US TSYS: Tsys Fully Reject Thursday's CPI-Tied Rally, Bund Decline Adds to Move

- Treasuries look to finish weaker Friday, early impetus: Japanese bond selloff overnight after the BOJ's rate hike set a negative tone that was picked up by long-end EGBs in early trade, with the broader German bear steepening move following Thursday's ECB decision.

- Treasuries followed Bunds lead in early trade, extending lows as rates fall back towards yesterday's pre-data levels as markets continued to question the delayed/abbreviated Oct/Nov report.

- Currently, TYH6 trades -8 at 112-16 vs. 112-14.5 low, 10Y yield +.0274 at 4.1490%, a deeper pullback would cancel a bull theme and instead refocus on attention on 111-29, the Dec 10 low and a key short-term support.

- NY Fed President Williams tells CNBC in an interview Friday that the this week's soft CPI print as well as the tickup in the unemployment rate were distorted by technical factors. As such he says that the latest data doesn't change his view of the outlook: “I don’t personally have a sense of urgency to need to act further on monetary policy right now because I think the cuts we’ve made have positioned us really well."

- Consumer sentiment ended the year on a down note, with the final U-Michigan survey for December confirming the weakest current conditions reading in series history. Overall Consumer Sentiment was revised down slightly to 52.9 from 53.3 (51.0 Nov), with Expectations also revised down 0.4 points to 54.6 (51.0 Nov), while Current Conditions at the record low 50.4 (50.7 prelim, 51.1 Nov).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Bearish Threat

- RES 4: 0.6660 High Sep 18

- RES 3: 0.6644 76.4% retracement of the Sep-Oct bear leg

- RES 2: 0.6618 High Oct 29 and a key near-term resistance

- RES 1: 0.6524/6580 20-day EMA / High Nov 13

- PRICE: 0.6452 @ 17:36 GMT Nov 19

- SUP 1: 0.6452 Low Nov 19

- SUP 2: 0.6440 Low Oct 14 and key support

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

Recent weakness in AUDUSD highlights a clear bear threat. This also reinforces a short-term bearish signal on Nov 13 - a shooting star (inverted hammer) candle formation. Note too that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term pivot resistance has been defined at 0.6580, the Nov 13 high. A continued sell-off would expose 0.6440, the Oct 14 low.

FED: FOMC Minutes: Eyeing More Bills On The Balance Sheeet

One of the least contentious aspects of the October FOMC meeting was on the decision to end QT: "almost all participants noted that it was appropriate to conclude the reduction in the Committee's aggregate securities holdings on December 1 or that they could support such a decision." And even those who didn't quite agree with the decision may be those who thought QT should end immediately rather than a month later (Gov Miran said Wednesday that was his preferred outcome).

- A large portion of the October minutes are devoted to a balance sheet management discussion, beginning with the SOMA manager's recommendation that the FOMC consider stopping runoff "soon" amid "recent changes in money market conditions [that] indicated that the level of reserves could be approaching ample". Participants took that advice to heart: "Participants agreed that the recent tightening in money market conditions indicated that it would soon be appropriate to end balance sheet runoff and that reinvestments of principal payments received on agency securities holdings should be directed into Treasury bills."

- We note for future reference that the SOMA manager eyed repo vs IORB and EFFR vs IORB spreads, and some of the peripheral indicators previously flagged by the NY Fed including a rising share of domestic banks borrowing in the Fed funds market, and rising elasticity of repo rates to changes in repo volumes.

- They discussed the future profile of the Fed balance sheet too, and unsurprisingly a majority wanted the composition to reflect Treasuries outstanding, with a majority wanting to see a larger share of Treasury bills than the current miniscule portion - with a notable minority wanting a relatively large TBill proportion: "Most participants favored a long-run composition of the SOMA portfolio that matched the composition of Treasury securities outstanding, indicating that a proportional allocation would provide enough flexibility and may be simpler to communicate. Some participants indicated that they favored a larger-than-proportional share of Treasury bills, citing the benefits of having even greater flexibility than available under a proportional allocation. Various participants noted that it was not necessary to decide on the long-run composition of the SOMA portfolio at this time, as the shift toward a long-run composition would take place over a number of years."

- On that note, "The presentation noted that the current share of Treasury bills in the SOMA portfolio was smaller than the bill share of total Treasury securities outstanding. The staff also noted that if the Committee preferred a SOMA portfolio with a proportional or greater share of Treasury bills relative to total outstanding, policymakers could wait to make that decision because the current share of Treasury bills in the portfolio was small and the monthly amounts of principal payments received on the Federal Reserve's holdings of agency securities that would need to be reinvested once balance sheet runoff stopped were modest."

- And there didn't seem to be too much opposition to buying bills in future: "Some participants indicated that during a transition phase, purchases to reach a larger share of Treasury bills in the SOMA portfolio could reduce the availability of short-term Treasury securities to the private sector and potentially affect market functioning. They thus favored a measured approach to purchasing Treasury bills. A couple of other participants noted the absence of market functioning problems in past episodes when purchases focused on Treasury bills. A number of participants noted that the expected pace of paydowns of agency securities in the near term was around only $15 billion to $20 billion per month, and that redirecting these proceeds into Treasury bills once balance sheet runoff ended likely would not adversely affect market functioning."

- Elsewhere, the FOMC discussed the Standing Repo Facility in fairly noncommittal fashion, with several looking to study central clearing more closely (" almost all noted that the SRF supports the effective implementation and transmission of monetary policy as well as smooth market functioning, and that central clearing of SRF transactions could improve the effectiveness of the facility").

US DATA: ~15% Of Firms Suggest Recent Layoffs Could Be Temporary – Atlanta Fed

The Atlanta Fed’s business survey for November (link) also offers some anecdotal information on the extent to which recent terminations might be temporary, with almost 15% of respondents suggesting that could be the case. Unfortunately, there isn’t a recent example of this special question to compare with.

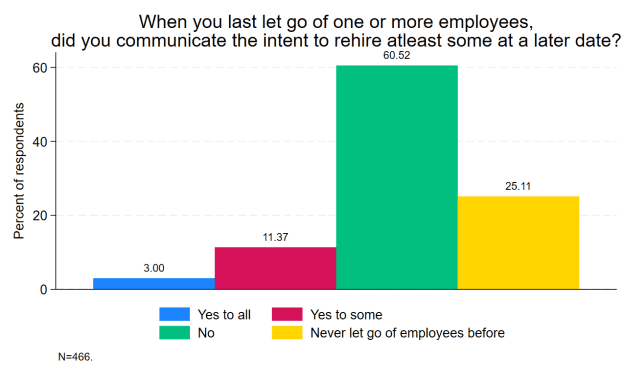

- When asking 466 firms “when you last let go of one or more employees, did you communicate the intent to rehire at least some at a later date”, 61% said no, 11% said yes to some and 3% said yes to all. The remaining 25% of respondents haven’t had to fire anyone.

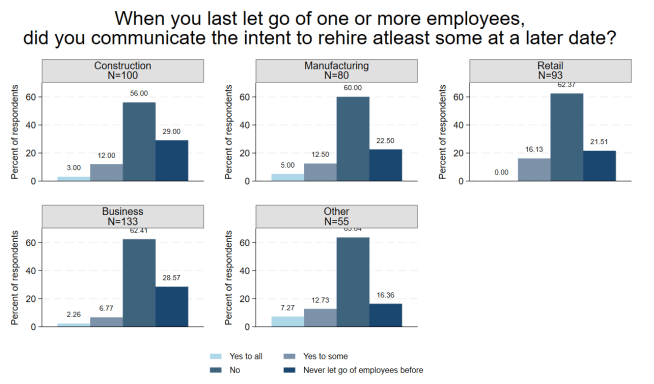

- The usage of temporary layoffs was fairly consistent by firm size: 12% yes to some and 3% yes to all for small firms through to 9% for yes to some and 2% for yes to all for large firms.

- Instead, there was much larger divergence when it came to those who haven’t used layoffs: 30% of small firms haven’t let someone go vs 10% of large firms (with a resulting 54% of small firms not planning to rehire vs 79% for large firms).

- Planned rehiring was lowest for business (finance & insurance) firms whilst retail, manufacturing and construction firms saw similar modest scope for re-hiring when combined over both “yes to all” and “yes to some”. That said, retail saw the lowest share of responses with “yes to all” at 0%.