Inflation Insight: Messy And Misleadingly Soft

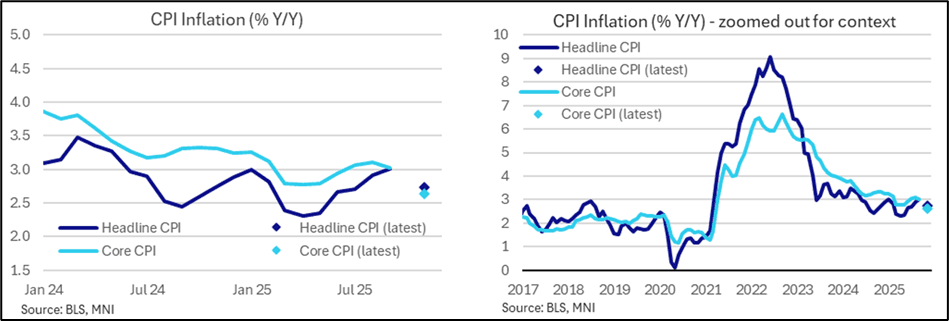

We've just published our review of the latest US CPI data - Download Full Report Here The November CPI report was even messier than had been feared coming into its delayed release, leaving several lingering questions in its wake. On the surface, the inflationary pressures from the report appeared much softer than expected.

- The two-month change in core CPI (Nov vs Sept; the October release was effectively skipped) came in at 0.159% SA, which roughly speaking translates into an 0.08% M/M average for each of Nov and Oct - well below the 0.24% M/M average expected for those two months (and 0.23% M/M in September).

- The average implied monthly change across Oct and Nov for key core CPI items were softer than expected across the board, most notably for housing.

- Headline CPI came in around 0.10% M/M on average in Oct and Nov (2-month rise was 0.20%). Both food and energy inflation softened on an average M/M pace compared with September though dynamics vs expectations varied.

- But the unusual collection period of late November and methodological choices made by BLS appear to have downwardly biased the readings in the report, and look poised to distort readings for months to come.

- This interpretation appears to be borne out by regional Feds’ extremely soft readings across the relevant underlying metrics which were based on the CPI data.

- Fed Chair Powell had warned this month regarding the latest CPI report that “data was not collected in October and half of November. So, we're going to get data, but we're going to have to look at it carefully and with a somewhat skeptical eye.”

- NY Fed President Williams reinforced this notion in downplaying the signal from the data, confirming that the FOMC will interpret these readings with extreme caution, using the December CPI report due out before the January meeting to make more sense of underlying price dynamics.

- Analysts have sharply downwardly revised expectations for core PCE in October and November (and indeed, Y/Y for several months to come) following the CPI report. All acknowledge that the downside surprise to key aggregates was probably driven by serious methodological issues/choices that may reverse to the upside in the coming months.

NEWS

MNI SECURITY: US Secretary Of State Rubio Talks On Ukraine, Venezuela & Gaza

Secretary of State Marco Rubio speaking at an end-of-year press conference (livestream). Regarding the state of talks on a Ukraine-Russia peace plan framework, Rubio claims that "We've made progress but we have a ways to go," adding that "Talks to end the Ukraine war are not about imposing a deal on anybody." Rubio: "What we're trying to figure out is what can Ukraine live with and what can Russia live with...Wars end one of two ways. Surrender by one side to another or a negotiated settlement. We don't see surrender by either side...Only a negotiated settlement gives us the opportunity to end this war."

US TSYS

MNI US TSYS: Tsys Fully Reject Thursday's CPI-Tied Rally, Bund Decline Adds to Move

- Treasuries look to finish weaker Friday, early impetus: Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move following Thursday's ECB decision.

- Treasuries followed Bunds lead in early trade, extending lows as rates fall back towards yesterday's pre-data levels as markets continued to question the delayed/abbreviated Oct/Nov report.

- Currently, TYH6 trades -8 at 112-16 vs. 112-14.5 low, 10Y yield +.0274 at 4.1490%, a deeper pullback would cancel a bull theme and instead refocus on attention on 111-29, the Dec 10 low and a key short-term support.

- NY Fed President Williams tells CNBC in an interview Friday that the this week's soft CPI print as well as the tickup in the unemployment rate were distorted by technical factors. As such he says that the latest data doesn't change his view of the outlook: “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

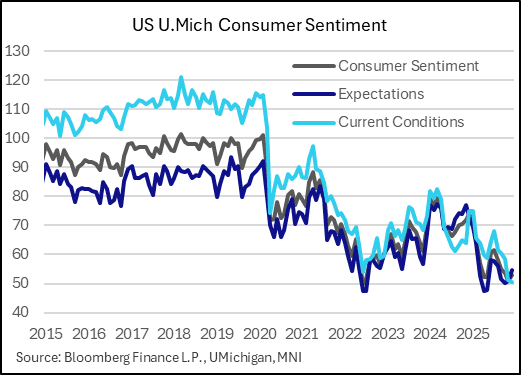

- Consumer sentiment ended the year on a down note, with the final U-Michigan survey for December confirming the weakest current conditions reading in series history. Overall Consumer Sentiment was revised down slightly to 52.9 from 53.3 (51.0 Nov), with Expectations also revised down 0.4 points to 54.6 (51.0 Nov), while Current Conditions at the record low 50.4 (50.7 prelim, 51.1 Nov).

OVERNIGHT DATA

MNI US DATA: UMich Sentiment Ends Year On Sour Note On Job And Inflation Concerns

Consumer sentiment ended the year on a down note, with the final UMichigan survey for December confirming the weakest current conditions reading in series history. Overall Consumer Sentiment was revised down slightly to 52.9 from 53.3 (51.0 Nov), with Expectations also revised down 0.4 points to 54.6 (51.0 Nov), while Current Conditions at the record low 50.4 (50.7 prelim, 51.1 Nov).

- The survey text summarizes the driver as "pocketbook issues continue to dominate consumer views of the economy" - namely inflation, with expectations of higher real income in the next year remaining around series lows and "good conditions" to buy a large household item continuing to decline from already depressed levels.

- Median 12M inflation expectations ticked up in the final (4.2% from 4.1% prelim) with 5-10Y steady at 3.2%, but both represented a decline from Nov (4.5% / 3.4%, respectively).

- But "Despite this softening in the outlook for future inflation, consumers remain strained by the persistence of high prices now. This month, 47% of consumers spontaneously mentioned that their personal finances were weighed down by high prices, unchanged from last month."

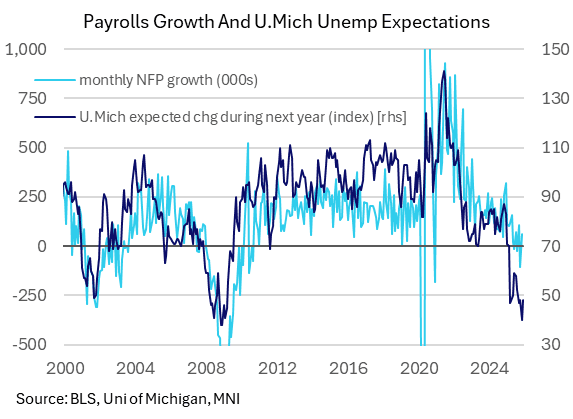

- We also take note that UMich surveys continue to point to deteriorating labor market dynamics; 63% of surveyed consumers expect unemployment to continue rising over the coming year, even though expected probability of job loss over the next 5 years actually fell to the lowest since February.

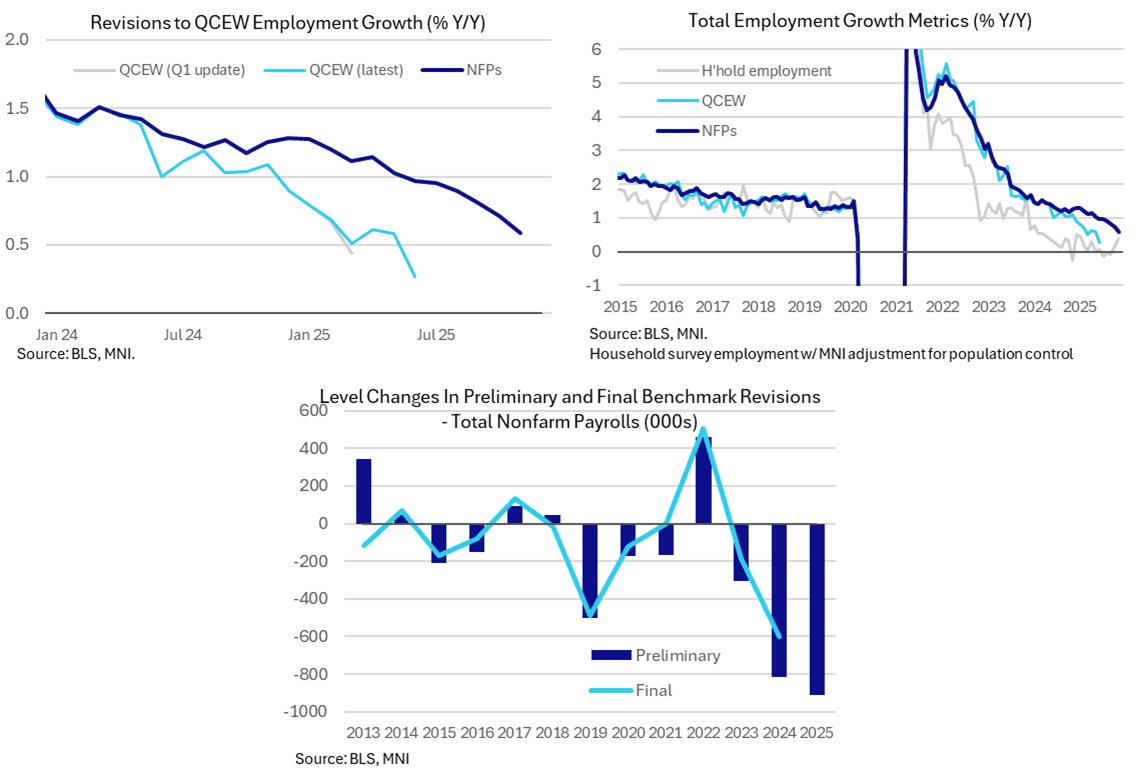

MNI US DATA: Downward NFP Revisions Look On Track For Powell's 60k/Month Estimate

The latest QCEW data for Q2, released at 1000ET, show what we think is confirmation that the benchmark revision for payrolls, due with the January payrolls report, will be less negative than the preliminary estimate pointed to (but still very large). Today’s update shouldn’t surprise the Fed or markets but we’ll revert if we see otherwise.

- There are two areas worth focusing on in today’s Q2 update for QCEW (the far more comprehensive measure of employment than payrolls): revisions to Q1 and latest trends.

- Q1 revisions were positive, with total employment rising 779k in the twelve months to March 2025 (when nonfarm payrolls will be revised to in the Jan 2026 report) vs a 675k increase in the Q1 update.

- Latest nonfarm payrolls data show a 1790k increase over the same period, i.e. they overestimated jobs growth by 1011k vs 1115k with the Q1 QCEW vintage.

- The latter coincided with a preliminary benchmark revision estimate of -911k, which as noted at the time was highly likely to be revised lower come the actual benchmark revision, as is usually the case (see bottom chart).

MNI US DATA: Existing Home Sales Still Soft Despite Modest Upside Momentum

Existing home sales rose in November to the highest since February at 4.27M (seasonally-adjusted, annual rate). That was weaker than the expected 4.15M but up from 4.11M in October and marked a 3rd consecutive sequential increase. Overall existing sales data point to still-soft housing market dynamics amid high mortgage rates, though we continue to await the release of delayed "official" government data on residential investment in recent months.

- In the report, National Association of Realtors' Chief Economist Lawrence Yun attributed the improvement to "lower mortgage rates this autumn" but cautioned that "inventory growth is beginning to stall. With distressed property sales at historic lows and housing wealth at an all-time high, homeowners are in no rush to list their properties during the winter months."

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 181.44 points (0.38%) at 48130.99

S&P E-Mini Future up 55.5 points (0.81%) at 6886.25

Nasdaq up 266.3 points (1.2%) at 23274.45

US 10-Yr yield is up 2.7 bps at 4.149%

US Mar 10-Yr futures are down 8.5/32 at 112-15.5

EURUSD down 0.0003 (-0.03%) at 1.1719

USDJPY up 2.03 (1.31%) at 157.58

WTI Crude Oil (front-month) up $0.51 (0.91%) at $56.66

Gold is up $8.01 (0.18%) at $4340.58

European bourses closing levels:

EuroStoxx 50 up 18.64 points (0.32%) at 5760.35

FTSE 100 up 59.65 points (0.61%) at 9897.42

German DAX up 88.9 points (0.37%) at 24288.4

French CAC 40 up 0.74 points (0.01%) at 8151.38

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +2.588, 53.406 (L: 49.66 / H: 55.087)

2Y10Y +0.611, 66.566 (L: 65.229 / H: 67.617)

2Y30Y +0.406, 134.487 (L: 132.879 / H: 136.271)

5Y30Y -0.465, 113.496 (L: 112.555 / H: 115.526)

Current futures levels:

Mar 2-Yr futures down 1.5/32 at 104-12.625 (L: 104-11.75 / H: 104-14)

Mar 5-Yr futures down 5.25/32 at 109-10.75 (L: 109-10 / H: 109-15.25)

Mar 10-Yr futures down 8.5/32 at 112-15.5 (L: 112-14.5 / H: 112-23)

Mar 30-Yr futures down 14/32 at 115-9 (L: 115-04 / H: 115-21)

Mar Ultra futures down 16/32 at 118-0 (L: 117-25 / H: 118-15)

MNI US 10YR FUTURE TECHS: (H6) Bull Cycle Intact For Now

- RES 4: 113-22+ High Nov 25 and a key resistance

- RES 3: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 2: 113-07 High Dec 3

- RES 1: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- PRICE: 112-17 @ 11:31 GMT Dec 19

- SUP 1: 112-06/111-29 Low Dec 16 / 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

The spike higher in Treasuries Thursday highlights a stronger short-term bullish condition and for now signals scope for a continued retracement of the recent Nov 25 - Dec 10 bear leg. A resumption of gains would open 113-00+, a Fibonacci retracement. Price has pulled back from yesterday’s high, a deeper pullback would cancel a bull theme and instead refocus on attention on 111-29, the Dec 10 low and a key short-term support.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.010 at 96.495

Jun 26 -0.015 at 96.705

Sep 26 -0.015 at 96.860

Dec 26 -0.020 at 96.910

Red Pack (Mar 27-Dec 27) -0.045 to -0.025

Green Pack (Mar 28-Dec 28) -0.045 to -0.04

Blue Pack (Mar 29-Dec 29) -0.04 to -0.04

Gold Pack (Mar 30-Dec 30) -0.04 to -0.035

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (-0.03), volume: $3.273T

- Broad General Collateral Rate (BGCR): 3.63% (-0.03), volume: $1.325T

- Tri-Party General Collateral Rate (TCR): 3.63% (-0.03), volume: $1.300T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $171B

FED Reverse Repo Operation

RRP usage retreats to $3.047B with 12 counterparties this afternoon vs. Thursday's $11.708B. Compares to last Thursday's $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Seal Bear Steepening For The Week

European curves bear steepened Friday to cap modest losses for the week, with Bunds underperforming Gilts.

- A Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move resuming following Thursday's ECB decision.

- Eurosystem sources told MNI's Policy Team that ECB policymakers think the deposit rate is likely to remain on hold for an extended period.

- Yields were also underpinned in afternoon trade as NY Federal Reserve President Williams downplayed any dovish policy implications of the week's major US data.

- 10Y Bund yield held just below the 2.90% level but posted its highest daily close since March.

- In data, the ECB's forward looking wage tracker continues to point to downside pay pressures next year. UK retail sales were on the soft side while UK public finance data was slightly worse than expected (a negative for Gilts).

- The day's move ensured a bear steepening move for the week as a whole: UK 2Y yield +0.6bp/10Y + 0.7bp; Germany 2Y flat/10Y+3.8bp.

- Periphery/semi-core EGB spreads closed a little wider, with OATs underperforming on a failure by the Government to pass its full budget before year-end.

- Next week's holiday-shortened schedule includes final GDP data for the UK and Spain, while we get a few ECB speakers on Monday (Simkus, Vujcic, Kazimir).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at 2.154%, 5-Yr is up 3.8bps at 2.488%, 10-Yr is up 4.5bps at 2.895%, and 30-Yr is up 5.1bps at 3.536%.

- UK: The 2-Yr yield is up 0.8bps at 3.753%, 5-Yr is up 3.4bps at 3.971%, 10-Yr is up 4.3bps at 4.524%, and 30-Yr is up 4.7bps at 5.255%.

- Italian BTP spread up 0.1bps at 69bps / French OAT up 1bps at 71.6bps

MNI FOREX: Friday Focus on Post-BOJ Yen Weakness, DXY Touch Higher on Week

- All the focus in FX markets Friday was on the weaker Yen following the Bank of Japan’s expected rate hike. BOJ Governor Kazuo Ueda laid the groundwork for further interest rate increases after the BOJ’s board decided on a unanimous 25-basis-point hike to the highest level in three decades on Friday, but provided little clue as to timing and stressed that policymakers must examine the impact of higher rates on the economy, inflation and financial conditions.

- USDJPY extended its post US employment squeeze, which was likely exacerbated by short-term positioning dynamics as we approach the holiday period. The path of least resistance remains lower for the Yen, and the limited conviction across the FX space has bolstered the underlying bearish JPY theme.

- As such, USDJPY rose 1.26% on the session and trade around 157.50 as we approach the weekend close. Price action has significantly narrowed the gap to the recent cycle highs at 157.89, the Nov 20 high and a bull trigger. A break of this hurdle would confirm a resumption of the uptrend.

- Late comments from Katayama continued to sound the alarm on excessive one-sided moves in the JPY but has done little to impact intra-day sentiment overall.

- The only other notable mover on Friday was the New Zealand dollar, with NZDUSD extending its moderate reversal lower following dovish leaning remarks from Governor Breman and soft revisions within the latest GPD data. This has helped NZDUSD fall further back below the medium-term pivot of 0.5800, and boosted AUDNZD back towards 1.1500.

- Overall this week, the long-awaited return of tier-one US data did little to move the needle for both fed expectations and the USD. The DXY put in a 0.9787 low post-NFP on Tuesday and has subsequently risen around 0.75%, looking set to post moderate gains on the week.

- In emerging markets, renewed weakness for HUF following the NBH meeting and ongoing struggles for BRL amid mounting political uncertainty in Brazil are notable. MXN maintains its resilient profile in the face of a still dovish-leaning Banxico.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/12/2025 | 0700/0700 | * | Quarterly current account balance | |

| 22/12/2025 | 0700/0700 | *** | GDP Second Estimate | |

| 22/12/2025 | 0900/1000 | ** | PPI | |

| 22/12/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/12/2025 | 1800/1300 | * | US Treasury Auction Result for 2 Year Note |