US DATA: Downward NFP Revisions Look On Track For Powell's 60k/Month Estimate

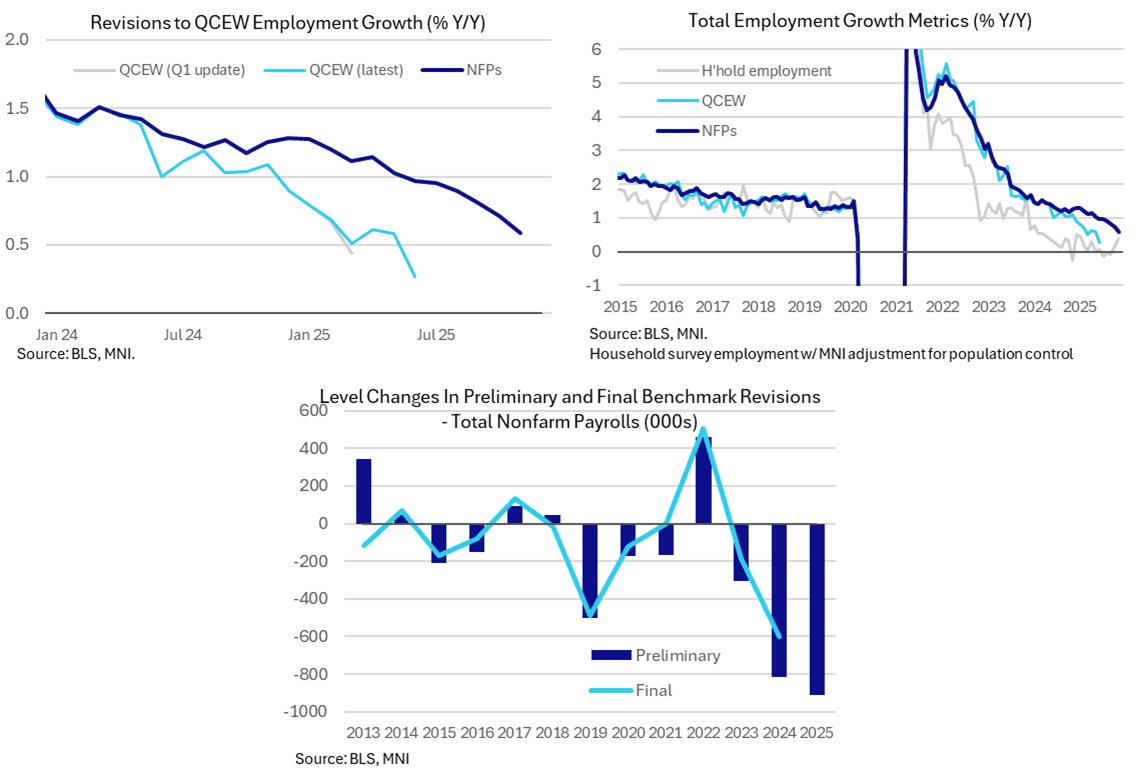

The latest QCEW data for Q2, released at 1000ET, show what we think is confirmation that the benchmark revision for payrolls, due with the January payrolls report, will be less negative than the preliminary estimate pointed to (but still very large). Today’s update shouldn’t surprise the Fed or markets but we’ll revert if we see otherwise.

- There are two areas worth focusing on in today’s Q2 update for QCEW (the far more comprehensive measure of employment than payrolls): revisions to Q1 and latest trends.

- Q1 revisions were positive, with total employment rising 779k in the twelve months to March 2025 (when nonfarm payrolls will be revised to in the Jan 2026 report) vs a 675k increase in the Q1 update.

- Latest nonfarm payrolls data show a 1790k increase over the same period, i.e. they overestimated jobs growth by 1011k vs 1115k with the Q1 QCEW vintage.

- The latter coincided with a preliminary benchmark revision estimate of -911k, which as noted at the time was highly likely to be revised lower come the actual benchmark revision, as is usually the case (see bottom chart).

- We therefore crudely assume - and will keep an eye out for other estimates - that the benchmark estimate is currently tracking more like -815k, or 68k/month vs 76k/month with the preliminary estimate, with a further narrowing in the gap next quarter.

- This shouldn’t be a surprise, with these monthly adjustments walking closer to those by Powell last week at the FOMC press conference (“we think there’s an overstatement […] by about 60k” per month) and Waller again earlier this week (50-60k overestimation, having estimated a 60k overshoot for some time).

- As for latest QCEW data for Q2, it continues to point to softer employment growth than implied by payrolls, up just 0.3% Y/Y in June vs 1.0% Y/Y for nonfarm payrolls at the time. Since then, payrolls growth has slowed to 0.6% Y/Y in November whilst the household survey equivalent was 0.4% Y/Y in November (crudely adjusting for the annual population control).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Steepening Extends, Swap Spreads Sell Off

{GB} GILTS:

- Futures as low as 91.59. Support at 91.82 and 91.67 is breached, strengthening the recent bearish theme. Downside focus moves to Fibonacci support located at 91.12.

- Long end UK swap spreads also extend their narrowing during the move (as noted in recent bullets), indicating increased fiscal & political risk premium in UK paper as PM Starmer’s future as leader of the Labour Party comes under scrutiny.

- Yields 1-7bp higher, curve steepening extends further.

- 10+-Year yields register highest levels seen since Mide October.

- Gilt/Bund spread out widens to 190bp, set for the highest close since October 21.

- Very front end of STIR curves anchored by this morning’s CPI data, which lowered the bar to a Dec cut, while further out the strip is more concerned with fiscal/political risks, resulting in steeper short end curves.

- BoE-dated OIS is 2bp more dovish to 3bp more hawkish on the day, showing 21bp of easing for December, 27bp for February, 35bp for March and 44bp through April.

- SONIA futures little changed to -4.5.

FOREX: Renewed Bid in USD Works Against Major Pairs; GBPUSD Slips

Renewed bid in the USD works further against the major pairs - pressing EURUSD, GBPUSD and others to new daily lows. Vague back-and-forth for risk sentiment remains the primary driver here, particularly with performance in Mag-7 stocks mirroring that of the S&P ahead of the post-market Nvidia earnings (these historically cross at 2120GMT/1620ET).

- GBP is underperforming on the latest leg, helping EURGBP rise back into positive territory on the day, although still below the earlier highs in turn triggered by political uncertainty. As a result, GBPUSD has narrowed the gap with the bear trigger of 1.3010 - a level that may come under pressure on any further signs of Starmer's support fracturing headed into next Wednesday's Budget (and beyond).

- We noted earlier today the elevated front-end of the GBP vol curve: The GBPUSD vol premium over EURUSD has only traded wider on two occasions since the Truss/Kwarteng budget in 2022: January 2025's GBP sell-off, and the BoE's 50bps rate hike in June 2023. This signals broad currency risk into Reeves' Budget - despite more settled expectations of the tax-and-spend measures.

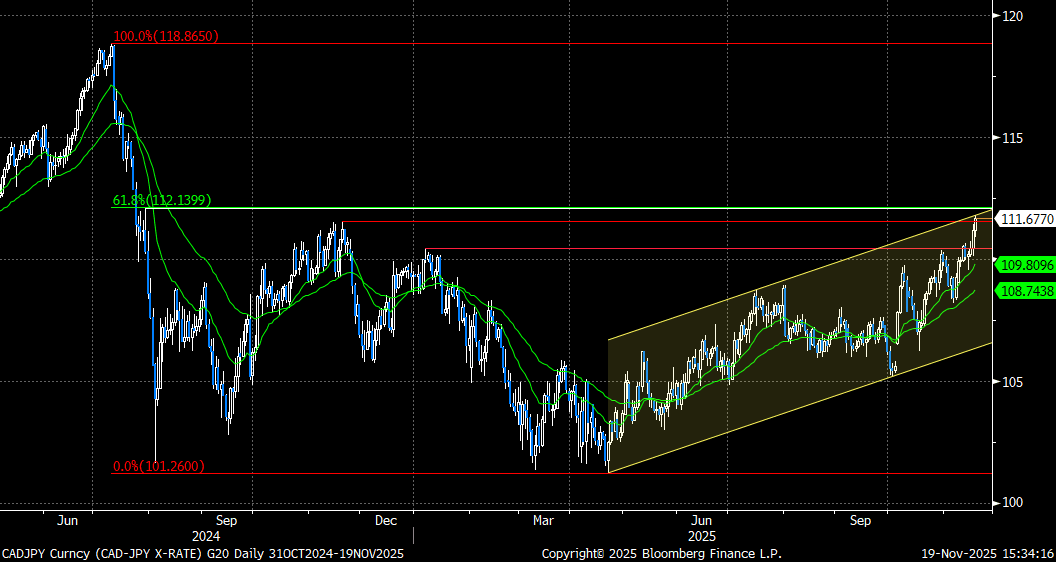

FOREX: CADJPY Approaching Clustered Resistance Zone

- With the Canadian dollar relatively outperforming its G10 peers on Wednesday, CADJPY has notably extended its most recent break above the years highs, which were located around 110.50.

- Today’s 0.52% advance has resulted in an additional breach of the November 2024 high, with spot rising to a high of 111.82 in recent trade. The move has significantly narrowed the gap to a notable cluster of resistance, with the cross now testing the top of a bull channel, drawn from the April lows.

- Above here, the July 30 2024 high is located at 112.10, which very closely coincides with the 61.8% retracement of the 2024-2025 downleg (shown below). Support for the cross moves up to 109.80, the 20-day EMA.

- We pointed out yesterday that moves have been bolstered by PM Mark Carney securing passage of the first federal budget of his tenure, ensuring the survival of his minority government. Furthermore, the fact that further BOC rate cuts are pretty much out of the question after October data provides a supportive CAD backdrop.

- Canada’s data calendar is relatively light this week, with September retail sales due on Friday.