US DATA: Existing Home Sales Still Soft Despite Modest Upside Momentum

Dec-19 15:32

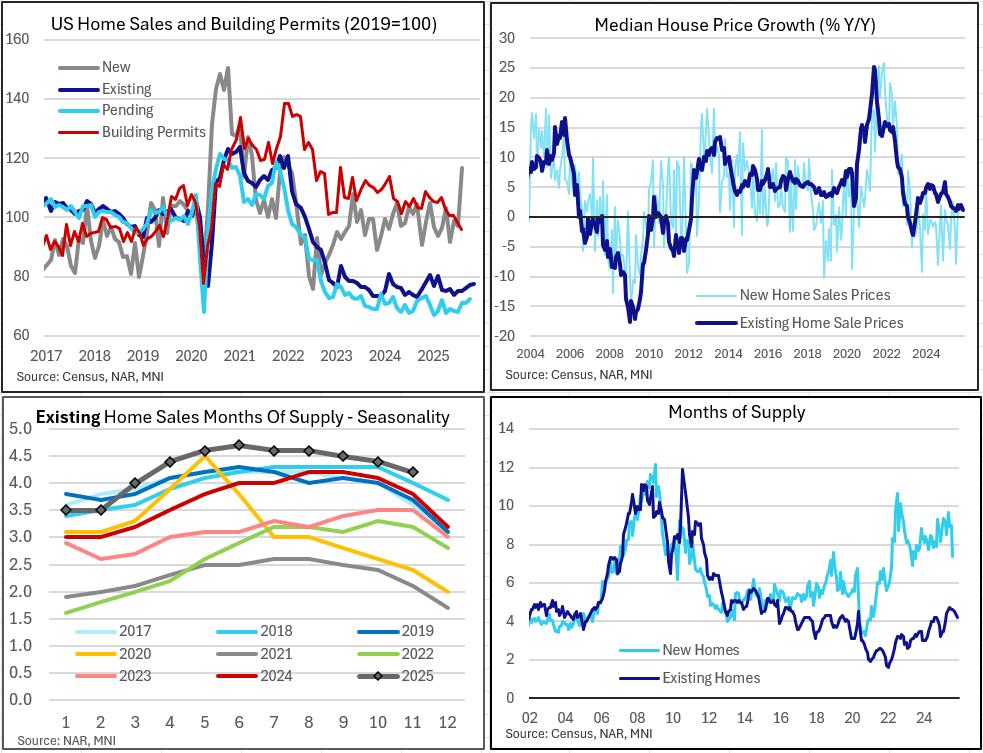

Existing home sales rose in November to the highest since February at 4.27M (seasonally-adjusted, annual rate). That was weaker than the expected 4.15M but up from 4.11M in October and marked a 3rd consecutive sequential increase. Overall existing sales data point to still-soft housing market dynamics amid high mortgage rates, though we continue to await the release of delayed "official" government data on residential investment in recent months.

- In the report, National Association of Realtors' Chief Economist Lawrence Yun attributed the improvement to "lower mortgage rates this autumn" but cautioned that "inventory growth is beginning to stall. With distressed property sales at historic lows and housing wealth at an all-time high, homeowners are in no rush to list their properties during the winter months."

- Inventory indeed fell sharply M/M in November, with a 5.9% drop to 1.43M homes for sales an 8-month low (all NSA, this is actually up from 1.33M a year prior) meant that implied months of supply fell to 4.2 from 4.4 for the lowest since March.

- While still above 4, it's tighter than the mid-year levels when it appeared that the existing homes market was on an inexorably loosening trajectory amid sustained high mortgage rates and weakening labor market/confidence. This is a typical seasonal pattern but overall supply this year has been at its highest in a decade.

- Median prices picked up 1.2% Y/Y ($409.2k) but this is weaker than inflation and very subdued vs the pandemic years with gains well into double-digits.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR -3.43M TO 424.2M NOV 14 WK

Nov-19 15:30

- US EIA: CRUDE OIL STOCKS EX SPR -3.43M TO 424.2M NOV 14 WK

- US EIA: DISTILLATE STOCKS +0.17M TO 111.1M IN NOV 14 WK

- US EIA: GASOLINE STOCKS +2.33M TO 207.4M IN NOV 14 WK

- US EIA: CUSHING STOCKS -0.7M TO 21.8M BARRELS IN NOV 14 WK

- US EIA: SPR +0.53M TO 410.9M BARRELS IN NOV 14 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +0.6% TO 90.0% IN NOV 14 WK

US TSY FUTURES: December'25-March'26 Roll Update

Nov-19 15:21

The latest Tsy quarterly futures roll volumes for December'25 to March'26 outlined below. Percentage complete gradually rising ahead the "First Notice" date of Friday, November 28. Current roll details:

- TUZ5/TUH6 appr 210,200 from -6.0 to -5.62, -5.75 last; 7% complete

- FVZ5/FVH6 appr 453,100 from -2.75 to -2.25, -2.25 last; 13% complete

- TYZ5/TYH6 appr 70,600 from 1.5 to 2.0, 2.0 last; 12% complete

- UXYZ5/UXYH6 43,600 from 5.25 to 5.5, 5.5 last; 5% complete

- USZ5/USH6 27,500 from 13.0 to 14.0, 13.75 last; 9% complete

- WNZ5/WNH6 appr 147,800 from 9.75 to 10.25, 10.0 last; 7% complete

- Reminder, Dec'25 futures don't expire until next month: 10s, 30s and Ultras on December 19, 2s and 5s on December 31. Meanwhile, Dec'25 Tsy options will expire this Friday, November 21

OPTIONS: Expiries for Nov20 NY cut 1000ET (Source DTCC)

Nov-19 15:19

- EUR/USD: $1.1500(E2.0bln), $1.1550(E559mln), $1.1600(E1.1bln), $1.1625-30(E1.8bln), $1.1675-80(E1.5bln)

- USD/JPY: Y150.00($1.3bln), Y155.00($1.4bln)

- GBP/USD: $1.3250(Gbp679mln)

- EUR/GBP: Gbp0.8750(E524mln)

- AUD/USD: $0.6500(A$737mln)

- AUD/NZD: N$1.1400(A$537mln)

- USD/CNY: Cny7.1080-89($2.0bln)