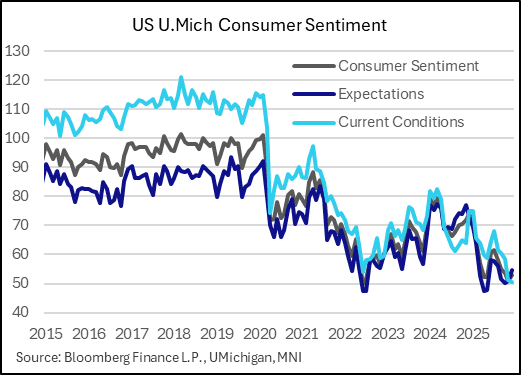

US DATA: UMich Sentiment Ends Year On Sour Note On Job And Inflation Concerns

Consumer sentiment ended the year on a down note, with the final UMichigan survey for December confirming the weakest current conditions reading in series history.

- Overall Consumer Sentiment was revised down slightly to 52.9 from 53.3 (51.0 Nov), with Expectations also revised down 0.4 points to 54.6 (51.0 Nov), while Current Conditions at the record low 50.4 (50.7 prelim, 51.1 Nov).

- The survey text summarizes the driver as "pocketbook issues continue to dominate consumer views of the economy" - namely inflation, with expectations of higher real income in the next year remaining around series lows and "good conditions" to buy a large household item continuing to decline from already depressed levels.

- Median 12M inflation expectations ticked up in the final (4.2% from 4.1% prelim) with 5-10Y steady at 3.2%, but both represented a decline from Nov (4.5% / 3.4%, respectively).

- But "Despite this softening in the outlook for future inflation, consumers remain strained by the persistence of high prices now. This month, 47% of consumers spontaneously mentioned that their personal finances were weighed down by high prices, unchanged from last month."

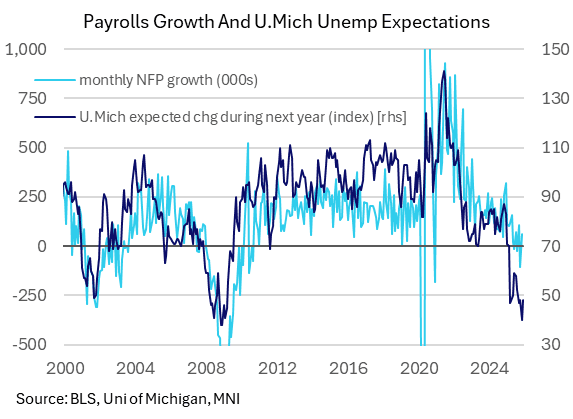

- We also take note that UMich surveys continue to point to deteriorating labor market dynamics; 63% of surveyed consumers expect unemployment to continue rising over the coming year, even though expected probability of job loss over the next 5 years actually fell to the lowest since February.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

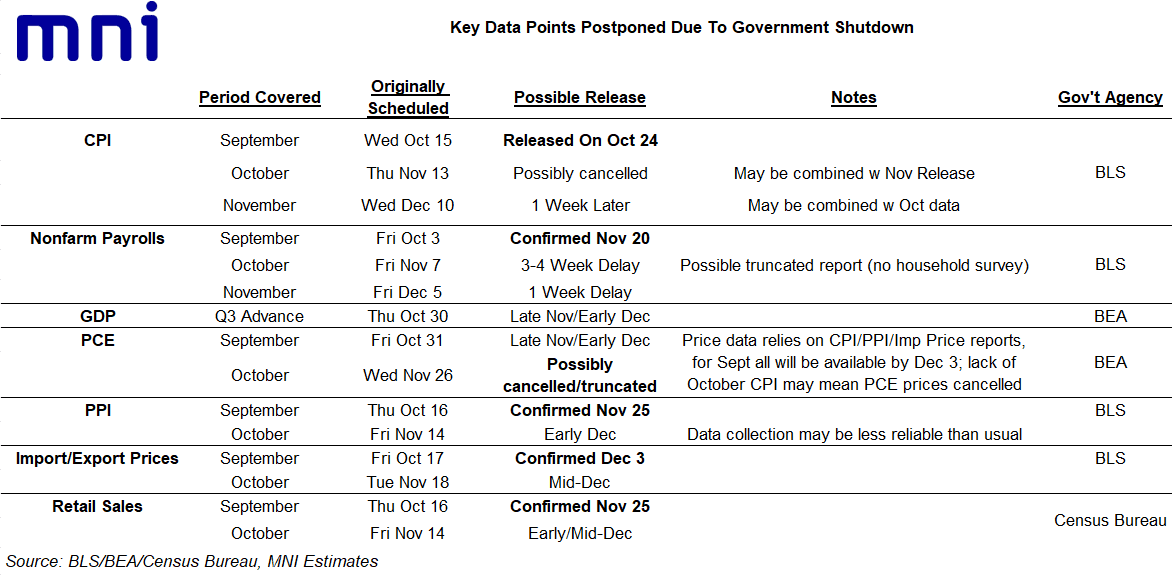

US DATA: Fed Still Unlikely To Have November CPI, Payrolls By Dec Decision Time

In our latest MNI FedSpeak podcast we discussed the outlook for economic data releases as the Federal Reserve's December decision looms - we also opined on what the meeting decision and messaging might be. To hear the full episode (recorded Tuesday), click here.

- Despite the latest scheduling updates indicating an increasing likelihood of getting Q3 GDP and September PCE in the coming couple of weeks, MNI remains doubtful that the Fed will have nonfarm payrolls data for November (originally scheduled for Dec 5) by its December 9-10 meeting - particularly since the BLS backlog appears to be clearing only slowly, and the Thanksgiving holiday (Nov 27) approaches. We acknowledge that opinions are mixed on the November payrolls release, with some analysts still having a Dec 5 release as their base case.

- When and if it does come out, October's dataset would include only the Establishment survey but not Household survey results (so headline payrolls but not unemployment rate etc), so there is a chance a short report will be produced by early Dec.

- Overall we think there's a good case to combine the October and November reports due to the data collection deficiencies in October. Merely getting a headline payrolls number from October may not be enough to sway Fed decision-making - in the event of a weak figure, hawks may shrug off the noisiness and uncertainty surrounding the collection of data in the month, while most are looking more closely at the unemployment rate anyway as a gauge of labor market looseness.

- And while there has been no official word from BLS, October CPI's reading will almost certainly be cancelled, which should preclude the publication of an October PCE prices report altogether. The November CPI data was scheduled to be released on the morning of the FOMC decision but that looks extremely unlikely.

- We update our key data points schedule below. Our FAQ on rescheduled data (Nov 11) remains largely intact, though releases are coming out a little more slowly than we had anticipated, by a few days to about a week - here

- Also see MNI's Data Methodology Cheat Sheet (Nov 13 - including methodologies underlying data releases) - here

GILTS: Steepening Extends, Swap Spreads Sell Off

{GB} GILTS:

- Futures as low as 91.59. Support at 91.82 and 91.67 is breached, strengthening the recent bearish theme. Downside focus moves to Fibonacci support located at 91.12.

- Long end UK swap spreads also extend their narrowing during the move (as noted in recent bullets), indicating increased fiscal & political risk premium in UK paper as PM Starmer’s future as leader of the Labour Party comes under scrutiny.

- Yields 1-7bp higher, curve steepening extends further.

- 10+-Year yields register highest levels seen since Mide October.

- Gilt/Bund spread out widens to 190bp, set for the highest close since October 21.

- Very front end of STIR curves anchored by this morning’s CPI data, which lowered the bar to a Dec cut, while further out the strip is more concerned with fiscal/political risks, resulting in steeper short end curves.

- BoE-dated OIS is 2bp more dovish to 3bp more hawkish on the day, showing 21bp of easing for December, 27bp for February, 35bp for March and 44bp through April.

- SONIA futures little changed to -4.5.

FOREX: Renewed Bid in USD Works Against Major Pairs; GBPUSD Slips

Renewed bid in the USD works further against the major pairs - pressing EURUSD, GBPUSD and others to new daily lows. Vague back-and-forth for risk sentiment remains the primary driver here, particularly with performance in Mag-7 stocks mirroring that of the S&P ahead of the post-market Nvidia earnings (these historically cross at 2120GMT/1620ET).

- GBP is underperforming on the latest leg, helping EURGBP rise back into positive territory on the day, although still below the earlier highs in turn triggered by political uncertainty. As a result, GBPUSD has narrowed the gap with the bear trigger of 1.3010 - a level that may come under pressure on any further signs of Starmer's support fracturing headed into next Wednesday's Budget (and beyond).

- We noted earlier today the elevated front-end of the GBP vol curve: The GBPUSD vol premium over EURUSD has only traded wider on two occasions since the Truss/Kwarteng budget in 2022: January 2025's GBP sell-off, and the BoE's 50bps rate hike in June 2023. This signals broad currency risk into Reeves' Budget - despite more settled expectations of the tax-and-spend measures.